“`html

At Davies Wealth Management, we understand the importance of maximizing your investment potential while minimizing your tax burden. Tax-advantaged investment strategies can be powerful tools in building long-term wealth and securing your financial future.

In this post, we’ll explore various tax-advantaged accounts and techniques to help you make the most of your investments. From traditional IRAs to advanced tax-efficient investing methods, we’ll provide practical insights to optimize your financial strategy.

Tax-Advantaged Investment Accounts: Your Path to Financial Growth

The Power of IRAs: Traditional vs. Roth

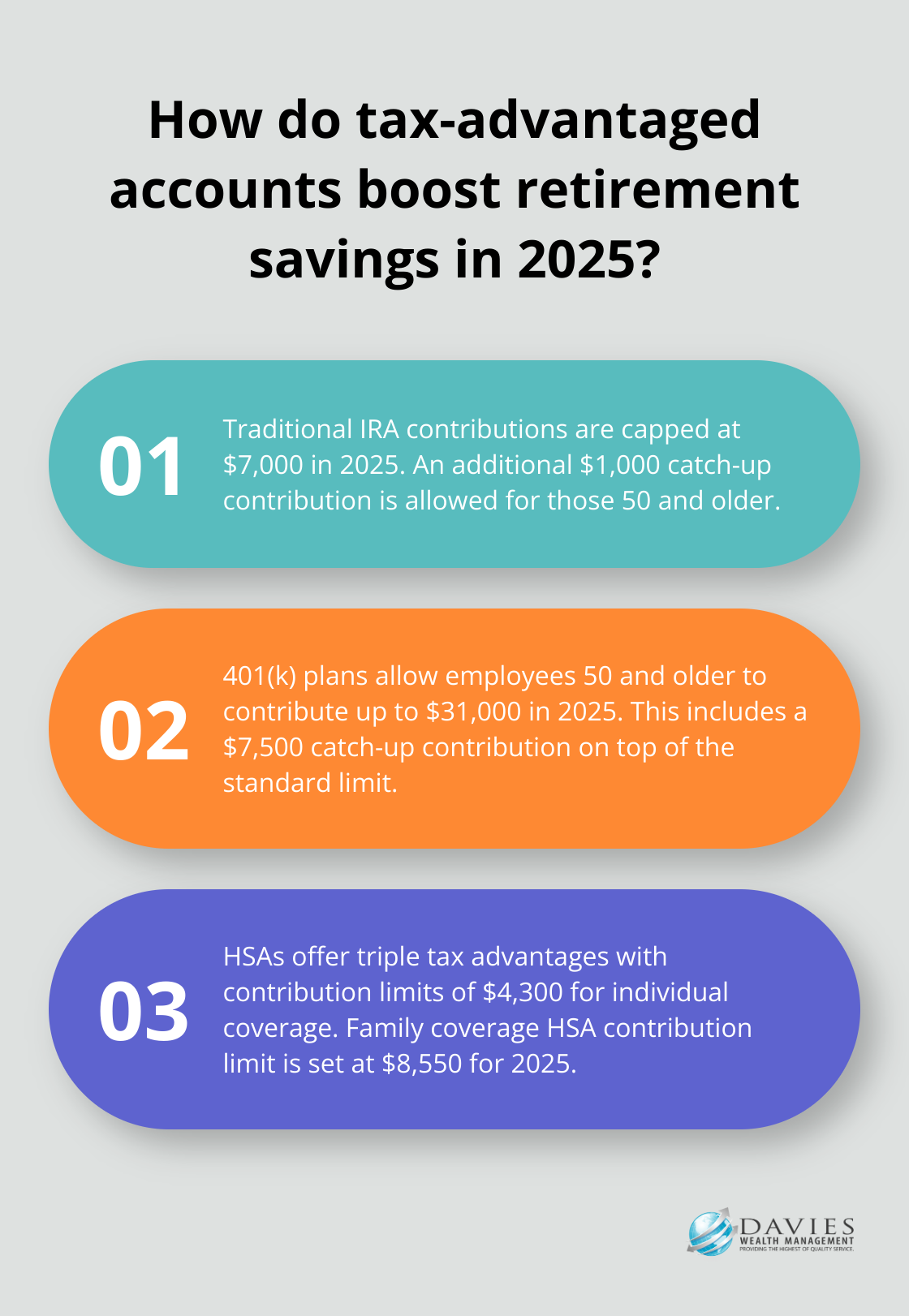

Individual Retirement Accounts (IRAs) offer significant tax advantages for investors. Traditional IRAs provide upfront tax deductions on contributions, with taxes paid upon withdrawal. In 2025, you can contribute up to $7,000 (plus an additional $1,000 if you’re 50 or older). This can result in substantial tax savings, particularly for high-income earners.

Roth IRAs, in contrast, use after-tax dollars but allow tax-free growth and withdrawals in retirement. These accounts appeal to those who anticipate a higher tax bracket in retirement.

401(k) Plans: Leveraging Employer Benefits

Employer-sponsored 401(k) plans form a cornerstone of many retirement strategies. Employees age 50 or older may contribute up to an additional $7,500 for a total of $31,000. Many employers offer matching contributions (essentially free money).

An often-overlooked strategy involves making after-tax contributions to a 401(k) beyond standard limits. This proves particularly beneficial if your plan permits in-service distributions or rollovers to a Roth IRA.

HSAs: The Triple Tax Advantage Powerhouse

Health Savings Accounts (HSAs) offer a unique triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. In 2025, you can contribute up to $4,300 if you are covered by a high-deductible health plan just for yourself, or $8,550 if you have coverage for your family.

HSAs also function as powerful investment vehicles. Once your HSA balance reaches a certain threshold (often around $1,000), you can invest the funds in various options, similar to an IRA. This allows for potential long-term growth, and unlike Flexible Spending Accounts (FSAs), HSA funds roll over year to year.

Some investors use HSAs strategically by paying current medical expenses out-of-pocket and allowing their HSA investments to grow tax-free for future healthcare costs in retirement. This approach can significantly boost long-term savings potential.

As we move forward, we’ll explore strategies to maximize these tax-advantaged investment accounts, ensuring you make the most of every opportunity to grow your wealth efficiently.

How to Maximize Tax-Advantaged Investment Strategies

Optimize Your Contributions

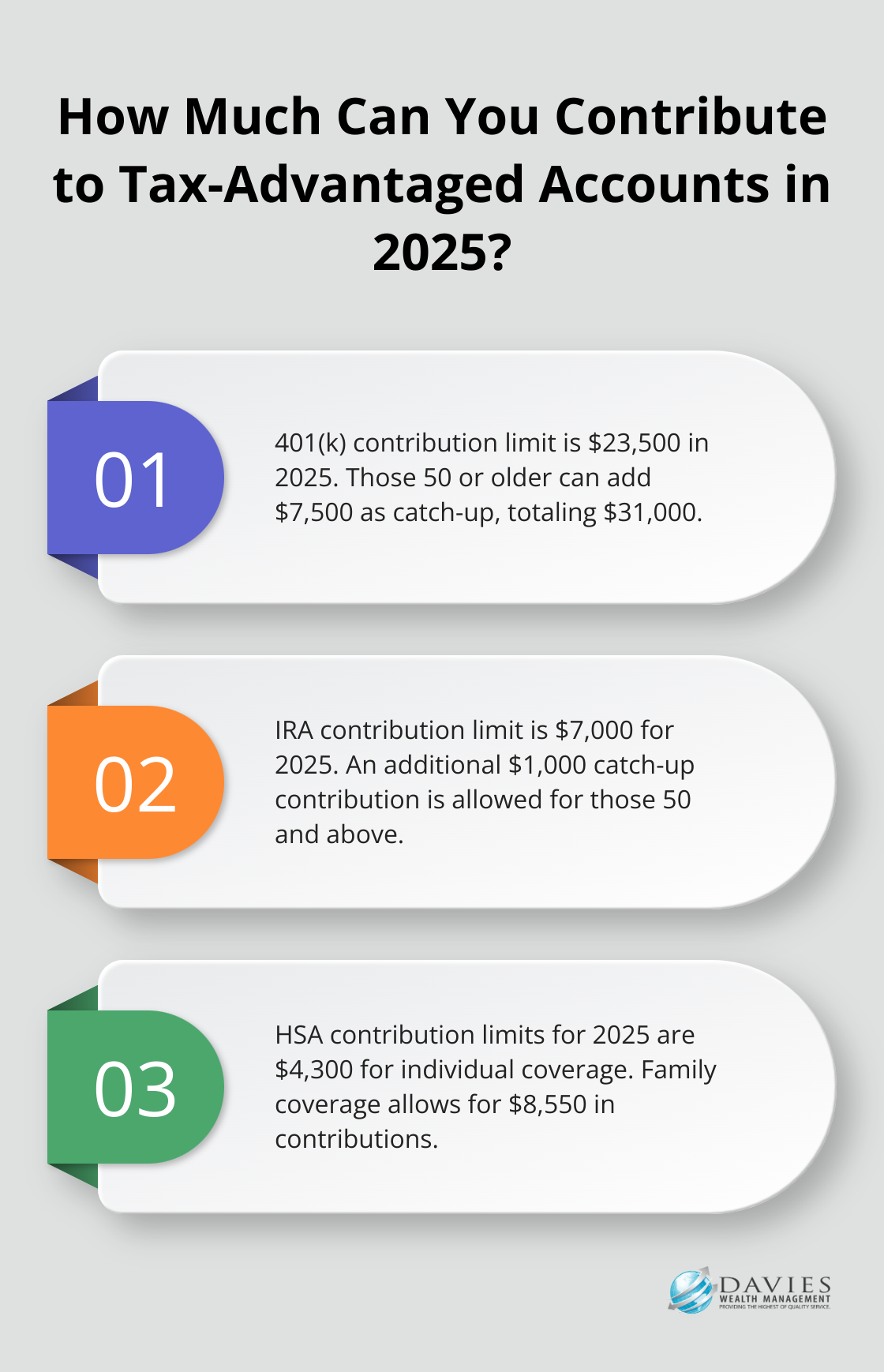

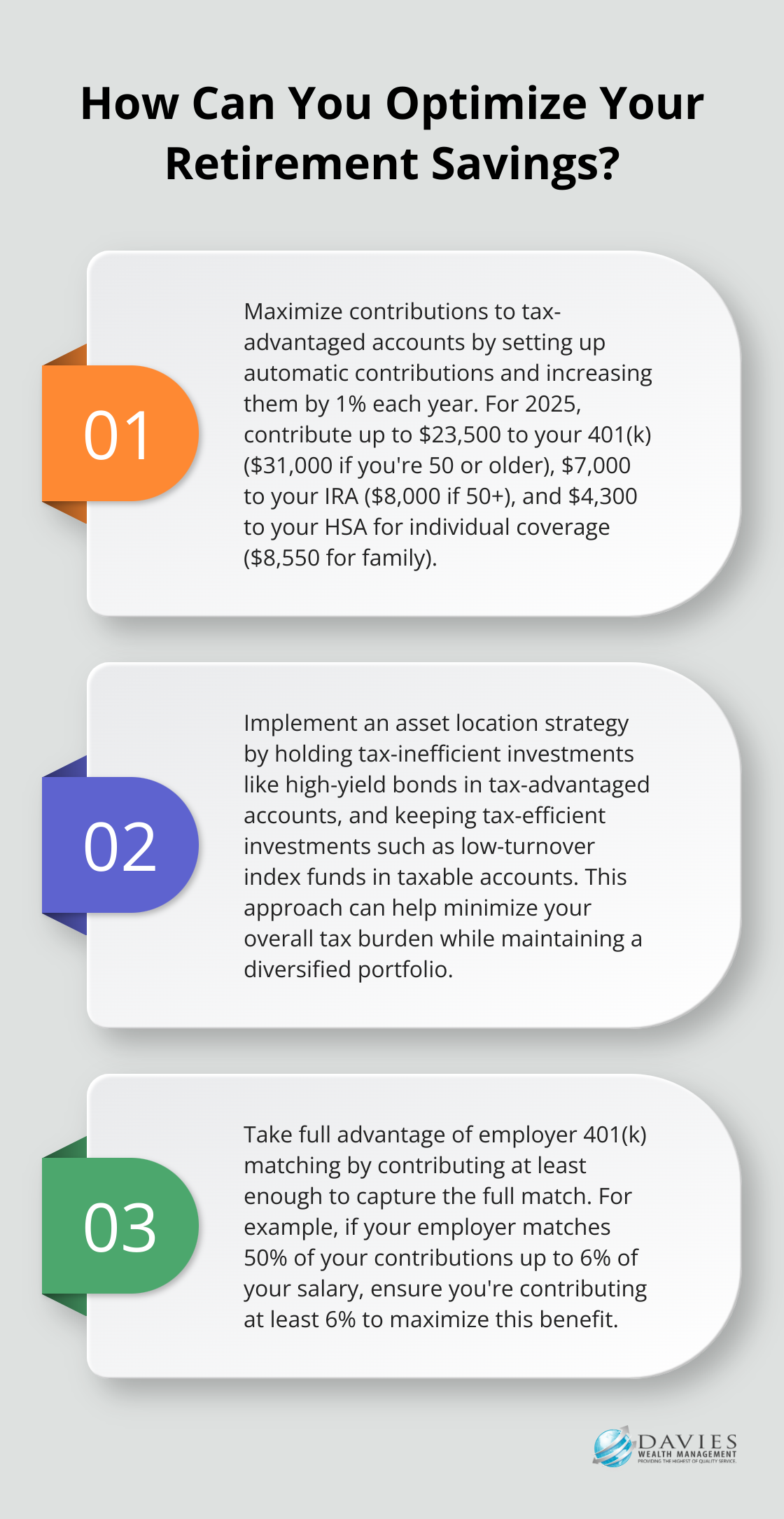

At Davies Wealth Management, we believe in empowering our clients to make the most of their tax-advantaged investment opportunities. One of the most straightforward ways to boost your tax-advantaged investments is to maximize your contributions. For 2025, the IRS has set the 401(k) contribution limit at $23,500. If you’re 50 or older, you can add an extra $7,500 as a catch-up contribution, bringing your total to $31,000.

For IRAs, the limit stands at $7,000, with an additional $1,000 catch-up contribution for those 50 and above. Don’t overlook HSAs either – in 2025, you can contribute up to $4,300 for individual coverage or $8,550 for family coverage.

We recommend setting up automatic contributions to ensure you consistently fund these accounts. If you can’t max out immediately, try to increase your contributions by 1% each year. This gradual approach can significantly impact your long-term savings without drastically affecting your current lifestyle.

Implement Strategic Asset Allocation

The placement of your investments across different account types can substantially impact your after-tax returns. We suggest implementing an asset location strategy for tax efficiency. This involves holding your most tax-inefficient investments (such as high-yield bonds or actively managed funds with frequent turnover) in tax-advantaged accounts like 401(k)s or traditional IRAs.

Conversely, consider keeping more tax-efficient investments, such as low-turnover index funds or municipal bonds, in taxable accounts. This strategy can help minimize your overall tax burden while maintaining a diversified portfolio.

For example, if you’re in a high tax bracket, it might make sense to hold dividend-paying stocks in a Roth IRA. This way, you can reinvest dividends without immediate tax consequences and potentially enjoy tax-free growth over the long term.

Harness the Power of Employer Matching

If your employer offers a 401(k) match, it’s important to take full advantage of this benefit. According to a survey, the average 401(k) match is 4.7% of salary. This is essentially free money that can significantly boost your retirement savings.

Let’s say you earn $75,000 annually, and your employer matches 50% of your contributions up to 6% of your salary. If you contribute 6% ($4,500), your employer will add an additional $2,250 to your account. Over 30 years, assuming a 7% annual return, this employer match alone could grow to over $200,000.

We always advise our clients to contribute at least enough to their 401(k) to capture the full employer match. If you’re not sure about your company’s matching policy, reach out to your HR department for clarification.

Consider Advanced Tax-Efficient Techniques

While maximizing contributions and employer matching form the foundation of tax-advantaged investing, there are more advanced strategies to consider. These techniques can further optimize your tax situation and potentially increase your overall returns. In the next section, we’ll explore some of these advanced tax-efficient investing methods, including tax-loss harvesting, municipal bonds, and Roth conversion strategies.

Advanced Tax Strategies for Savvy Investors

At Davies Wealth Management, we strive to help our clients optimize their tax situation and maximize their investment returns. This chapter explores advanced tax-efficient investing techniques that can elevate your financial strategy.

Tax-Loss Harvesting: A Powerful Tool

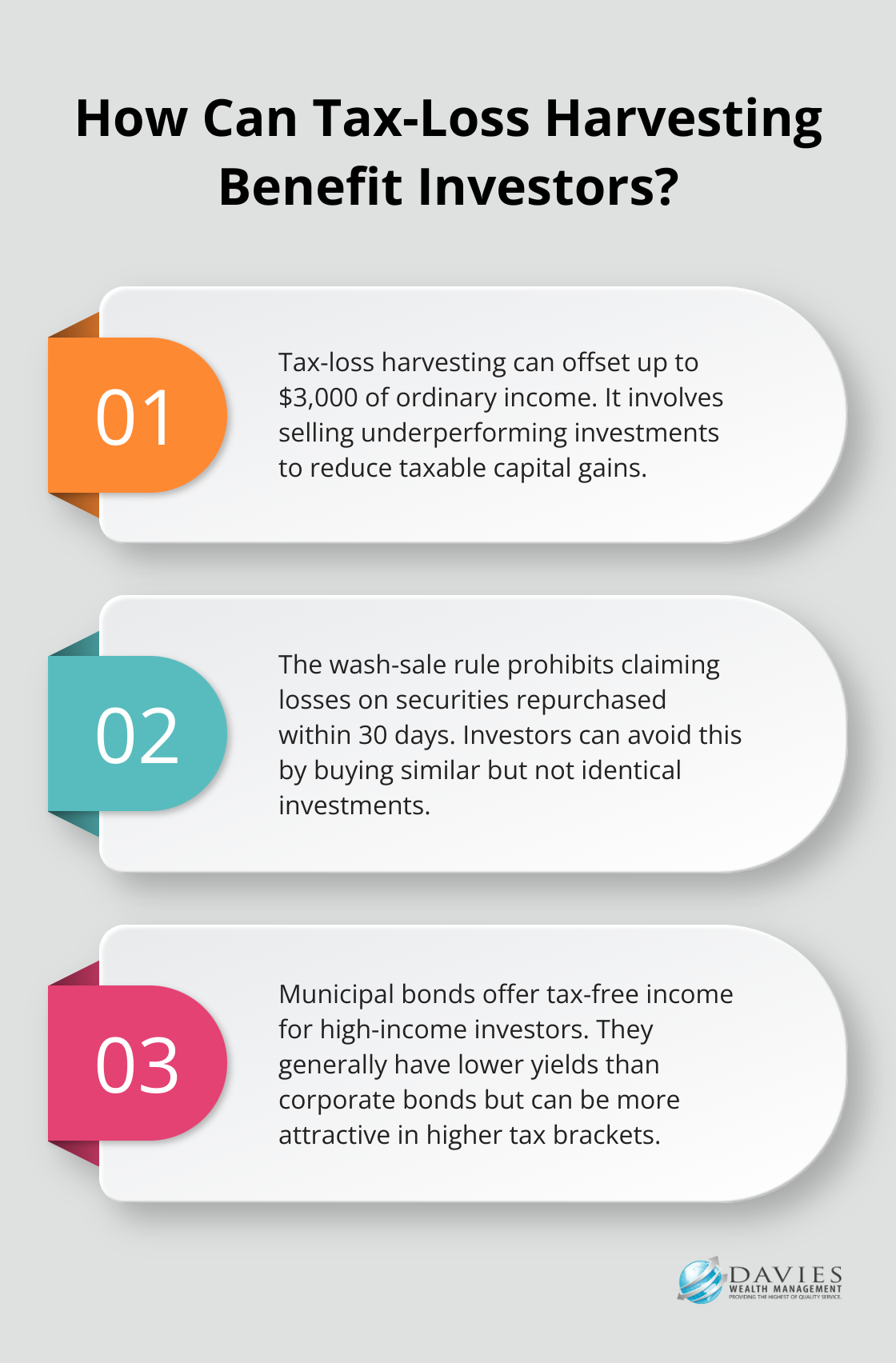

Tax-loss harvesting involves selling an investment that’s underperforming and losing money. You then use that loss to reduce your taxable capital gains and potentially offset up to $3,000 of ordinary income.

Consider this scenario: You own a stock that has decreased in value. You could sell it and use the loss to offset gains from other investments. You then reinvest the proceeds in a similar (but not identical) investment to maintain your portfolio allocation.

Be aware of the wash-sale rule, which prohibits claiming a loss on a security if you buy the same or a substantially identical security within 30 days before or after the sale. To avoid this, invest in a different company in the same sector or a similar ETF that tracks a different index.

Municipal Bonds: Tax-Free Income Generator

Municipal bonds can enhance a tax-efficient portfolio, especially for high-income investors. In general, tax-exempt municipal bonds are more attractive to those in higher tax brackets. To compare municipal bonds to taxable bonds, you need to consider your tax situation.

However, consider your overall investment strategy and risk tolerance. Municipal bonds generally offer lower yields than corporate bonds, so they may not suit all investors or all portions of your portfolio.

Roth Conversion Strategies: Managing Future Tax Liability

Roth conversions can effectively manage your tax liability in retirement. This strategy converts traditional IRA or 401(k) assets to a Roth IRA, paying taxes on the converted amount now in exchange for tax-free growth and withdrawals in the future.

A Roth conversion ladder describes the strategy of moving funds from a pretax retirement account to a Roth IRA in smaller increments over multiple years. This strategy works particularly well if you expect to be in a higher tax bracket in retirement than you are now.

High-income earners ineligible for direct Roth IRA contributions can use the backdoor Roth IRA strategy as an effective workaround. This involves making a non-deductible contribution to a traditional IRA and then immediately converting it to a Roth IRA. However, be mindful of the pro-rata rule, which can complicate this strategy if you have existing pre-tax IRA balances.

These advanced tax strategies can offer significant benefits, but they also come with complexities and potential pitfalls. Consult with a qualified financial advisor (such as Davies Wealth Management) and tax professional before implementing any of these strategies to ensure they align with your overall financial goals.

Final Thoughts

Tax-advantaged investment strategies offer powerful tools for building long-term wealth and securing your financial future. From maximizing contributions to retirement accounts to leveraging HSAs, each strategy presents unique opportunities to optimize investments while minimizing tax burdens. Advanced techniques such as tax-loss harvesting and Roth conversion strategies provide additional layers of tax optimization and potentially increase overall investment returns.

Your financial situation, goals, and risk tolerance are unique, which makes personalized financial planning important. At Davies Wealth Management, we craft tailored financial strategies that align with individual needs and objectives. Our team of experts can help you navigate the intricacies of tax-advantaged investment strategies (ensuring you make the most of every opportunity to grow and protect your wealth).

We encourage you to take the next step in optimizing your financial future. Consult with a financial advisor who can provide personalized guidance and help you implement these strategies effectively. With the right approach and expert advice, you can work towards achieving your financial goals while maximizing tax efficiency.

“`

Leave a Reply