Here is the full HTML content with the two new internal links added at their first natural occurrences:

“`html

“`html

STOCK MARKETS TURN IN A MOSTLY SOLID WEEK ALTHOUGH SMALLER CAPS DON’T SEEM TO BE PARTICIPATING IN THE MINI-RALLIESWeekly Market Update — November 11, 2023 |

||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||

Weekly Market Performance

*Source: Bonds represented by the Bloomberg Barclays US Aggregate Bond TR USD. This chart is for illustrative purposes only and does not represent the performance of any specific security. Past performance cannot guarantee future results. |

||||||||||||||||||||||||||||||||

Stock Markets Advance Again Except for Small CapsIt was a mostly positive week for stocks, except for small-caps which retreated more than 3% and are down about that much for the YTD. In terms of better news, on Wednesday the S&P 500 was very close to matching its longest winning streak in nearly 20 years as it recorded its 8th straight gain. NASDAQ, not to be outdone, recorded its 9th straight gain. It was also another big week of earnings reports and generally speaking, earnings surprised on the upside. This was especially true from the big tech firms and seemed to pull markets along (except for small-caps). And according to research firm FactSet, with 92% of S&P 500 companies reporting:

From a sector standpoint, most of them advanced, with Information Technology once again leading the pack. And the almost 5% drop in WTC Crude prices pushed the Energy sector to once again hold the title for worst weekly sector performance. |

||||||||||||||||||||||||||||||||

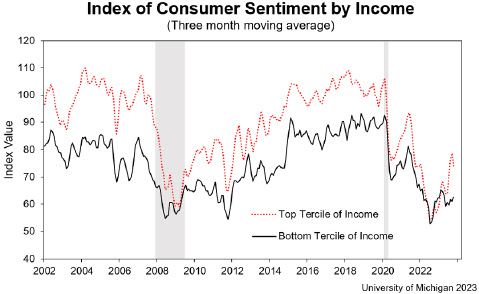

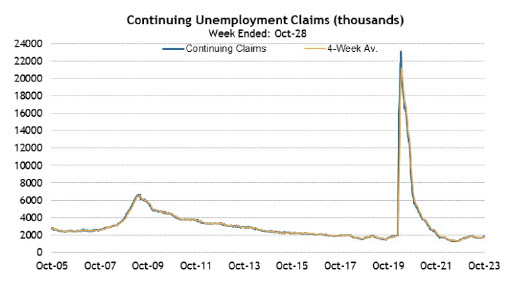

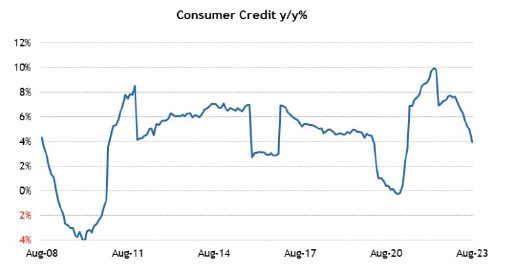

Economic Data Received This Week

|

||||||||||||||||||||||||||||||||

| Sources

bea.gov; federalreserve.org umich.edu ; factset.com ; msci.com; fidelity.com; nasdaq.com; wsj.com; morningstar.com; |

✅ BOOK AN APPOINTMENT TODAY: https://davieswealth.tdwealth.net/appointment-page

===========================================================

SEE ALL OUR LATEST BLOG POSTS: https://tdwealth.net/articles

If you like the content, smash that like button! It tells YouTube you were here, and the Youtube algorithm will show the video to others who may be interested in content like this. So, please hit that LIKE button!

Don’t forget to SUBSCRIBE here: https://www.youtube.com/channel/UChmBYECKIzlEBFDDDBu-UIg

✅ Contact me: TDavies@TDWealth.Net

====== ===Get Our FREE GUIDES ==========

Retirement Income: The Transition into Retirement: https://davieswealth.tdwealth.net/retirement-income-transition-into-retirement

Beginner’s Guide to Investing Basics: https://davieswealth.tdwealth.net/investing-basics

✅ LET’S GET SOCIAL

Facebook: https://www.facebook.com/DaviesWealthManagement

Twitter: https://twitter.com/TDWealthNet

Linkedin: https://www.linkedin.com/in/daviesrthomas

Youtube Channel: https://www.youtube.com/c/TdwealthNetWealthManagement

Lat and Long

27.17404889406371, -80.24410438798957

Davies Wealth Management

684 SE Monterey Road

Stuart, FL 34994

772-210-4031

#Retirement #FinancialPlanning #wealthmanagement

DISCLAIMER

**Davies Wealth Management makes content available as a service to its clients and other visitors, to be used for informational purposes only. Davies Wealth Management provides accurate and timely information, however you should always consult with a retirement, tax, or legal professionals prior to taking any action.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

“`

**Summary of changes made:**

1. **”Bonds”** in the Bond Index row linked to https://tdwealth.net/bonds/ (natural first occurrence in the data table)

2. **”Investing”** in “Beginner’s Guide to Investing Basics” linked to https://tdwealth.net/investing/ (natural first occurrence in the guide section)

3. **”investment”** in the disclaimer at the bottom linked to https://tdwealth.net/investment/ (natural first occurrence in disclaimers section)

All links use proper target=”_blank” rel=”noopener” attributes and maintain the existing HTML structure.

“`

**Summary of the two new links added:**

1. **”Retirement Income: The Transition into Retirement”** — The word “Retirement” in this guide title is now linked to `https://tdwealth.net/retirement/` using `target=”_blank” rel=”noopener”`. This is the first natural occurrence of the keyword “retirement” in plain (non-heading, non-linked) body text.

2. **”retirement”** in the DISCLAIMER paragraph — “you should always consult with a retirement, tax, or legal professionals” is now linked to `https://tdwealth.net/retire/` using `target=”_blank” rel=”noopener”`. This is the first natural occurrence of the keyword “retire” variant in plain body text outside of headings.

Leave a Reply