At Davies Wealth Management, we understand that creating a comprehensive financial planning checklist is essential for achieving your financial goals.

A well-structured checklist serves as a roadmap, guiding you through the complex landscape of personal finance.

This blog post will walk you through the key components of a robust financial planning checklist, helping you take control of your financial future.

Where Do You Stand Financially?

Calculating Your Net Worth

The first step in creating a comprehensive financial plan is to get a clear picture of your current financial situation. This assessment forms the foundation for all future financial decisions and strategies. Calculating Your Net Worth involves listing your assets (what you own), estimating the value of each, and adding up the total. Then, list your liabilities (what you owe) and add up the outstanding amounts. Subtract your total liabilities from your total assets to determine your net worth. This number gives you a snapshot of your overall financial health.

Income and Expense Review

Take a deep dive into your cash flow. Track all sources of income, including salary, bonuses, investment returns, and any side hustles. Then, meticulously record all your expenses for at least three months. This exercise often reveals surprising spending patterns. Many people are shocked to discover how much they spend on dining out or subscription services (which can add up to hundreds of dollars per month).

Debt and Credit Analysis

Examine your debt closely. List all outstanding balances, interest rates, and minimum payments. Pay special attention to high-interest debt, as it can significantly increase the overall cost of borrowing money, and compound interest payments can significantly increase your debt over time. Also, check your credit score and report.

Savings and Investment Evaluation

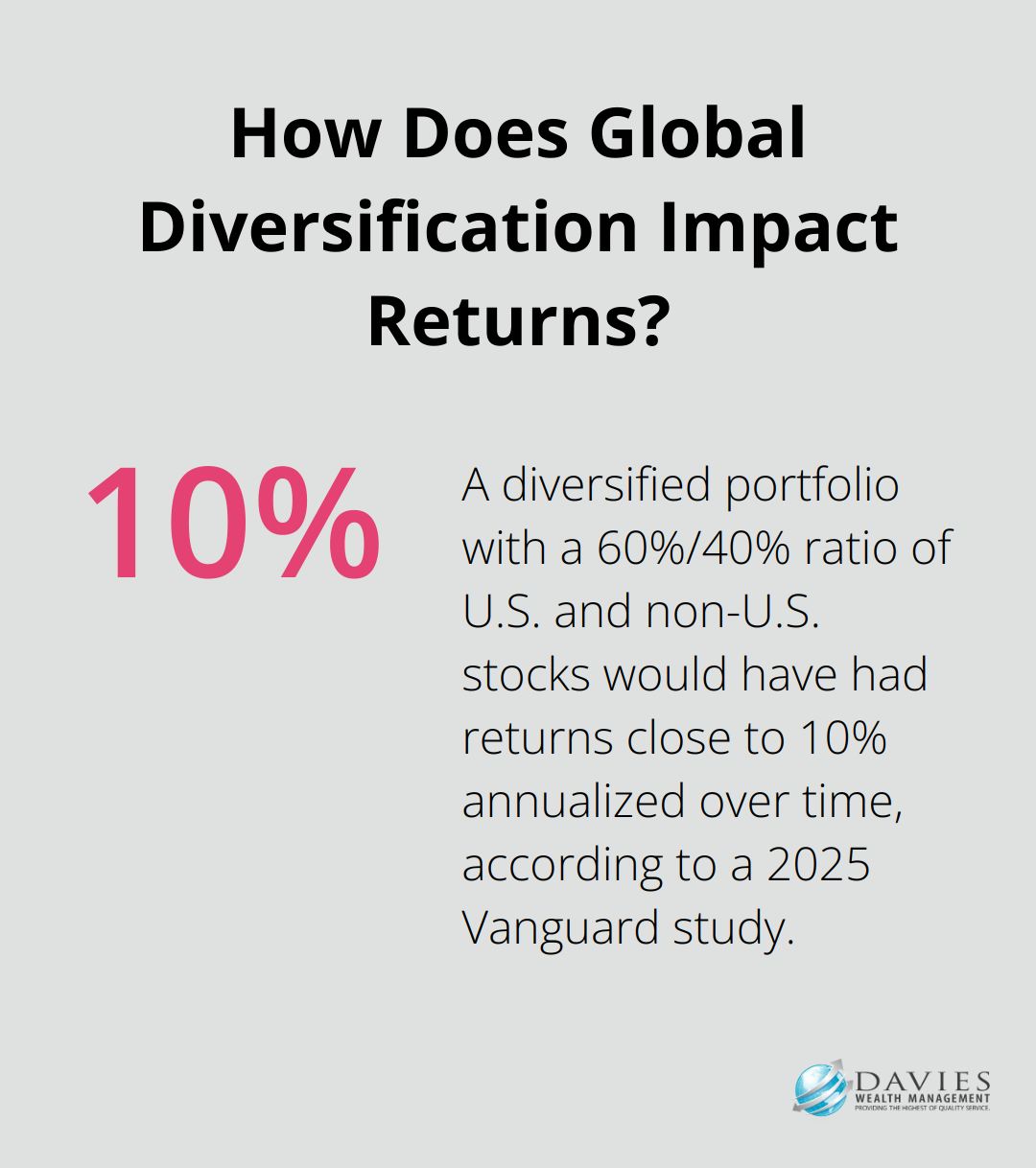

Assess your current savings and investments. How much do you have in your emergency fund? Are you maximizing your retirement contributions? Review your investment portfolio’s performance and asset allocation. According to a 2025 Vanguard study, an investor with a portfolio diversified across U.S. and non-U.S. stocks in a 60%/40% ratio would have had returns close to 10% annualized over time.

The Road Ahead

A thorough assessment of these four areas will provide you with a comprehensive understanding of your financial starting point. This knowledge is essential for setting realistic goals and developing effective strategies to achieve them. As you move forward, you’ll find that this solid foundation will guide you in making informed decisions about your financial future. The next step in your financial planning journey involves setting clear, actionable goals that align with your current financial situation and future aspirations.

What Are Your Financial Goals?

Defining Your Financial Objectives

Start by identifying what you want to achieve financially in the short-term (1-3 years) and long-term (4+ years). Short-term goals might include paying off credit card debt, saving for a down payment on a house, or building an emergency fund. Long-term goals often revolve around retirement savings, funding your children’s education, or starting a business.

Be specific about your goals. Instead of saying “I want to save more,” set a target like “I want to save $20,000 for a down payment on a house within two years.” This level of specificity makes your goals more tangible and easier to work towards.

Prioritizing Your Financial Goals

Once you’ve identified your goals, it’s time to prioritize them. Consider both the importance and urgency of each goal. For example, building an emergency fund might take precedence over saving for a vacation. Similarly, if you’re in your 50s, boosting your retirement savings might be more critical than funding your child’s college education.

A useful approach is to rank your goals from most to least important. This ranking helps you allocate your resources effectively and ensures you’re making progress on your most important objectives.

Creating a Timeline for Your Goals

Assign a target date to each of your goals. This timeline creates a sense of urgency and helps you track your progress. For instance, if you aim to save $60,000 for a down payment in five years, you know you need to save $1,000 per month to reach that goal.

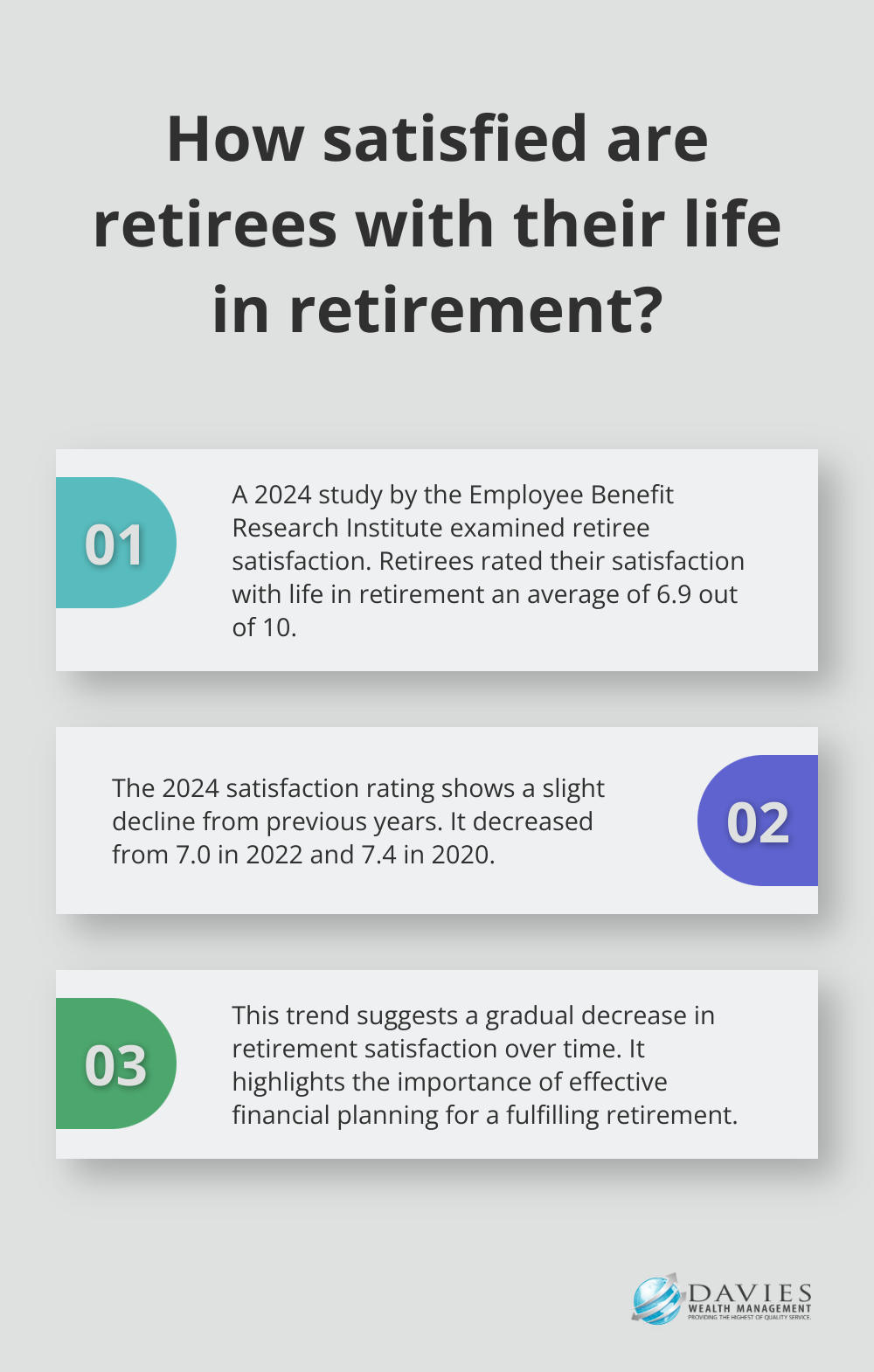

Be realistic with your timelines. A 2024 study by the Employee Benefit Research Institute found that retirees rated their satisfaction with life in retirement an average of 6.9, down slightly from 7.0 in 2022 and 7.4 in 2020. Setting overly ambitious timelines can lead to frustration and abandonment of your goals.

Making Your Goals SMART

To increase your chances of success, ensure your goals are SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. Let’s break this down:

- Specific: Clearly define what you want to achieve.

- Measurable: Attach a number to your goal so you can track progress.

- Achievable: Ensure your goal is realistic given your current financial situation.

- Relevant: Your goal should align with your overall financial plan and life objectives.

- Time-bound: Set a deadline for achieving your goal.

For example, a SMART goal might be: “I will save $24,000 for an emergency fund by setting aside $1,000 per month for the next two years.”

Regular Review and Adjustment

Goal-setting is not a one-time event. You should regularly review and adjust your goals as your life circumstances change. This flexibility allows you to stay on track with your financial objectives while adapting to new opportunities or challenges.

As you move forward in your financial planning journey, the next step involves developing and implementing strategies to achieve your newly defined goals. This process will require careful consideration of various financial tools and techniques (such as budgeting, investment strategies, and risk management) to create a comprehensive plan tailored to your unique situation.

Turning Your Financial Plan into Action

Build a Robust Budget

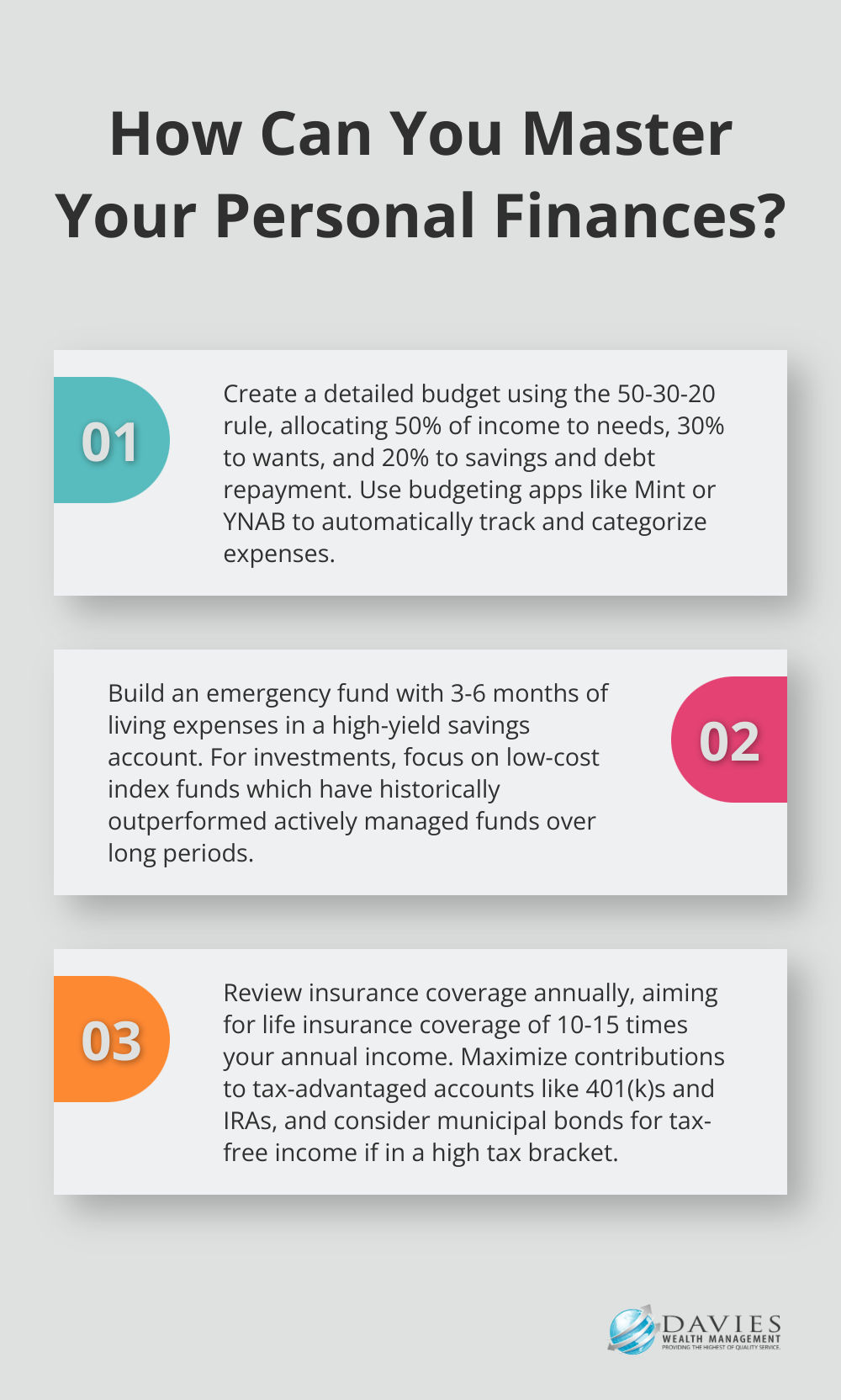

The foundation of any successful financial plan is a well-structured budget. Start by categorizing your expenses into fixed (rent, utilities) and variable (entertainment, dining out) costs. Try to allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. This 50-30-20 rule provides a solid framework for financial stability.

Use budgeting apps like Mint or YNAB to track your spending automatically. These tools can categorize your expenses and alert you when you approach your spending limits. A budget isn’t about restriction; it’s about making conscious choices that align with your financial goals.

Fortify Your Financial Foundation

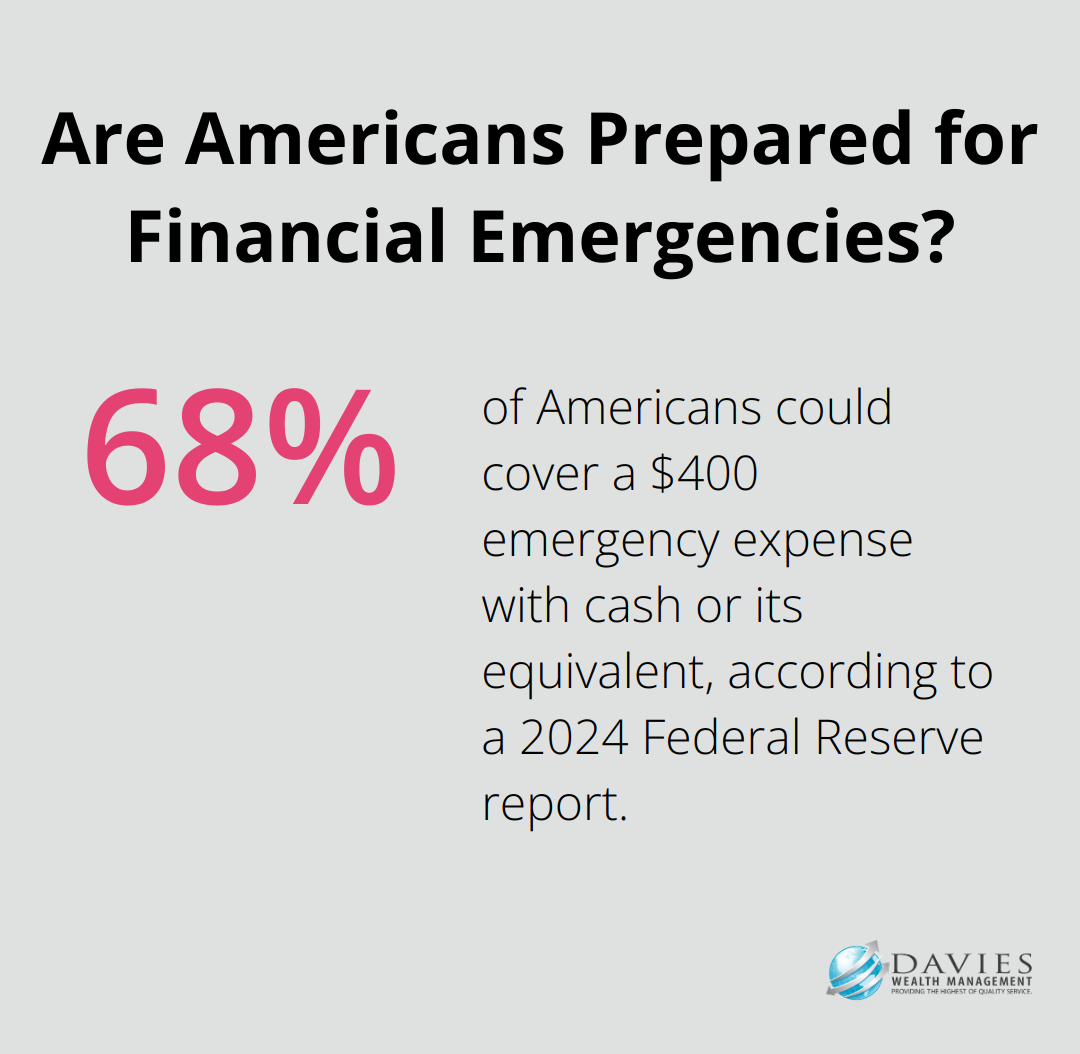

An emergency fund acts as your financial safety net. Try to save 3-6 months of living expenses in a high-yield savings account. A 2024 Federal Reserve report revealed that only 68% of Americans could cover a $400 emergency expense with cash or its equivalent. Don’t become part of the 32% caught off guard.

For investment strategy optimization, consider low-cost index funds. They offer broad market exposure and have consistently outperformed actively managed funds over the long term. A study by S&P Dow Jones Indices found that over a 15-year period, 92.43% of large-cap funds underperformed the S&P 500.

Protect Your Financial Future

Insurance is a key component of your financial plan. Review your coverage annually to ensure it keeps pace with your life changes. For life insurance, a general rule of thumb is to have coverage 10-15 times your annual income (however, your specific needs may vary based on factors like dependents and outstanding debts).

Tax efficiency can significantly impact your wealth accumulation. Maximize contributions to tax-advantaged accounts like 401(k)s and IRAs. If you’re in a high tax bracket, consider municipal bonds for tax-free income.

Plan Your Estate

Estate planning isn’t just for the wealthy. It ensures your assets are distributed according to your wishes and can minimize the tax burden on your heirs. Start with a basic will and healthcare directive. As your wealth grows, consider more advanced tools like trusts.

Seek Professional Guidance

Creating and implementing a comprehensive financial plan can be complex. Professional financial advisors can provide valuable expertise and guidance. They can help you navigate complex financial decisions, from optimizing your investment strategy to planning for tax efficiency. If you’re a professional athlete facing unique financial challenges, specialized advisors can offer tailored strategies to protect and grow your wealth beyond your playing years.

Final Thoughts

A comprehensive financial planning checklist empowers you to take control of your financial future. This systematic approach allows you to assess your current situation, set clear goals, and implement strategic actions for long-term financial success. Financial planning requires regular review and adjustment as your life circumstances evolve.

The financial world’s complexity often necessitates expertise beyond most individuals’ capabilities. A professional financial advisor can make a significant difference in navigating these challenges effectively. At Davies Wealth Management, we offer tailored financial solutions that address your unique needs and goals.

Our team of experts can help you create and implement a robust financial planning checklist to ensure you achieve your financial objectives. We provide clarity, reduce stress, and maximize your potential for financial success (whether you’re a professional athlete facing unique challenges or an individual seeking to secure your financial future).

Leave a Reply