At Davies Wealth Management, we understand that optimizing your investing tax strategies can significantly impact your overall financial success.

Smart tax planning can help you keep more of your investment returns and build wealth more efficiently.

In this post, we’ll explore key techniques to minimize your tax burden while maximizing your investment potential.

Tax-Efficient Investing Strategies

At Davies Wealth Management, we prioritize tax-efficient investing strategies to maximize your wealth over time. These techniques can help you retain more of your investment returns and accelerate your progress towards financial goals.

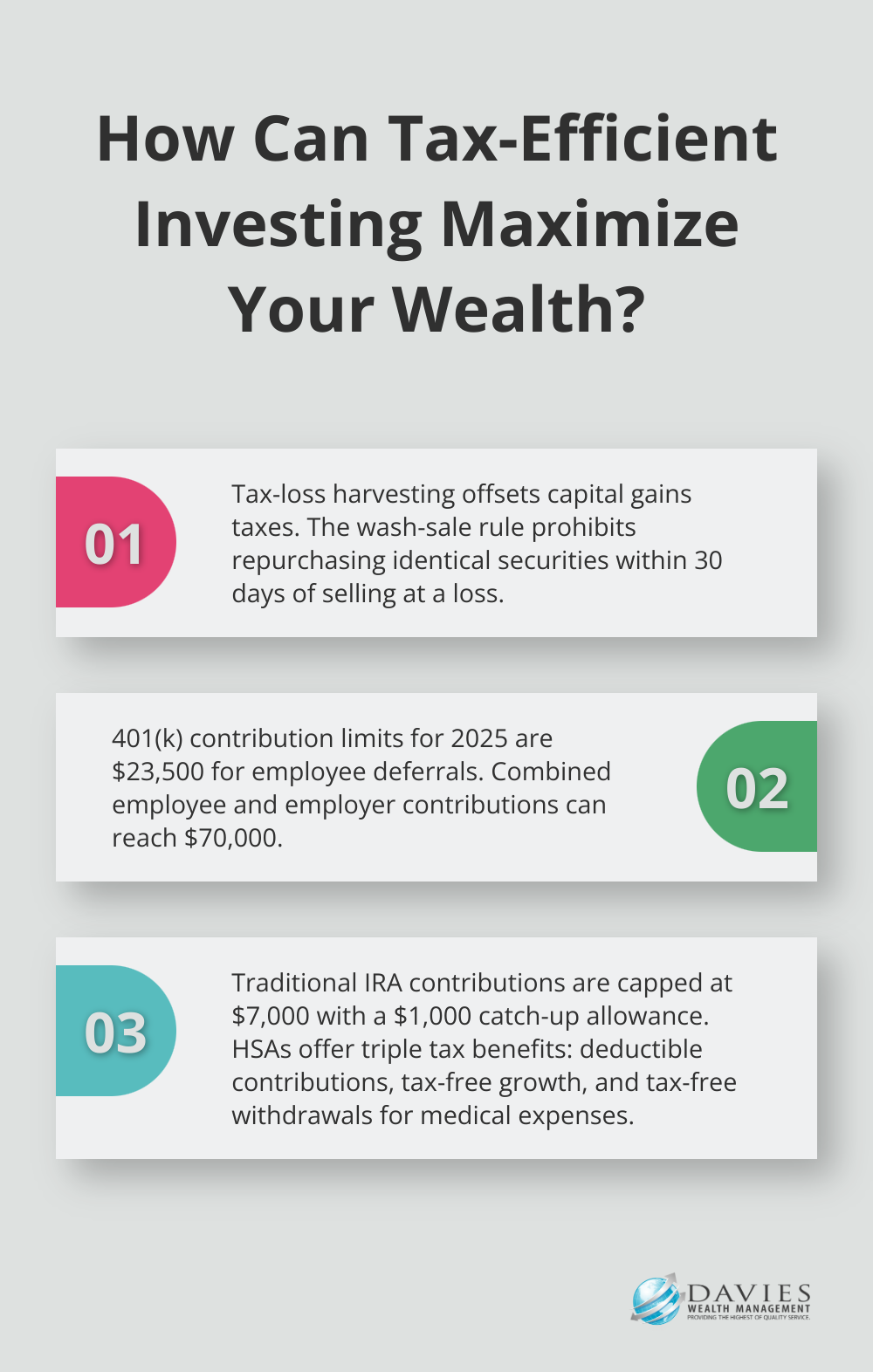

Tax-Loss Harvesting

Tax-loss harvesting involves selling investments that have declined in value to offset capital gains taxes on profitable investments. This strategy can reduce your overall tax liability while maintaining your portfolio’s asset allocation. Be aware of the wash-sale rule, which prohibits repurchasing the same or substantially identical securities within 30 days of selling them at a loss.

Maximizing Tax-Advantaged Accounts

Fully utilizing tax-advantaged accounts minimizes your tax burden effectively. For 2026, you can contribute up to $24,500 to a 401(k) plan through employee salary deferrals. The combined employee and employer contributions can reach up to $72,000. Traditional IRA contributions are limited to $7,500 (with a $1,100 catch-up allowance). Health Savings Accounts (HSAs) offer triple tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Tax-Efficient Investment Vehicles

Incorporating tax-efficient investment vehicles into your portfolio can significantly reduce your tax liability. Bonds provide income that’s generally exempt from federal taxes, making them an attractive investment option for individuals in high tax brackets. Index funds and ETFs typically have lower turnover rates compared to actively managed funds, resulting in fewer capital gains distributions and lower tax bills.

Customized Tax Strategies for Athletes

Professional athletes face unique tax challenges due to varying income streams and multi-state tax obligations. Davies Wealth Management specializes in creating personalized investment strategies tailored to these complex financial situations. We optimize your investment approach to ensure you’re not just growing your wealth, but retaining as much of it as possible in the face of tax liabilities.

As we move forward, it’s important to consider how the timing of your investments can further enhance your tax benefits. Let’s explore strategies to capitalize on long-term vs. short-term capital gains and other timing considerations.

When to Time Your Investments for Tax Benefits

Long-Term vs. Short-Term Capital Gains

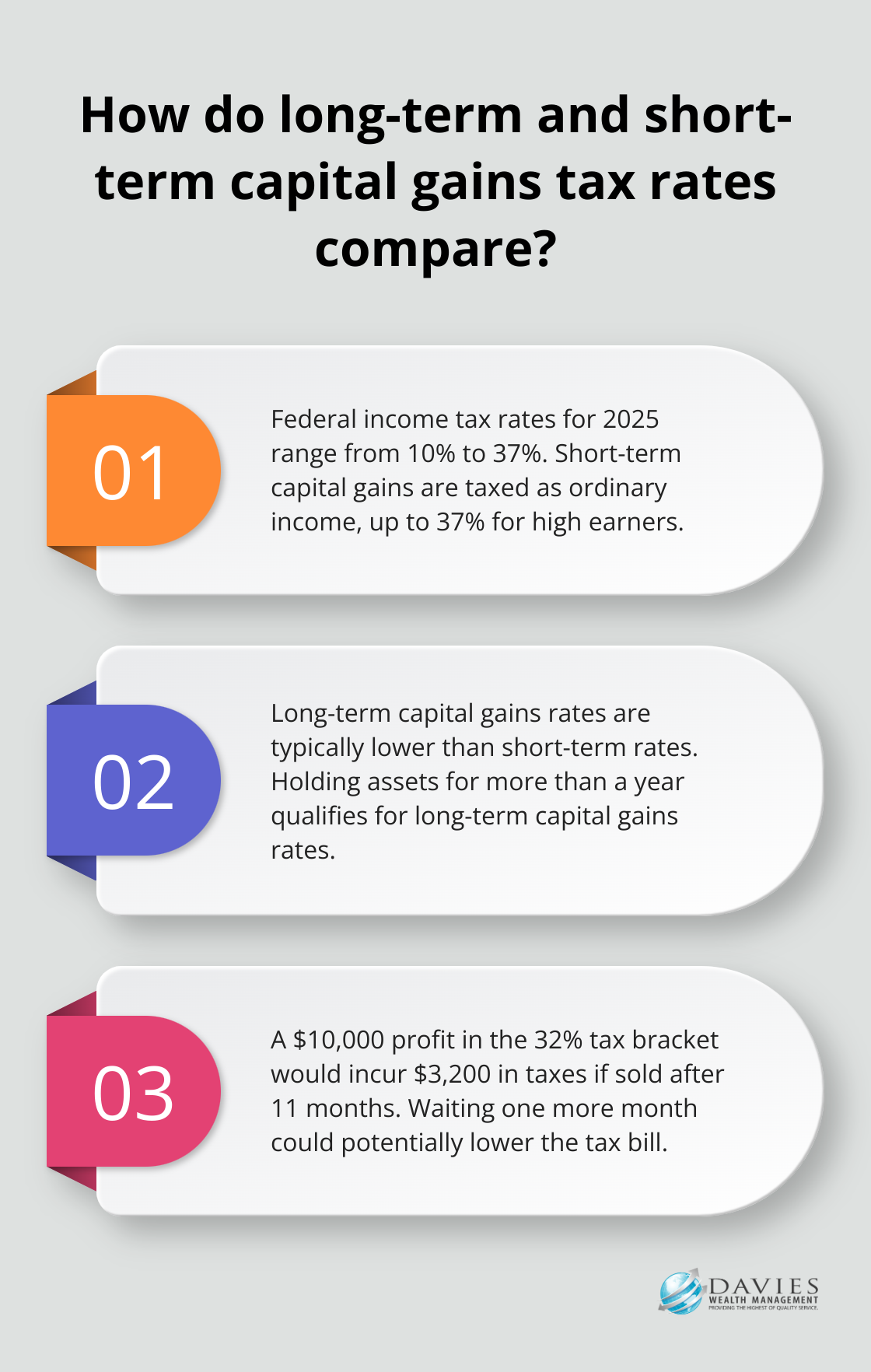

The holding period of your investments directly affects your tax rate. Assets held for more than a year qualify for long-term capital gains rates, which are typically lower than short-term rates. For 2025, federal income tax rates are 10%, 12%, 22%, 24%, 32%, 35%, and 37%. In contrast, short-term gains are taxed as ordinary income, which can reach up to 37% for high earners.

Consider this example: If you’re in the 32% tax bracket and sell a stock for a $10,000 profit after holding it for 11 months, you’ll owe $3,200 in taxes. However, if you wait just one more month to sell, your tax bill could be lower, depending on your specific tax situation. This difference underscores the importance of considering holding periods in your investment decisions.

Strategic Selling for Tax Efficiency

When it’s time to sell investments, consider which specific shares to sell to minimize your tax burden. The specific identification method allows you to choose which shares of a security to sell, rather than using the default first-in-first-out (FIFO) method.

For instance, if you bought shares of a company at different times and prices, you might choose to sell the highest-cost shares first to minimize your capital gain. This strategy can prove particularly effective when you rebalance your portfolio or raise cash for other investments.

Year-End Tax Planning

As the year draws to a close, review your investment portfolio for tax-saving opportunities. If you have unrealized losses, consider selling these investments to offset gains realized earlier in the year. This strategy, known as tax-loss harvesting, can lower your tax bill and better position your portfolio going forward.

Additionally, if you’re charitably inclined, consider donating appreciated securities instead of cash. You’ll avoid paying capital gains tax on the appreciation and may be able to deduct the full fair market value of the donation.

Roth IRA Conversion Strategies

Converting to a Roth IRA can serve as a powerful long-term tax strategy, especially in years when your income is lower than usual. While you’ll pay taxes on the converted amount in the year of conversion, future withdrawals from the Roth IRA will be tax-free, potentially allowing you to better manage your tax brackets in retirement.

For professional athletes (who often have fluctuating incomes), timing Roth conversions during lower-income years can prove particularly advantageous. Financial advisors can help identify these opportunities and execute conversions strategically to minimize lifetime tax burden.

As we explore these timing strategies, it becomes clear that optimizing your tax situation requires a multifaceted approach. Let’s now turn our attention to some advanced tax optimization techniques that can further enhance your overall financial picture.

Advanced Tax Strategies for Savvy Investors

At Davies Wealth Management, we’ve observed how advanced tax optimization techniques can significantly boost our clients’ wealth accumulation. These strategies extend beyond basic tax-efficient investing and can lead to substantial long-term savings.

Charitable Giving for Tax Benefits

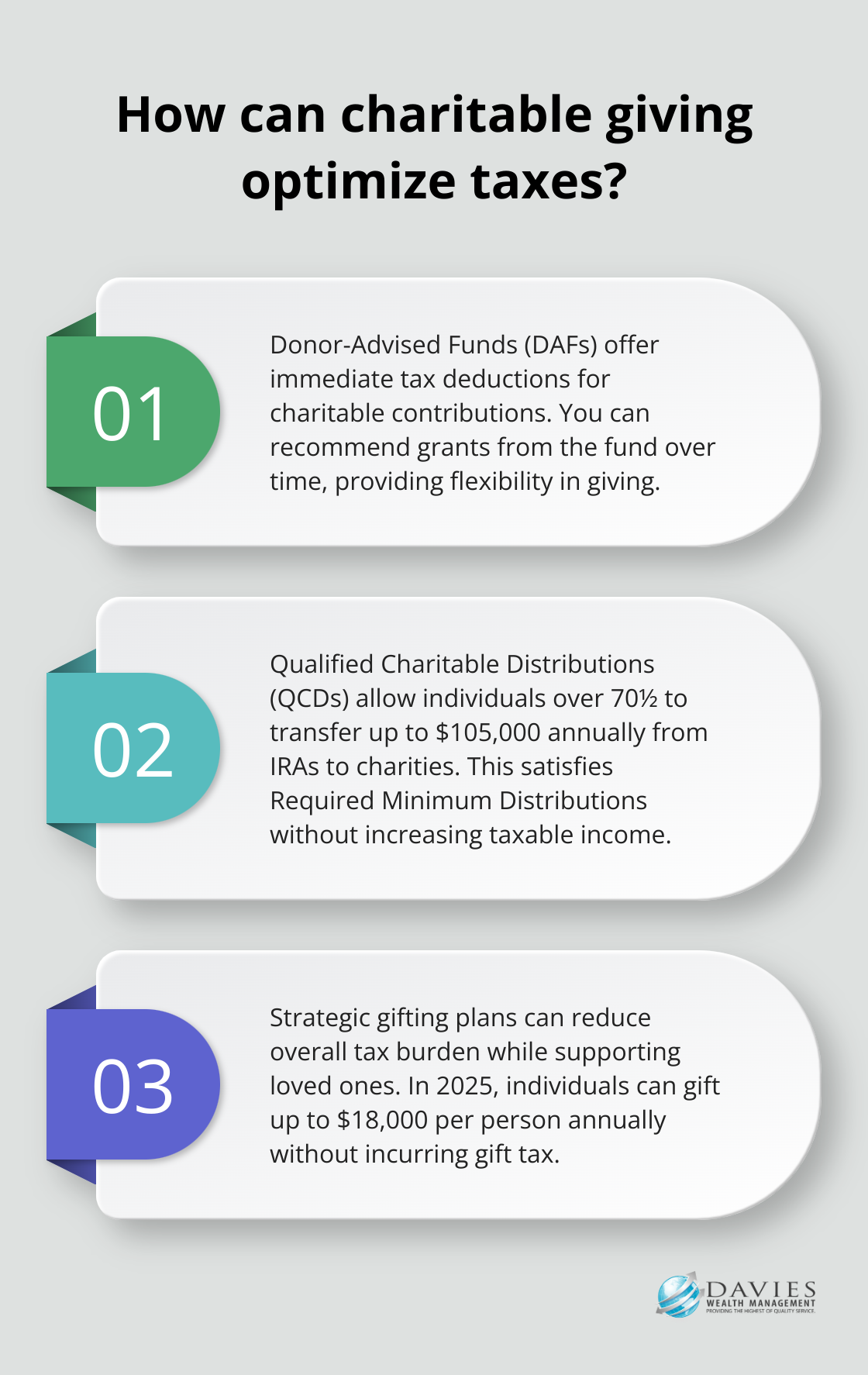

Charitable giving supports causes you care about and serves as a powerful tax optimization tool. Donor-Advised Funds (DAFs) allow you to take an immediate tax deduction when you make a charitable contribution, reducing your tax liability. You can then recommend grants from the fund over time, providing flexibility in your charitable giving while maximizing tax benefits.

For individuals over 70½, Qualified Charitable Distributions (QCDs) offer a unique advantage. You can transfer up to $105,000 annually from your IRA directly to qualified charities, satisfying your Required Minimum Distribution (RMD) without increasing your taxable income. This strategy effectively reduces your overall tax burden in retirement.

Strategic Estate Planning and Gifting

Estate planning benefits more than just the ultra-wealthy. A strategic gifting plan reduces your overall tax burden while supporting your loved ones. In 2025, you can gift up to $18,000 per person annually without incurring gift tax (this amount doubles to $36,000 per recipient for married couples).

Trusts help transfer wealth to future generations more tax-efficiently. Irrevocable Life Insurance Trusts (ILITs), for instance, remove life insurance proceeds from your taxable estate, potentially saving your heirs significant estate taxes.

Asset Location Optimization

Asset location plays a critical role in tax-efficient investing. Strategic placement of investments in the right types of accounts minimizes your tax liability without altering your overall asset allocation.

Tax-inefficient investments (such as high-yield bonds or REITs) should reside in tax-advantaged accounts like IRAs or 401(k)s. Tax-efficient investments (e.g., low-turnover index funds or municipal bonds) fit better in taxable accounts.

For example, if you invest in both stocks and bonds, consider holding your bonds in a tax-advantaged account where the interest income avoids annual taxation. Your stocks, which benefit from preferential long-term capital gains rates, can then occupy a taxable account.

Tax-Efficient Withdrawal Strategies

Developing a tax-efficient withdrawal strategy proves essential in retirement. The order in which you withdraw from different account types (taxable, tax-deferred, and tax-free) can significantly impact your overall tax burden.

A common approach involves withdrawing from taxable accounts first, followed by tax-deferred accounts, and finally tax-free accounts. This strategy allows tax-advantaged accounts to continue growing tax-free for longer periods.

Roth Conversion Ladders

Roth conversion ladders can help you move money gradually from a traditional IRA to a Roth IRA and save tax money. This strategy involves converting portions of a traditional IRA to a Roth IRA over several years, paying taxes on the converted amount each year. After five years, you can withdraw the converted amounts penalty-free, even if you’re under 59½.

Final Thoughts

Optimizing investing tax strategies enhances wealth-building potential. Tax-loss harvesting, maximizing tax-advantaged accounts, and using tax-efficient investment vehicles reduce tax burdens while growing portfolios. Timing investments wisely and considering long-term versus short-term capital gains amplify tax savings.

Advanced strategies offer additional avenues for tax efficiency. These approaches, combined with tax-efficient withdrawal strategies in retirement, lead to substantial long-term benefits. However, effective tax planning is not a one-size-fits-all endeavor (your unique financial situation should guide your approach).

Professional guidance often proves wise given the intricacies of tax laws. At Davies Wealth Management, we create personalized financial strategies aligned with specific needs and goals. Our expertise in investing tax strategies helps navigate complexities, ensuring informed decisions that support long-term financial success.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

Leave a Reply