At Davies Wealth Management, we understand that creating tax-efficient retirement strategies is a critical aspect of financial planning. Taxes can significantly impact your retirement savings, potentially reducing your hard-earned nest egg.

We’ve designed this guide to help you navigate the complexities of tax planning in retirement and maximize your savings. By implementing smart tax strategies, you can keep more of your money working for you throughout your golden years.

What Are Tax-Efficient Retirement Strategies?

Definition and Importance

Tax-efficient retirement strategies are financial plans that minimize your tax burden during retirement. These strategies maximize your after-tax income, allowing you to keep more of your savings. Tax planning plays a vital role in retirement for everyone, not just high-income earners or the wealthy. Without proper planning, you might pay more in taxes than necessary, potentially depleting your retirement savings faster than anticipated.

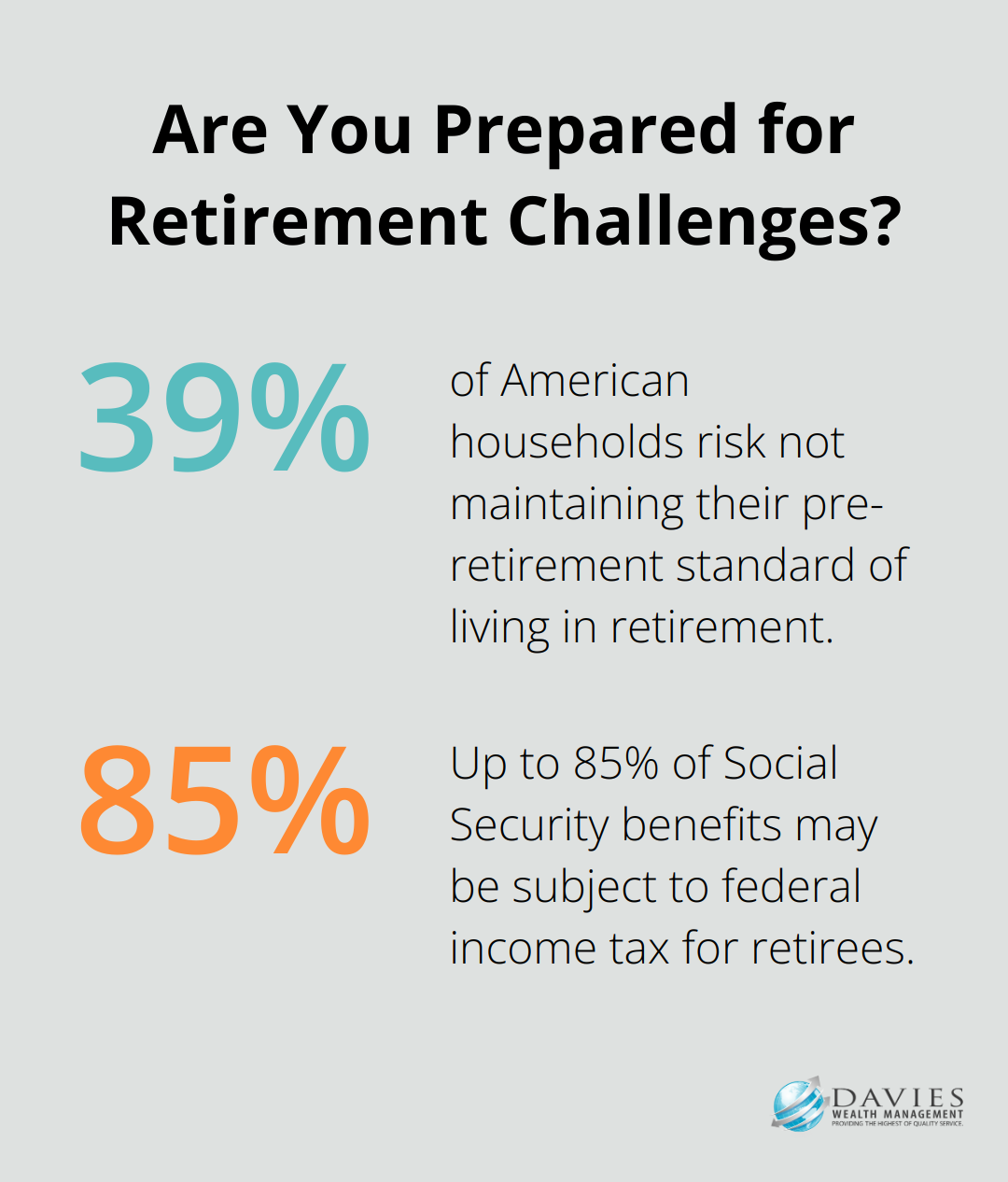

A study by the National Retirement Risk Index reveals that 39% of American households risk not maintaining their pre-retirement standard of living in retirement. Effective tax planning helps mitigate this risk by preserving more of your retirement income.

Common Tax Challenges in Retirement

Retirees face several tax challenges that can erode their savings if not properly managed:

- Required Minimum Distributions (RMDs): The RMD rules require individuals to take withdrawals from their IRAs (including SIMPLE IRAs and SEP IRAs) every year once they reach age 72 (73 if the account owner turns 72 after December 31, 2022). These distributions are taxed as ordinary income and can push retirees into higher tax brackets.

- Social Security Benefit Taxation: Depending on your total income, up to 85% of your Social Security benefits may be subject to federal income tax. This often surprises retirees who haven’t planned for this additional tax burden.

Effective Tax-Efficient Strategies

Diversifying Retirement Accounts

One effective strategy involves balancing your savings between tax-deferred accounts (like traditional IRAs), tax-free accounts (like Roth IRAs), and taxable accounts. This diversity gives you more control over your taxable income in retirement.

Strategic Roth IRA Conversions

Roth conversions can be a powerful tool. Converting portions of your traditional IRA to a Roth IRA during lower-income years can reduce your future RMDs and potentially lower your overall tax liability in retirement.

Professional Athlete Example

For instance, a professional athlete client benefited from a tax-efficient retirement plan that accounted for high-income years during their playing career and the transition to retirement. Strategic use of Roth conversions and diversifying retirement accounts significantly reduced their projected tax burden in retirement.

The Value of Professional Guidance

While these strategies can be powerful, they’re also complex. Tax laws change frequently, and what works for one person may not be optimal for another. Working with experienced professionals who can tailor these strategies to your unique situation is essential.

As we move forward, we’ll explore specific tax-efficient retirement strategies in more detail, providing you with actionable insights to optimize your retirement planning.

Maximizing Your Retirement Savings Through Tax-Efficient Strategies

At Davies Wealth Management, we’ve observed how the right tax-efficient strategies can significantly boost retirement savings. Let’s explore some powerful tactics that can help you keep more of your hard-earned money.

The Power of Account Diversification

Diversifying your retirement accounts forms a cornerstone of tax efficiency. Spreading your savings across traditional IRAs, Roth IRAs, and 401(k)s creates flexibility in managing your tax liability during retirement. For example, having both traditional and Roth accounts allows you to strategically withdraw from either tax-deferred or tax-free sources, depending on your current tax situation.

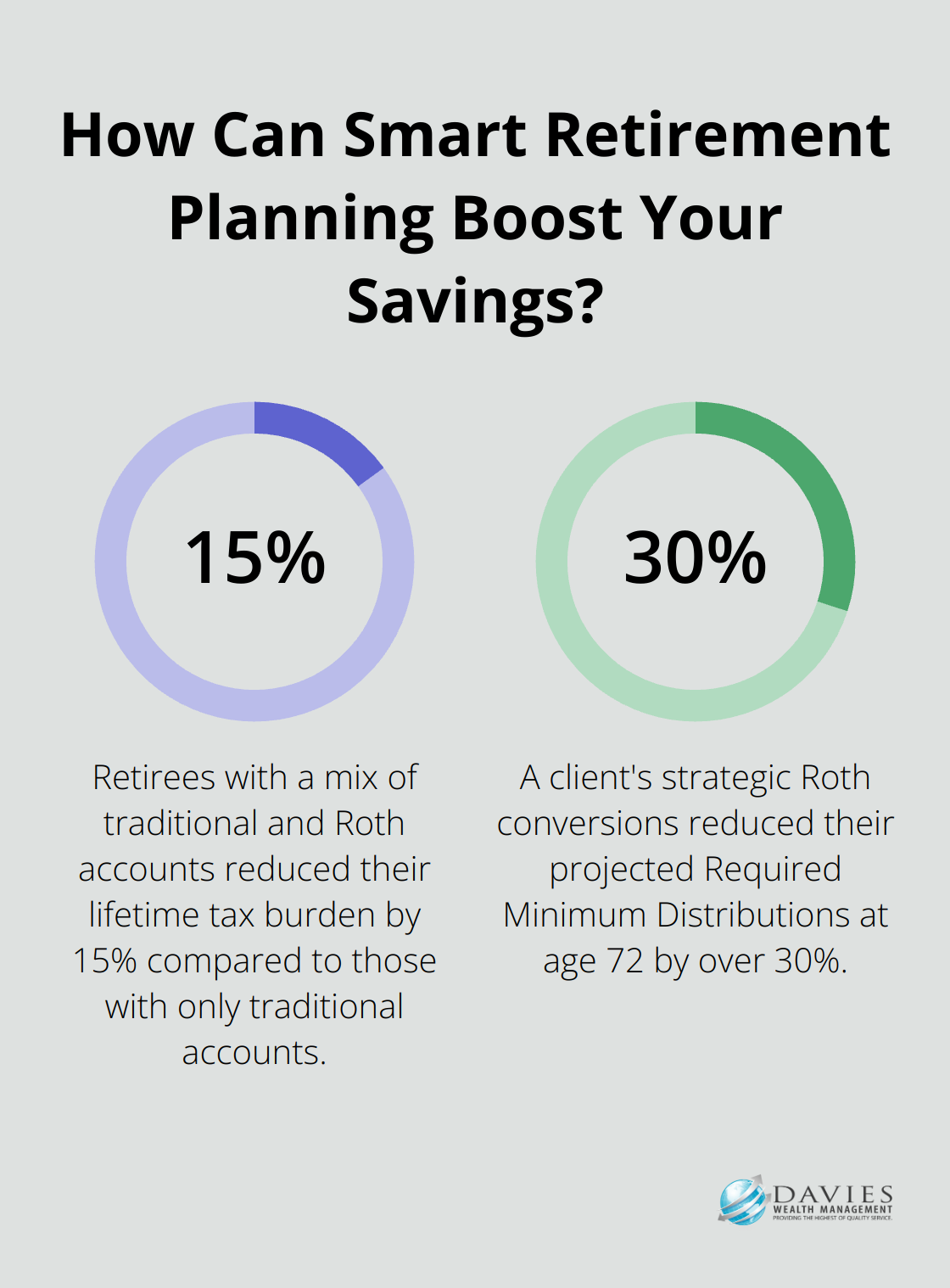

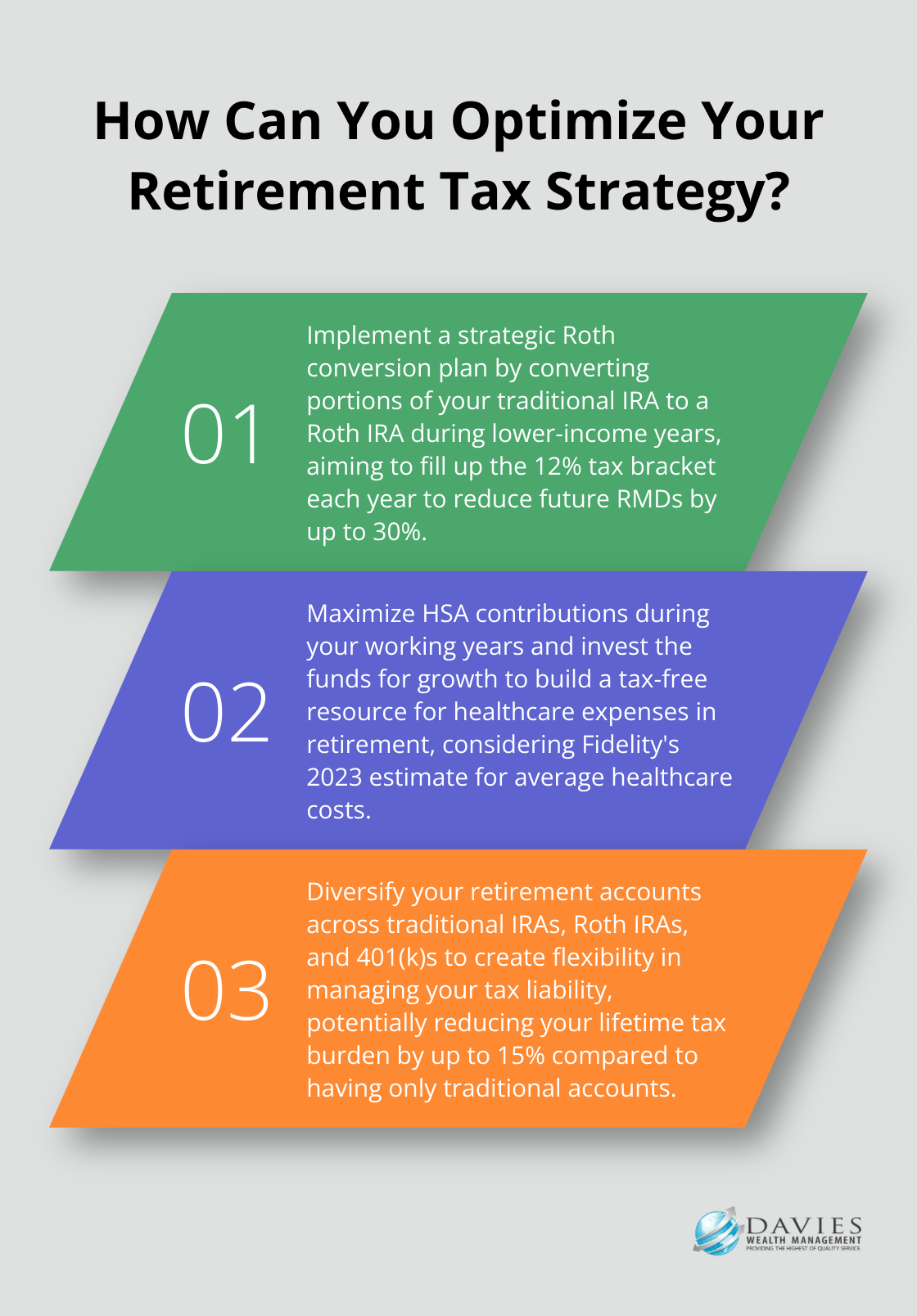

A study by the Employee Benefit Research Institute found that retirees with a mix of traditional and Roth accounts reduced their lifetime tax burden by up to 15% compared to those with only traditional accounts. This translates to thousands of dollars in savings over the course of retirement.

Strategic Roth Conversions

Roth conversions can transform many retirees’ financial situations. Converting portions of your traditional IRA to a Roth IRA during lower-income years can potentially reduce your future Required Minimum Distributions (RMDs) and overall tax liability.

For instance, a client who retired at 62 with a significant traditional IRA balance implemented a series of Roth conversions over five years, filling up the 12% tax bracket each year. This strategy reduced their projected RMDs at age 72 by over 30%, lowered their future tax burden, and provided more tax-free growth potential.

Optimizing Withdrawal Strategies

The order in which you withdraw from your retirement accounts can substantially impact your tax liability. A common strategy starts with taxable accounts, then moves to tax-deferred accounts, and finally taps into tax-free accounts like Roth IRAs.

However, this approach doesn’t fit everyone. A more nuanced strategy often involves taking distributions from multiple account types each year to manage your tax bracket. You might withdraw enough from your traditional IRA to fill up the lower tax brackets, then supplement with tax-free Roth withdrawals to meet additional income needs.

Leveraging Health Savings Accounts

Health Savings Accounts (HSAs) offer unparalleled tax benefits but are often overlooked as retirement savings vehicles. An HSA offers triple tax savings, where you can contribute pre-tax dollars, pay no taxes on earnings, and withdraw the money tax-free now or in retirement.

Fidelity’s 2023 estimate remains the same as last year for average healthcare costs in retirement for a couple retiring at 65. Maximizing HSA contributions during your working years and investing the funds for growth can build a substantial tax-free resource for healthcare expenses in retirement.

Embracing Tax-Efficient Investments

The types of investments you hold can significantly impact your tax liability. Municipal bonds provide tax-free interest income at the federal level (and often at the state level for residents). For taxable accounts, consider low-turnover index funds or ETFs, which typically generate fewer taxable events than actively managed funds.

Strategic asset location can reduce tax burden through placing tax-inefficient investments in tax-advantaged accounts and tax-efficient investments in taxable accounts.

These strategies require careful planning and ongoing management. While the potential tax savings are substantial, it’s important to tailor these approaches to your unique financial situation. Professional guidance can help you navigate the complexities of tax-efficient retirement planning and maximize your savings for a more secure future. In the next section, we’ll explore how working with a financial advisor can further enhance your retirement strategy.

Navigating Tax-Efficient Retirement with Expert Guidance

The Power of Professional Financial Advice

Creating a tax-efficient retirement strategy requires deep knowledge of tax laws, investment vehicles, and retirement planning principles. While the strategies we’ve discussed can significantly impact your retirement savings, their effective implementation often demands professional expertise.

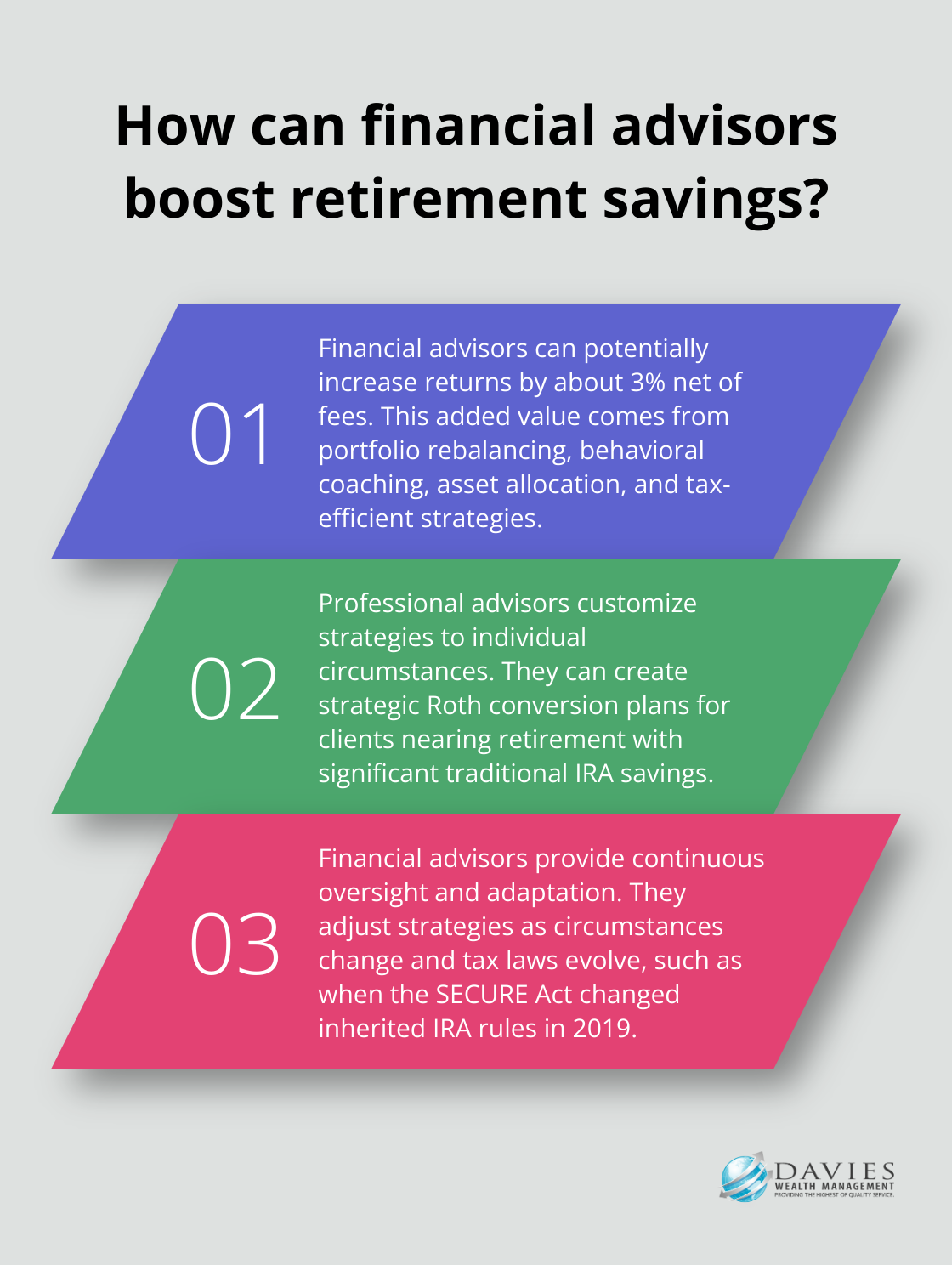

Financial advisors offer valuable knowledge and experience. They keep up with changing tax laws and regulations, which is essential for optimizing retirement strategies. A study by Vanguard suggests that working with a financial advisor can potentially increase returns by about 3% net of fees. This added value stems from portfolio rebalancing, behavioral coaching, asset allocation, and tax-efficient strategies.

Customizing Strategies to Individual Needs

Tax-efficient retirement planning doesn’t follow a one-size-fits-all approach. Each person’s financial situation, goals, and risk tolerance are unique. Professional advisors can customize strategies to your specific circumstances.

For example, a client nearing retirement with significant savings in a traditional IRA might benefit from a strategic Roth conversion plan. Converting assets early in retirement before you face required minimum distributions (RMDs) can reduce those RMDs and the risk that they will push you into a higher tax bracket.

Continuous Management and Adaptation

Tax-efficient retirement planning isn’t a static process. It requires ongoing management and adaptation as circumstances change and tax laws evolve. Professional advisors provide continuous oversight, adjusting strategies to keep them aligned with your goals and the current tax environment.

When the SECURE Act changed the rules around inherited IRAs in 2019, proactive advisors reviewed and adjusted their clients’ estate plans to ensure wealth transfer strategies remained tax-efficient under the new laws. Beneficiaries of an IRA, and most plans, have the option of taking a lump-sum distribution of the inherited account at any time.

Coordinating with Other Professionals

Effective tax planning often requires coordination with other professionals, such as accountants and estate planning attorneys. Financial advisors can act as the quarterback of your financial team, ensuring all aspects of your financial plan work together seamlessly.

Leveraging Specialized Expertise

For individuals with unique financial situations (like professional athletes or business owners), working with advisors who have specialized expertise can be particularly beneficial. These advisors understand the specific challenges and opportunities in these areas and can craft highly tailored strategies.

Professional athletes, for instance, face unique tax implications due to their often-fluctuating incomes. Experienced advisors can implement strategies to smooth out tax liabilities over time, potentially saving significant amounts in taxes over the course of their careers and into retirement.

Final Thoughts

Creating tax-efficient retirement strategies requires a personalized approach tailored to your unique financial situation and goals. Professional guidance proves invaluable in navigating complex tax laws and developing effective strategies to minimize your tax burden during retirement. At Davies Wealth Management, we specialize in crafting customized financial plans that address the distinct needs of our clients, including professional athletes with unique financial challenges.

Our expertise in tax-efficient strategies and comprehensive retirement planning can help you navigate financial management complexities. We strive to maximize your overall financial well-being in retirement, potentially allowing you to keep more of your hard-earned money and ensure a steady income stream throughout your golden years.

Take the first step towards a tax-efficient retirement today and set yourself up for financial success. Our team stands ready to assist you in developing a tailored strategy that aligns with your specific goals and circumstances (including tax optimization techniques).

✅ BOOK AN APPOINTMENT TODAY: https://davieswealth.tdwealth.net/appointment-page

===========================================================

SEE ALL OUR LATEST BLOG POSTS: https://tdwealth.net/articles

If you like the content, smash that like button! It tells YouTube you were here, and the Youtube algorithm will show the video to others who may be interested in content like this. So, please hit that LIKE button!

Don’t forget to SUBSCRIBE here: https://www.youtube.com/channel/UChmBYECKIzlEBFDDDBu-UIg

✅ Contact me: TDavies@TDWealth.Net

====== ===Get Our FREE GUIDES ==========

Retirement Income: The Transition into Retirement: https://davieswealth.tdwealth.net/retirement-income-transition-into-retirement

Beginner’s Guide to Investing Basics: https://davieswealth.tdwealth.net/investing-basics

✅ Want to learn more about Davies Wealth Management, follow us here!

Website:

Podcast:

Social Media:

https://www.facebook.com/DaviesWealthManagement

https://twitter.com/TDWealthNet

https://www.linkedin.com/in/daviesrthomas

https://www.youtube.com/c/TdwealthNetWealthManagement

Lat and Long

27.17404889406371, -80.24410438798957

Davies Wealth Management

684 SE Monterey Road

Stuart, FL 34994

772-210-4031

#Retirement #FinancialPlanning #wealthmanagement

DISCLAIMER

The content provided by Davies Wealth Management is intended solely for informational purposes and should not be considered as financial, tax, or legal advice. While we strive to offer accurate and timely information, we encourage you to consult with qualified retirement, tax, or legal professionals before making any financial decisions or taking action based on the information presented. Davies Wealth Management assumes no liability for actions taken without seeking individualized professional advice.

Leave a Reply