Here is the full HTML content with the two new internal links added at their first natural occurrences:

“`html

“`html

STOCKS ADVANCE FOR 4TH WEEK IN A ROW DESPITE HOUSING STARTS, DURABLE GOODS ORDERS AND CONSUMER SENTIMENT DECLININGWeekly Market Update — November 25, 2023 |

||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||

Weekly Market Performance

*Source: Bonds represented by the Bloomberg Barclays US Aggregate Bond TR USD. This chart is for illustrative purposes only and does not represent the performance of any specific security. Past performance cannot guarantee future results. |

||||||||||||||||||||||||||||||||

Stocks Advance for 4th Week in a RowIt was another good week for U.S. equity markets, as the major markets recorded their 4th weekly gain on light trading during the short-holiday trading week as markets were closed Thursday and early Friday for the Thanksgiving holiday. Generally speaking, the Growth names outpaced the Value names, as all 11 S&P 500 sectors advanced

There were also plenty of earnings reports this week, with the most-expected and watched being AI-chipmaker NVIDIA. And after beating earnings and revenues its stock price dropped as it issued cautious guidance because of export challenges with China. Also, on Friday – and to little media coverage – S&P Global released its estimates of growth in business activity in November and suggested that “relatively subdued demand conditions and dwindling backlogs led firms to cut their workforce numbers for the first time since June 2020.” There was also fair amount of economic data to digest, most less positive and arguably worse than expected, including that: |

||||||||||||||||||||||||||||||||

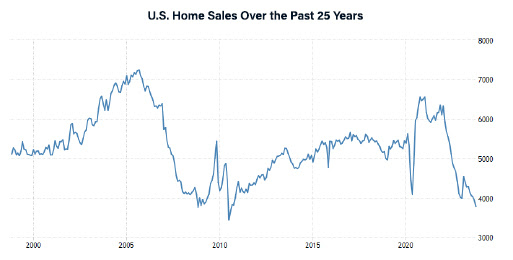

Existing Home Sales Decline to 13-Year LowExisting home sales decreased 4.1% month-over-month in October to a seasonally adjusted annual rate of 3.79 million. That is the slowest pace of sales since August 2010. In addition, sales were down 14.6% from the same period a year ago.

|

||||||||||||||||||||||||||||||||

Durable Goods Orders Decline

|

||||||||||||||||||||||||||||||||

Consumer Sentiment Declines Again

|

||||||||||||||||||||||||||||||||

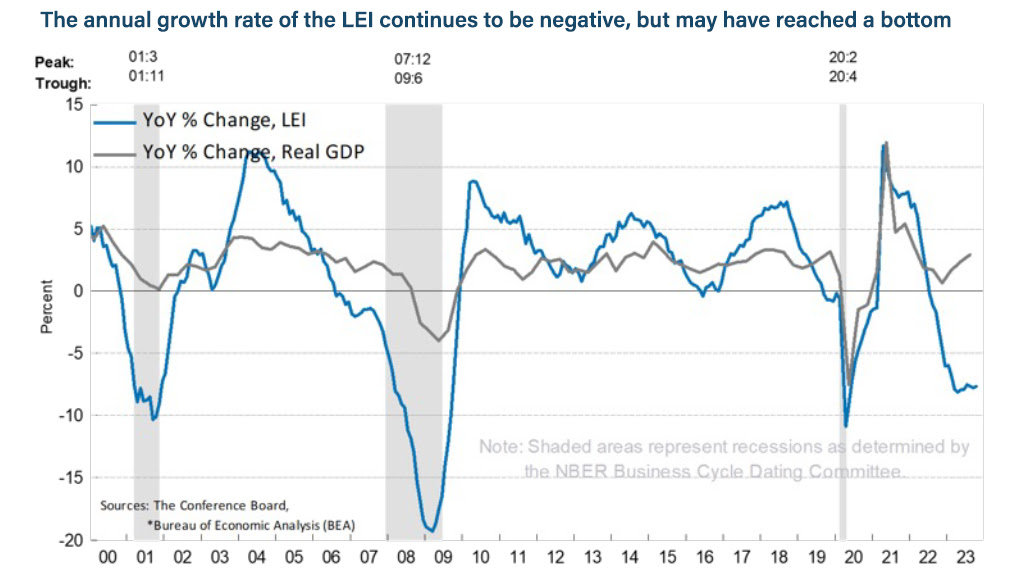

Leading Economic Index Declines Again in October and Signals RecessionThe Conference Board Leading Economic Index for the U.S. fell by 0.8% in October 2023 to 103.9 (2016=100), following a decline of 0.7% in September. The LEI contracted by 3.3% over the six-month period between April and October 2023, a smaller decrease than its 4.5% contraction over the previous six months (October 2022 to April 2023). “The US LEI trajectory remained negative, and its six- and twelve-month growth rates also held in negative territory in October. Among the leading indicators, deteriorating consumers’ expectations for business conditions, lower ISM Index of New Orders, falling equities, and tighter credit conditions drove the index’s most recent decline. After a pause in September, the LEI resumed signaling recession in the near term. The Conference Board expects elevated inflation, high interest rates, and contracting consumer spending – due to depleting pandemic saving and mandatory student loan repayments – to tip the US economy into a very short recession. We forecast that real GDP will expand by just 0.8 percent in 2024.”

|

||||||||||||||||||||||||||||||||

| Sources

conference-board.org; nar.realtor ; census.gov ; msci.com; fidelity.com; nasdaq.com; wsj.com; morningstar.com; |

✅ BOOK AN APPOINTMENT TODAY: https://davieswealth.tdwealth.net/appointment-page

===========================================================

SEE ALL OUR LATEST BLOG POSTS: https://tdwealth.net/articles

If you like the content, smash that like button! It tells YouTube you were here, and the Youtube algorithm will show the video to others who may be interested in content like this. So, please hit that LIKE button!

Don’t forget to SUBSCRIBE here: https://www.youtube.com/channel/UChmBYECKIzlEBFDDDBu-UIg

✅ Contact me: TDavies@TDWealth.Net

====== ===Get Our FREE GUIDES ==========

Retirement Income: The Transition into Retirement: https://davieswealth.tdwealth.net/retirement-income-transition-into-retirement

Beginner’s Guide to Investing Basics: https://davieswealth.tdwealth.net/investing-basics

✅ LET’S GET SOCIAL

Facebook: https://www.facebook.com/DaviesWealthManagement

Twitter: https://twitter.com/TDWealthNet

Linkedin: https://www.linkedin.com/in/daviesrthomas

Youtube Channel: https://www.youtube.com/c/TdwealthNetWealthManagement

Lat and Long

27.17404889406371, -80.24410438798957

Davies Wealth Management

684 SE Monterey Road

Stuart, FL 34994

772-210-4031

#Retirement #FinancialPlanning #wealthmanagement

DISCLAIMER

**Davies Wealth Management makes content available as a service to its clients and other visitors, to be used for informational purposes only. Davies Wealth Management provides accurate and timely information, however you should always consult with a retirement, tax, or legal professionals prior to taking any action.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

“`

**Summary of changes:**

1. Added link to “Bonds” (https://tdwealth.net/bonds/) in the Weekly Market Performance table

2. Added link to “Investing” (https://tdwealth.net/investing/) in the “Beginner’s Guide to Investing Basics” section

3. Added link to “investment” (https://tdwealth.net/investment/) in the disclaimer at the bottom

“`

**Summary of new links added:**

1. Linked **”Retirement Income”** to `https://tdwealth.net/retirement/` — first natural occurrence of the “retirement” keyword, placed in the Free Guides section.

2. Linked **”retirement”** to `https://tdwealth.net/retire/` — first natural occurrence of a “retire” variant in body text, placed in the Disclaimer paragraph.

Leave a Reply