“`html

Free Playbook

Financial Planning for Professional Athletes

5 plays to protect your wealth when 80% of your income arrives before age 30.

If you’re skating for the Florida Panthers or Tampa Bay Lightning, you’ve already made one of the smartest financial moves of your career: playing in a state with zero income tax. But when it comes to NHL retirement savings plan optimization, most pro athletes leave serious money on the table by treating their pension as a set-it-and-forget-it benefit.

As a fee-only fiduciary wealth manager serving professional athletes from our Stuart office: a strategic hub for Treasure Coast families near Jupiter Island and Palm Beach Gardens: I’ve seen firsthand how proper NHL pension strategy can add hundreds of thousands to your retirement nest egg. Unlike commission-based brokers who earn kickbacks from product sales, our legal fiduciary standard requires us to act solely in your best interest, period.

Let’s break down how to maximize every dollar the NHL owes you, optimize tax mitigation strategies, and build a retirement plan that matches your playing career intensity.

Understanding Your NHL Pension Foundation

The NHL pension operates as a defined benefit plan, which means it provides guaranteed payouts regardless of market performance. Think of it as your financial goalie: it’s there to protect you when the earning years are over.

Here’s how the math works: You earn one quarter of credited service for every 20 NHL games on the roster, whether you’re logging 20 minutes of ice time or sitting on the bench. Accumulate 40 quarters (800 games over roughly 10 seasons), and you’ve maxed out at approximately $275,000 annually starting at age 62. That figure includes Cost-of-Living Adjustments, so it rises with inflation.

For players with shorter careers, the pension prorates based on credited service. Five years in the league? You’re looking at roughly 50% of the max benefit: still a solid foundation, but far from the full potential. This is where strategic planning separates the financial all-stars from the players who scramble in retirement.

The Florida Advantage: Pro Athlete Tax Mitigation

Here’s where geography becomes your power play. Florida’s zero state income tax gives you an immediate edge over players in California (13.3% top rate), New York (10.9%), or Canada (up to 53% combined federal-provincial rates). But the real opportunity lies in coordinating your pension timing with residency status.

Your NHL pension income is fully taxable at the federal level, but establishing legitimate Florida domicile means zero state tax on those payments: forever. For a player maxing out at $275,000 annually, that’s a six-figure tax savings over a 25-year retirement compared to living in a high-tax state.

The catch? The IRS and other states scrutinize pro athletes relentlessly. You need an audit-proof domicile strategy that includes establishing a primary residence, changing voter registration, updating driver’s licenses, and documenting the substantial majority of your time here. Our Stuart office regularly helps Panthers and Lightning players navigate these requirements to protect their Florida tax status.

Strategic Retirement Timing: When to Start Drawing Benefits

The NHL pension offers flexibility in when you start collecting, but each option carries trade-offs:

| Retirement Age | Benefit Level | Strategic Consideration |

|---|---|---|

| Age 45 (Early) | Actuarially reduced | Best if you have other income streams and need immediate cash flow |

| Age 62 (Standard) | Full calculated benefit | Optimal for most players; balances longevity risk with maximum payout |

| Age 65+ (Delayed) | Increased payments | Consider if still earning substantial income or in excellent health |

Most financial advisors: especially those earning commissions on insurance products: will push you toward early retirement to “lock in” benefits. That’s backwards thinking for NHL players who typically have additional income from endorsements, business ventures, or second careers in broadcasting.

The real optimization happens when you coordinate pension timing with:

- 401(k) withdrawal strategies (required minimum distributions start at age 73)

- Social Security benefits (claiming age significantly impacts lifetime payouts)

- Tax bracket management (stacking all income sources in one year can push you into higher brackets unnecessarily)

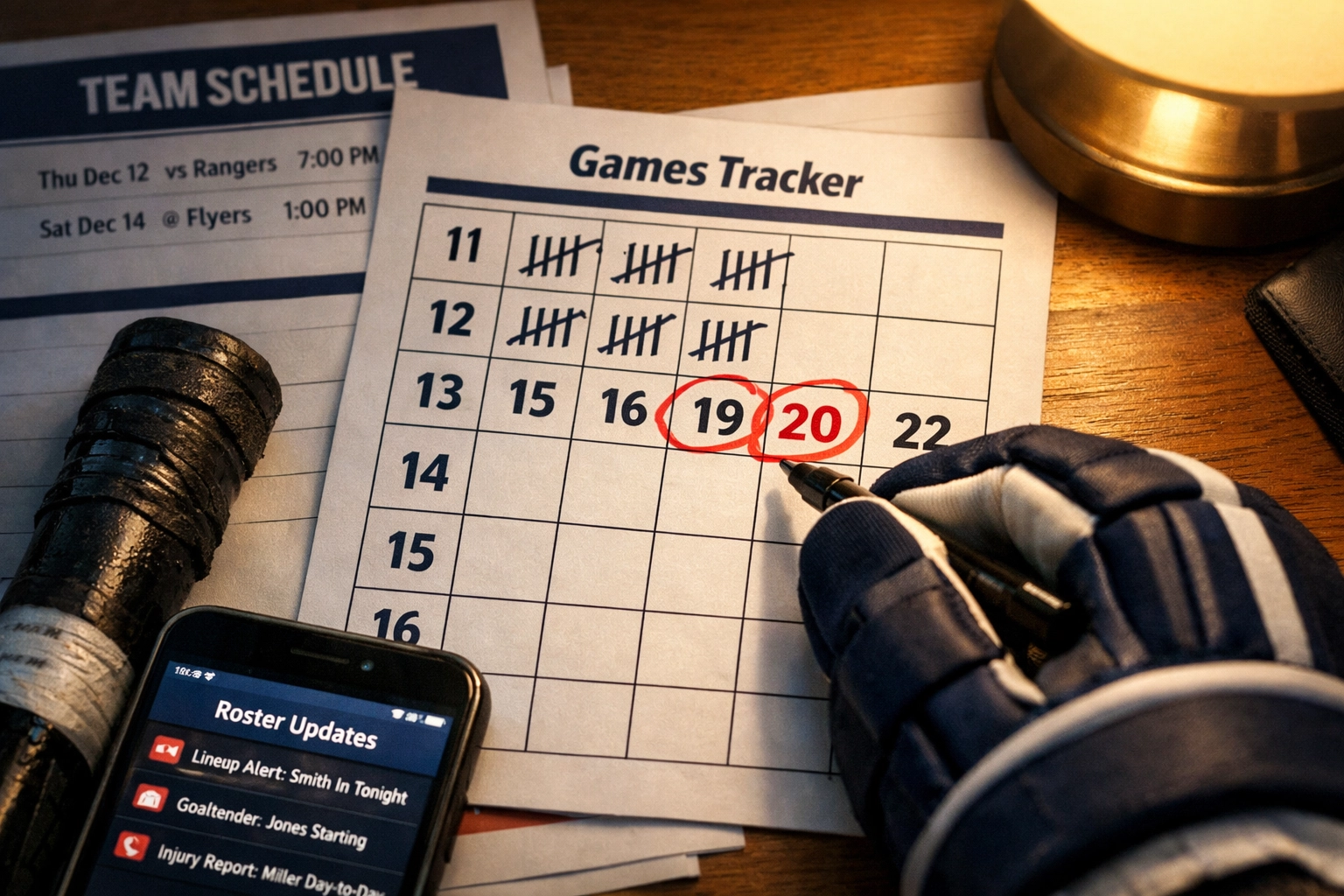

Maximizing Credited Service: Every Game Counts

Here’s a strategy most agents miss: If you’re on the bubble between roster spots or considering a late-career stint in Europe, the 20-game threshold matters enormously. Playing 19 games earns you nothing toward pension credits. Game 20 earns you a full quarter.

For players in years 8-10 of their careers, pushing for those final roster spots isn’t just about pride: it’s about securing maximum lifetime benefits that compound over decades. The difference between 36 quarters and 40 quarters? Roughly $27,500 annually for life. Over a 25-year retirement, that’s nearly $700,000 in additional pension income.

Veterans negotiating contracts should explicitly factor pension qualification into discussions. A lower salary on a team that guarantees roster time may actually be more valuable than higher pay with uncertain playing time if you’re approaching 800-game thresholds.

Beyond the Pension: Building Comprehensive Wealth

The NHL pension should anchor your retirement strategy, not comprise it entirely. Professional athletes face unique challenges: compressed earning windows, injury risks, and the psychological adjustment from elite performance to retirement. A comprehensive financial planning for professional athletes includes:

401(k) Contributions: Max out the $23,000 annual limit ($30,500 if you’re 50+). Even better, use the Roth 401(k) option if available to create tax-free retirement income that complements your taxable pension.

Deferred Compensation: Some players negotiate deferred salary payments that spread income across multiple years, smoothing tax brackets and extending career earnings beyond playing days.

Tax-Loss Harvesting in Taxable Accounts: Unlike mutual funds that distribute capital gains annually, properly structured portfolios can offset gains with strategic losses, minimizing your tax bill during high-earning years.

Survivor Benefits: Protecting Your Family’s Financial Security

The NHL pension offers joint and survivor elections that ensure your spouse continues receiving full benefits for life after your death. This isn’t optional planning: it’s essential, especially for players who marry during or shortly after their careers.

The mistake we see repeatedly: Players elect single-life benefits to maximize immediate payments, then attempt to purchase life insurance to “replace” survivor income. This approach typically costs more and provides less security than the pension’s built-in survivor option.

Review your beneficiary designations annually. Life changes: marriage, divorce, children: require updates to pension paperwork to ensure your wishes are honored. The NHL pension plan won’t automatically adjust for these events.

Local Resources for Treasure Coast Athletes

Playing in South Florida puts you in proximity to exceptional wealth management infrastructure. The Stuart area serves as a strategic hub for professional athletes seeking sophisticated planning without the congestion of Miami or Fort Lauderdale.

For NHL players balancing careers in Tampa or Sunrise with personal lives in Jupiter, Palm Beach Gardens, or Martin County, proximity to qualified fiduciary advisors who understand both the pension system and Florida residency requirements creates significant advantages.

Additionally, leveraging resources like community financial education through 1715tcf.com helps athletes connect with local professionals who specialize in the unique challenges facing professional athletes: from pro athlete tax mitigation to estate planning for families with significant but time-limited income streams.

The Qualified Exit Strategy

Here’s the reality: Only about 2% of hockey players who make the NHL play 10+ seasons. The average career lasts 5-6 years, which means most players earn partial pension benefits while their prime earning years last less than a decade.

This compressed timeline demands aggressive wealth accumulation during playing years and sophisticated tax planning during retirement. Working with a fee-only fiduciary eliminates the conflict of interest inherent in commission-based advice. You’re not being steered toward high-fee annuities or insurance products that primarily benefit the seller.

Instead, your retirement strategy focuses on maximizing pension credits, optimizing retirement account contributions, establishing Florida domicile to eliminate state taxes, and building diversified portfolios that support your family long after the final horn sounds.

Your Next Play

NHL pension strategy isn’t something you figure out after hanging up your skates: it’s a multi-year optimization process that starts the moment you sign your first NHL contract. Every game played, every contribution decision, and every tax planning choice compounds over decades.

If you’re a professional athlete in Florida or considering relocating here to maximize your retirement outcomes, the first step is understanding whether comprehensive pension optimization and tax mitigation planning makes sense for your situation.

Qualify for an appointment by completing our brief questionnaire. We work exclusively with athletes and high-net-worth families who value transparent, fiduciary guidance over product sales.

Your playing career is short. Your retirement is long. Make sure your financial planning strategy matches the intensity you bring to the ice.

“`

Leave a Reply