“`html

At Davies Wealth Management, we understand that retirement planning isn’t a one-size-fits-all approach. Your investment strategy should evolve as you age, reflecting your changing financial goals and risk tolerance.

This guide explores retirement investment strategies by age, helping you make informed decisions at every stage of your career. We’ll walk you through key considerations for each decade, from your early working years to the cusp of retirement.

How to Kickstart Your Retirement Savings in Your 20s and 30s

Your 20s and 30s provide the perfect opportunity to build a solid foundation for retirement. At Davies Wealth Management, we often observe young professionals who underestimate the power of early investing. Starting early gives you a significant advantage due to compound interest.

Maximize Workplace Retirement Plans

One of the most effective ways to jumpstart your retirement savings is through your employer’s 401(k) plan. If your company offers a match, contribute at least enough to get the full match – it’s essentially free money. For example, if your employer matches 50% of your contributions up to 6% of your salary, you should contribute at least 6% to maximize this benefit.

In 2025, the contribution limit for 401(k) plans stands at $23,500. While maxing out might not be feasible for everyone, try to increase your contributions gradually. Even a 1% increase each year can make a substantial difference over time.

Focus on Growth-Oriented Investments

In your 20s and 30s, time is on your side to weather market volatility. This allows you to focus on growth-oriented investments, primarily stocks. A portfolio heavily weighted towards equities has historically outperformed more conservative allocations over long periods.

Consider allocating a larger portion of your portfolio to stocks, with the remainder in bonds. This aggressive approach can potentially yield higher returns (though it comes with increased short-term volatility). You’re investing for decades, not days.

Use Tax-Advantaged Accounts

While 401(k)s are excellent, they’re not the only option. Individual Retirement Accounts (IRAs) offer additional tax advantages and investment options. For many young professionals, a Roth IRA is particularly attractive.

Roth IRAs are funded with after-tax dollars, but your earnings grow tax-free, and you can withdraw them tax-free in retirement. This can be especially beneficial if you expect to be in a higher tax bracket later in life. In 2025, you can contribute up to $8,000 to a Roth IRA if you’re age 50 or older (if you meet the income requirements).

Start Small, But Start Now

If the idea of setting aside large sums for retirement seems daunting, keep in mind that even small contributions can grow significantly over time. For instance, investing just $100 per month starting at age 25 could potentially grow to over $150,000 by age 65 (assuming a 7% annual return).

Consistent, early investing can lead to substantial wealth accumulation. Implementing these strategies in your 20s and 30s sets you up for a more secure financial future. As you progress through your career and your financial situation evolves, it’s important to adjust your investment strategy accordingly. Let’s explore how your approach should shift as you enter your 40s and 50s.

Maximizing Your Peak Earning Years: Retirement Planning in Your 40s and 50s

Boost Your Savings Rate

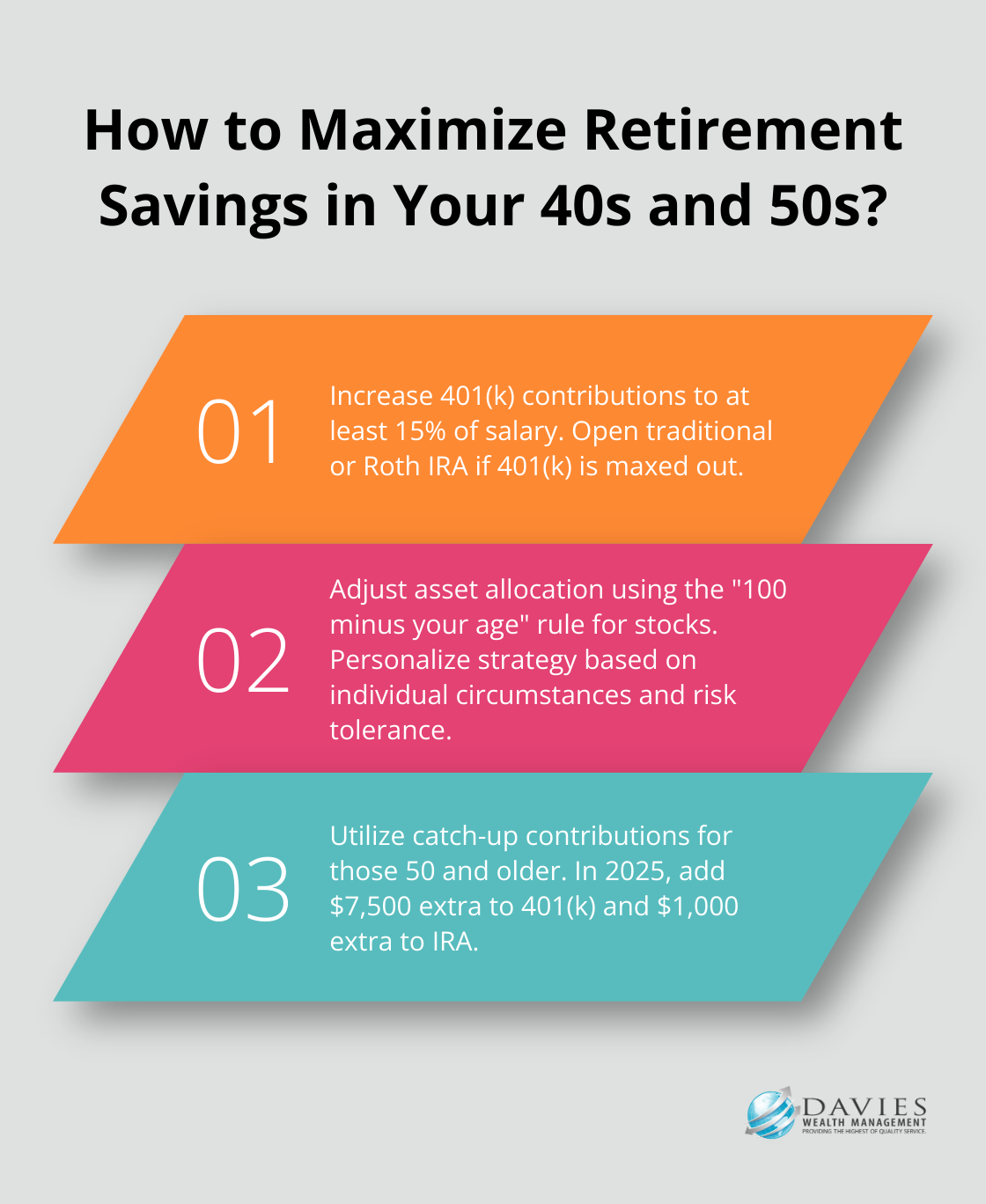

Your 40s and 50s often represent your highest earning potential. This period presents a prime opportunity to significantly increase your retirement savings. The 34th annual Retirement Confidence Survey (RCS) shows that younger workers are as likely to have taken certain steps to prepare for retirement as older workers. If you fall short of recommended benchmarks, now is the time to catch up.

We recommend you increase your 401(k) contributions to at least 15% of your salary (including any employer match). If you already max out your 401(k), consider opening a traditional IRA or a Roth IRA (if eligible) to further enhance your savings.

Rebalance Your Portfolio

As retirement approaches, it’s important to gradually adjust your investment strategy. While you still have time to recover from market fluctuations, you may want to start reducing your risk exposure. A common rule of asset allocation by age is that you should hold a percentage of stocks that is equal to 100 minus your age.

However, this is merely a starting point. Your ideal asset allocation depends on your individual circumstances, risk tolerance, and financial objectives. A personalized investment strategy will align best with your unique situation.

Leverage Catch-Up Contributions

For individuals 50 or older, the IRS permits additional “catch-up” contributions to retirement accounts. In 2025, you can contribute an extra $7,500 to your 401(k) on top of the standard $23,500 limit. For IRAs, you can add an extra $1,000 to the standard $8,000 limit.

These catch-up contributions can substantially boost your retirement savings. For example, if you maximize your 401(k) (including catch-up contributions) from age 50 to 65, you could potentially add over $450,000 to your retirement savings (assuming a 7% annual return).

Consider Long-Term Care Insurance

While it may seem early, your 50s provide an ideal time to explore long-term care insurance options. Most long-term care insurance claims begin when the policyholder is in their 80s or older, with half beginning between ages 80 and 89. Earlier purchase often means lower premiums and a higher likelihood of approval.

Long-term care costs can be substantial. Genworth’s 2021 Cost of Care Survey reveals that the median annual cost for a private room in a nursing home is $108,405. Having a plan in place can protect your retirement savings from potential depletion due to these expenses.

As you navigate these critical years, it’s essential to make the most of your peak earning potential and set yourself up for a comfortable retirement. The next phase of your journey involves fine-tuning your portfolio as you approach retirement age. Let’s explore how to adjust your strategy for this important milestone.

How to Safeguard Your Nest Egg Near Retirement

Reassess Your Risk Tolerance

As you approach retirement, your investment strategy must evolve. The transition from wealth accumulation to preservation becomes paramount. In your late 50s and early 60s, you need to reevaluate your risk tolerance. While growth remains necessary to combat inflation, capital preservation takes center stage.

Maximizing contributions to retirement accounts, exploring catch-up contribution options, and considering delaying retirement or working part-time during early retirement can be effective strategies to safeguard your nest egg.

Focus on Income-Generating Investments

Near retirement, you should prioritize investments that provide regular income. Diversifying with low-risk options such as Treasury bonds, CDs, and municipal bonds can offer stability and tax benefits.

Embrace Diversification

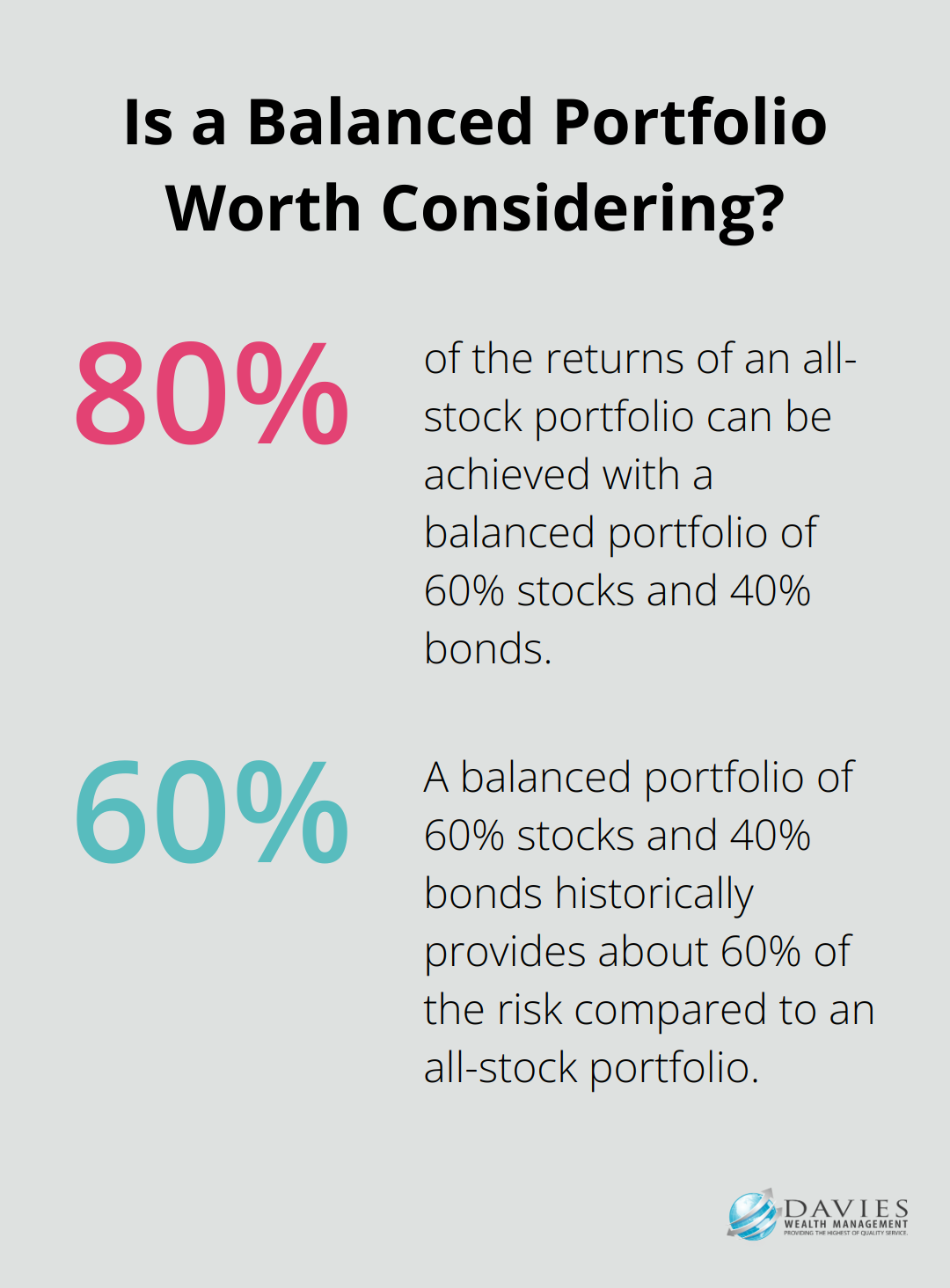

Diversification becomes even more critical as retirement approaches. A well-diversified portfolio can help mitigate risk while still offering growth opportunities. This might include a mix of domestic and international stocks, bonds of varying durations, and alternative investments like real estate or commodities.

Research shows that a balanced portfolio of 60% stocks and 40% bonds has historically provided about 80% of the returns of an all-stock portfolio with only about 60% of the risk.

Consider Guaranteed Income Options

Annuities can provide a guaranteed income stream in retirement, which proves valuable if you worry about outliving your savings. While annuities can be complex and involve fees, they offer peace of mind for some retirees.

Regular Review and Adjustment

Your financial situation and goals may change as you near retirement. You must regularly review and adjust your strategy to ensure it aligns with your current needs and future aspirations. Professional guidance can prove invaluable during this critical transition period.

Final Thoughts

Tailoring retirement investment strategies by age empowers individuals to build a secure financial future. Your approach should evolve from aggressive growth in your younger years to a more balanced portfolio in middle age, and finally to preservation and income generation as you near retirement. This dynamic strategy maximizes growth potential when time is on your side and protects your wealth as you approach your golden years.

Regular portfolio reviews ensure your investments align with your changing life circumstances and financial goals. As you progress through different life stages, your risk tolerance, income needs, and time horizon will shift. Consistent reassessment and adjustment of your investment strategy help you stay on track to meet your retirement objectives.

Working with a financial advisor provides invaluable guidance throughout your retirement planning journey. At Davies Wealth Management, we create personalized investment strategies that adapt to your unique needs at every stage of life. Our expertise in retirement planning can help you navigate complex financial decisions, optimize tax strategies (including catch-up contributions), and keep your portfolio aligned with your long-term goals.

“`

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

Leave a Reply