Retirement planning for high net worth individuals presents unique challenges and opportunities. At Davies Wealth Management, we understand that preserving wealth while maintaining a desired lifestyle requires specialized strategies.

Our expertise in navigating complex financial landscapes allows us to create tailored solutions for our high net worth clients. This blog post will explore key considerations and effective approaches to ensure a secure and fulfilling retirement for those with substantial assets.

What Are the Unique Retirement Needs of High Net Worth Individuals?

Complex Financial Landscapes

High net worth individuals (HNWIs) face distinct challenges when planning for retirement. Their financial situations often involve diverse asset portfolios, including stocks, bonds, real estate, and alternative investments. This complexity requires a sophisticated approach to retirement planning. HNWIs often diversify their retirement portfolios beyond traditional accounts, incorporating alternative investments and private wealth management strategies.

Wealth Preservation and Lifestyle Maintenance

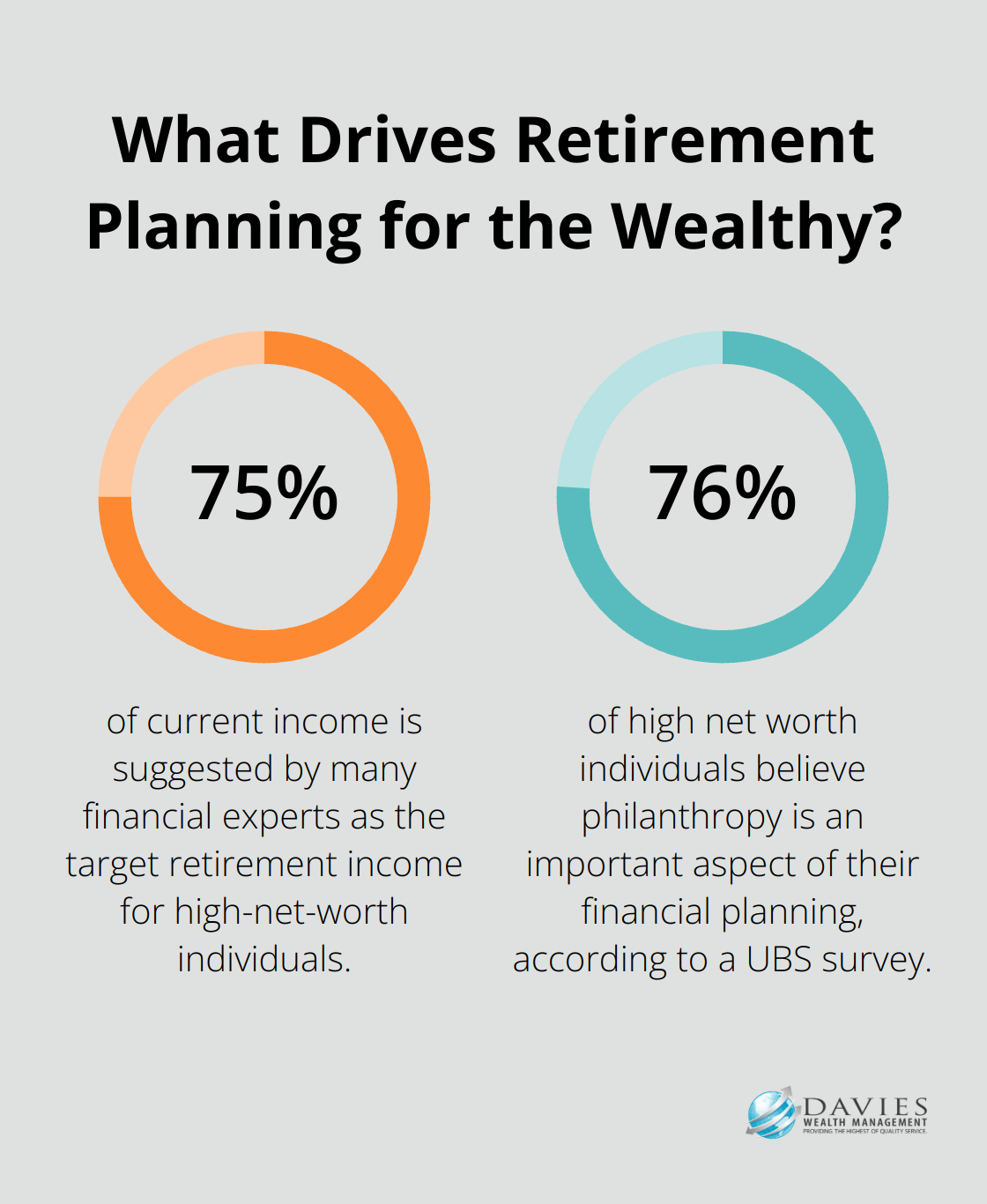

A primary concern for HNWIs in retirement is to maintain their accustomed lifestyle while ensuring their wealth lasts. Many financial experts suggest that high-net-worth individuals should try to achieve 75% of their current income as their target retirement income. This figure is based on reducing spending at retirement by 5% and saving 8% of gross household income.

It’s essential to factor in inflation when making these projections. With a 3% annual inflation rate, that $150,000 income need today would rise to about $201,587 in 10 years. This highlights the importance of creating a retirement strategy that not only preserves wealth but also allows for growth to outpace inflation.

Tax Implications and Estate Planning

Tax considerations play a significant role in retirement planning for HNWIs. Effective tax strategies can help maximize retirement income and preserve wealth for future generations. For instance, utilizing tax-advantaged accounts (like Roth IRAs) can provide options for tax-free growth and withdrawals, aiding long-term planning.

Estate planning is another critical aspect of retirement planning for HNWIs. A UBS survey found that 76% of HNWIs believe philanthropy is an important aspect of their financial planning. This underscores the need for strategies that not only minimize estate taxes but also align with personal values and legacy goals.

Professional Guidance and Expertise

Given the complexity of HNWI retirement planning, professional guidance is often necessary. A wealth management team can provide comprehensive strategies that address all aspects of retirement planning, from investment management to tax optimization and estate planning. Davies Wealth Management, for example, offers tailored solutions for high net worth clients, ensuring their unique needs and goals are met.

As we move forward, we’ll explore key strategies that HNWIs can employ to effectively plan for their retirement, taking into account their unique financial situations and long-term objectives.

Effective Strategies for High Net Worth Retirement

High net worth individuals (HNWIs) require sophisticated retirement planning strategies that go beyond traditional approaches. Several key tactics can significantly enhance retirement outcomes for affluent clients.

Diversification Beyond Conventional Assets

While traditional stocks and bonds form the foundation of many retirement portfolios, HNWIs benefit from broader diversification. A 2021 report by Capgemini revealed that the global high-net-worth individual (HNWI) population grew 6.3%, surpassing the 20-million bar. This growing demographic increasingly turns to alternative investments to enhance returns and manage risk.

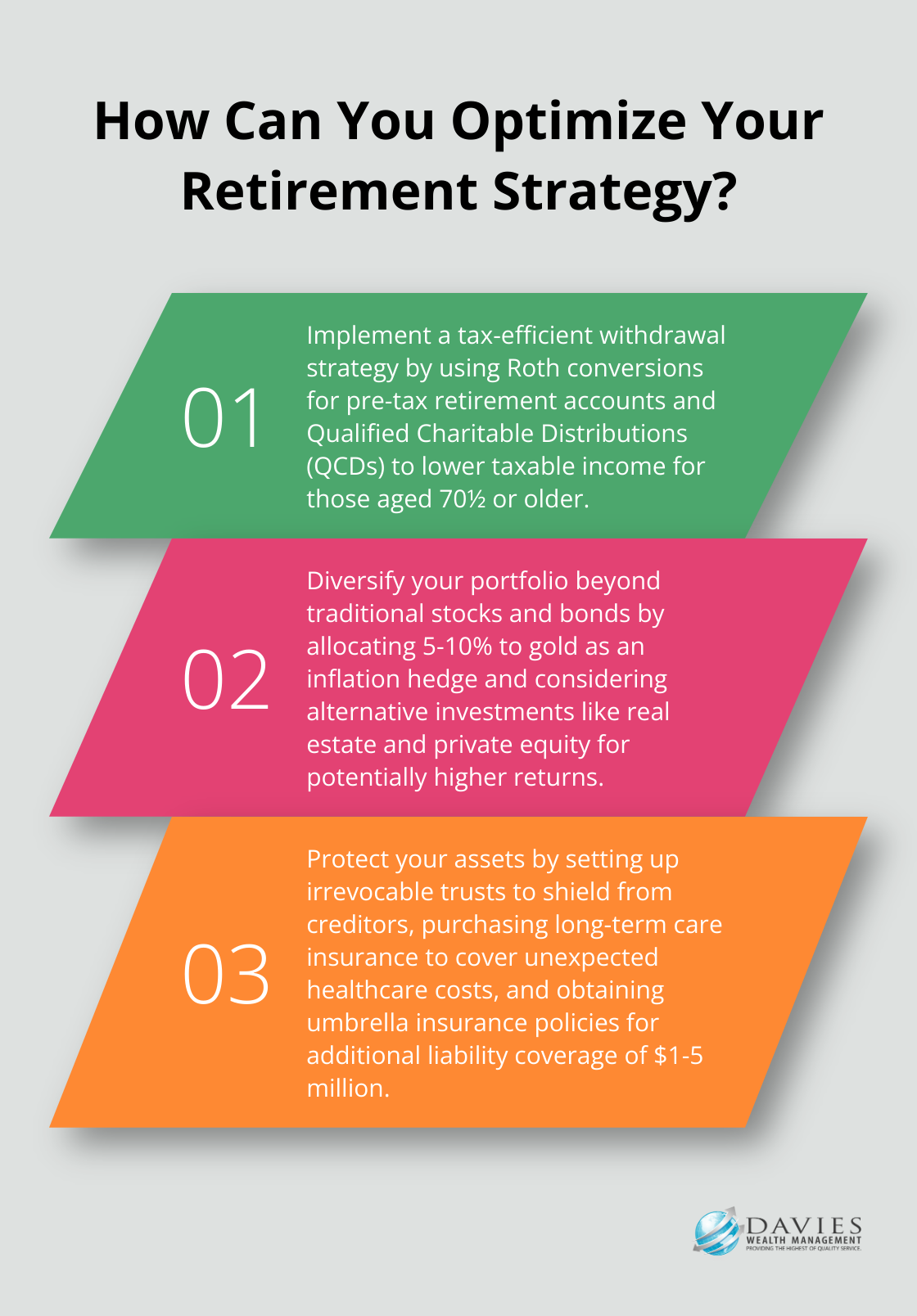

Real estate investments (both residential and commercial) can provide steady cash flow and potential appreciation. Private equity offers opportunities for higher returns, albeit with increased risk and reduced liquidity. Commodities and precious metals can serve as inflation hedges. For example, allocating 5-10% of a portfolio to gold has historically provided a buffer against economic uncertainty.

Tax-Efficient Withdrawal Strategies

Tax management plays a vital role for HNWIs in retirement. One effective strategy involves the strategic use of Roth conversions. Roth conversions involve taking money from a pre-tax retirement account, such as a 401(k) or traditional IRA, and converting it into a Roth IRA.

Another approach utilizes Qualified Charitable Distributions (QCDs). For those aged 70½ or older, donating up to $105,000 directly from Required Minimum Distributions (RMDs) to qualified charities can lower taxable income. This strategy not only fulfills philanthropic goals but also provides significant tax benefits.

Risk Mitigation Through Asset Protection

Asset protection is paramount for HNWIs. One effective method involves the use of trusts. Irrevocable trusts, for instance, can shield assets from creditors and provide tax benefits. A study by Wealth-X highlighted that many HNWIs prioritize these structures for both asset protection and estate planning purposes.

Insurance also plays a key role in risk management. Long-term care insurance can protect retirement assets from depletion due to unexpected healthcare costs. The average annual cost of long-term care insurance when purchasing $165,000 of immediate benefits for a 55-year-old man is $900.

HNWIs should also consider umbrella insurance policies to provide additional liability coverage beyond standard homeowners or auto insurance. These policies typically offer $1 million to $5 million in coverage, protecting against potential lawsuits that could otherwise jeopardize retirement savings.

Personalized Wealth Management Solutions

Creating comprehensive retirement strategies that address these complex needs requires expertise and a tailored approach. A wealth management team should work closely with clients to develop personalized plans that optimize tax efficiency, manage risk, and preserve wealth for generations to come. This collaborative process ensures that HNWIs can navigate the intricacies of retirement planning with confidence and peace of mind.

As we explore the importance of professional guidance in the next section, we’ll examine how a dedicated wealth management team can provide invaluable support in implementing these strategies and achieving long-term financial success.

Leveraging Expert Guidance for Retirement Success

The Power of a Holistic Approach

A wealth management team combines diverse expertise to address all aspects of your financial life. This comprehensive view proves essential for high net worth individuals, as it ensures that investment strategies, tax planning, and estate considerations work in harmony. A comprehensive wealth management strategy can help secure your retirement by balancing growth, risk, and legacy planning.

Synergy of Financial Professionals

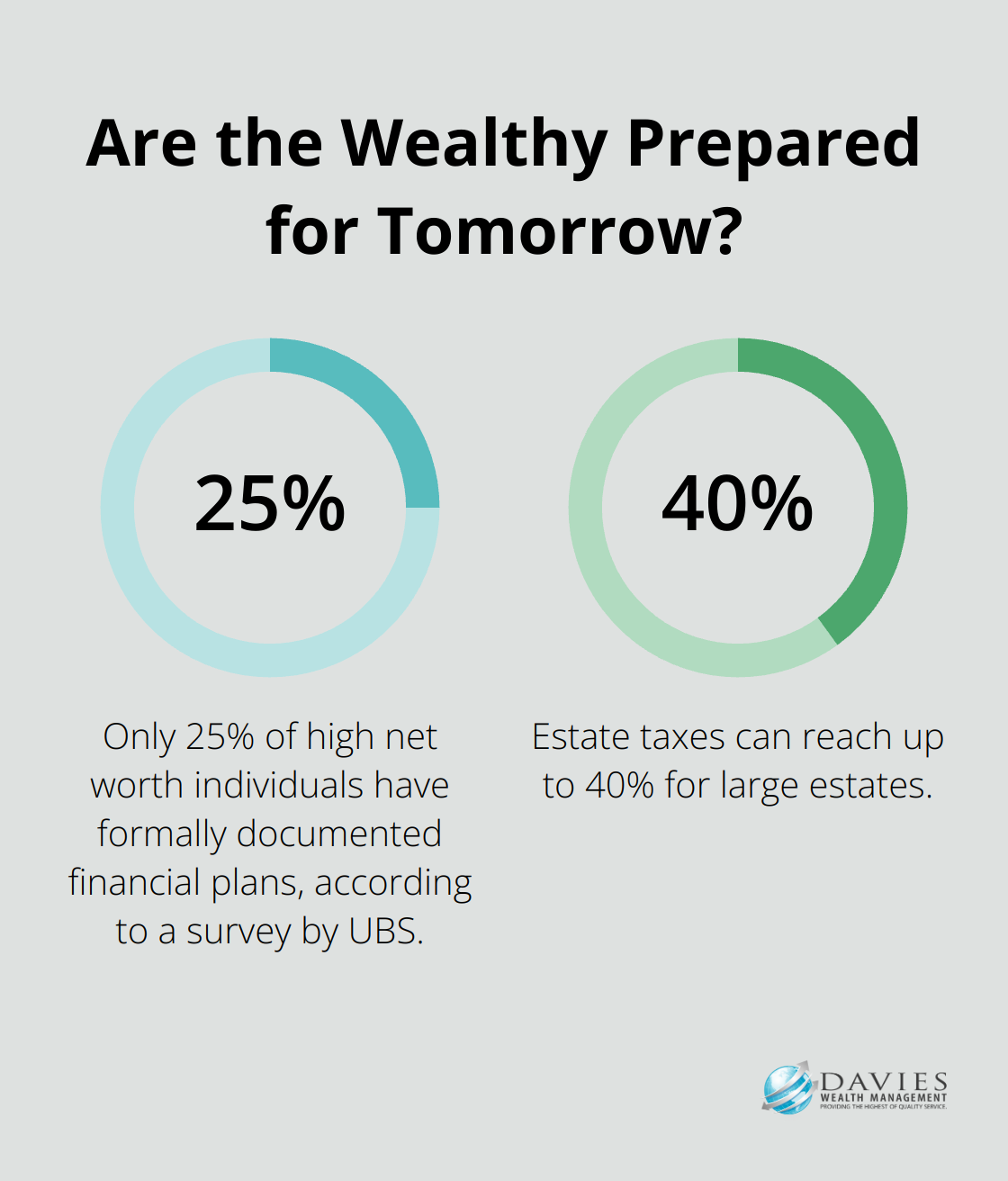

Coordination with tax professionals and estate planning attorneys forms a cornerstone of effective wealth management. These specialists work together to optimize your financial strategy. A tax professional might identify opportunities for tax-loss harvesting (potentially saving thousands in taxes annually). An estate planning attorney could structure trusts to protect your assets and minimize estate taxes (which can reach up to 40% for large estates).

Adapting to Change Through Regular Reviews

The financial landscape constantly evolves, and your retirement plan should follow suit. Regular reviews are not just beneficial; they are essential. A survey by UBS revealed that only 25% of high net worth individuals have formally documented financial plans, which indicates a significant opportunity for improvement through professional guidance. We recommend quarterly reviews for high net worth clients, allowing for strategy adjustments in response to market changes, life events, or shifts in financial goals.

Tailored Solutions for Complex Needs

High net worth individuals often face unique challenges that require customized solutions. A wealth management team can develop strategies that address specific concerns such as:

- Business succession planning for entrepreneurs

- International tax considerations for those with global assets

- Philanthropic planning to align financial goals with personal values

Technology and Data-Driven Insights

Modern wealth management leverages advanced technology and data analytics to enhance decision-making. Sophisticated portfolio management tools can provide real-time insights into asset allocation, risk exposure, and performance metrics. This data-driven approach allows for more precise and timely adjustments to retirement strategies, ensuring they remain aligned with long-term objectives.

Final Thoughts

Retirement planning for high net worth individuals demands a sophisticated approach to address complex financial landscapes and wealth preservation. Personalized strategies prove essential, as each affluent individual has unique goals, risk tolerances, and financial situations that require tailored solutions. Professional guidance becomes invaluable in this context, with wealth management teams providing comprehensive strategies to optimize retirement outcomes.

At Davies Wealth Management, we create customized retirement plans for high net worth individuals. Our approach combines in-depth financial analysis with a thorough understanding of our clients’ aspirations. We navigate the intricacies of tax planning, estate management, and investment strategies to help preserve and grow our clients’ wealth.

Proactive planning is key to achieving financial security in retirement. High net worth individuals should start early and regularly review their strategies to stay ahead of market changes, tax law updates, and shifts in personal circumstances. This forward-thinking approach, coupled with expert guidance, allows for the creation of a robust retirement plan that can withstand economic fluctuations and provide peace of mind.

Leave a Reply