At Davies Wealth Management, we understand the importance of making your money work for you in the short term.

Navigating the world of best short-term investment strategies can be challenging, but it’s essential for achieving your financial goals.

In this post, we’ll explore various options that can help you maximize returns while maintaining flexibility and minimizing risk management strategies.

Where to Park Your Short-Term Cash

At Davies Wealth Management, we recommend high-yield savings accounts (HYSAs) and money market funds as excellent options for short-term investing. These vehicles offer a balance of safety, liquidity, and competitive returns, making them ideal for parking cash you might need in the near future.

High-Yield Savings Accounts: Your First Stop

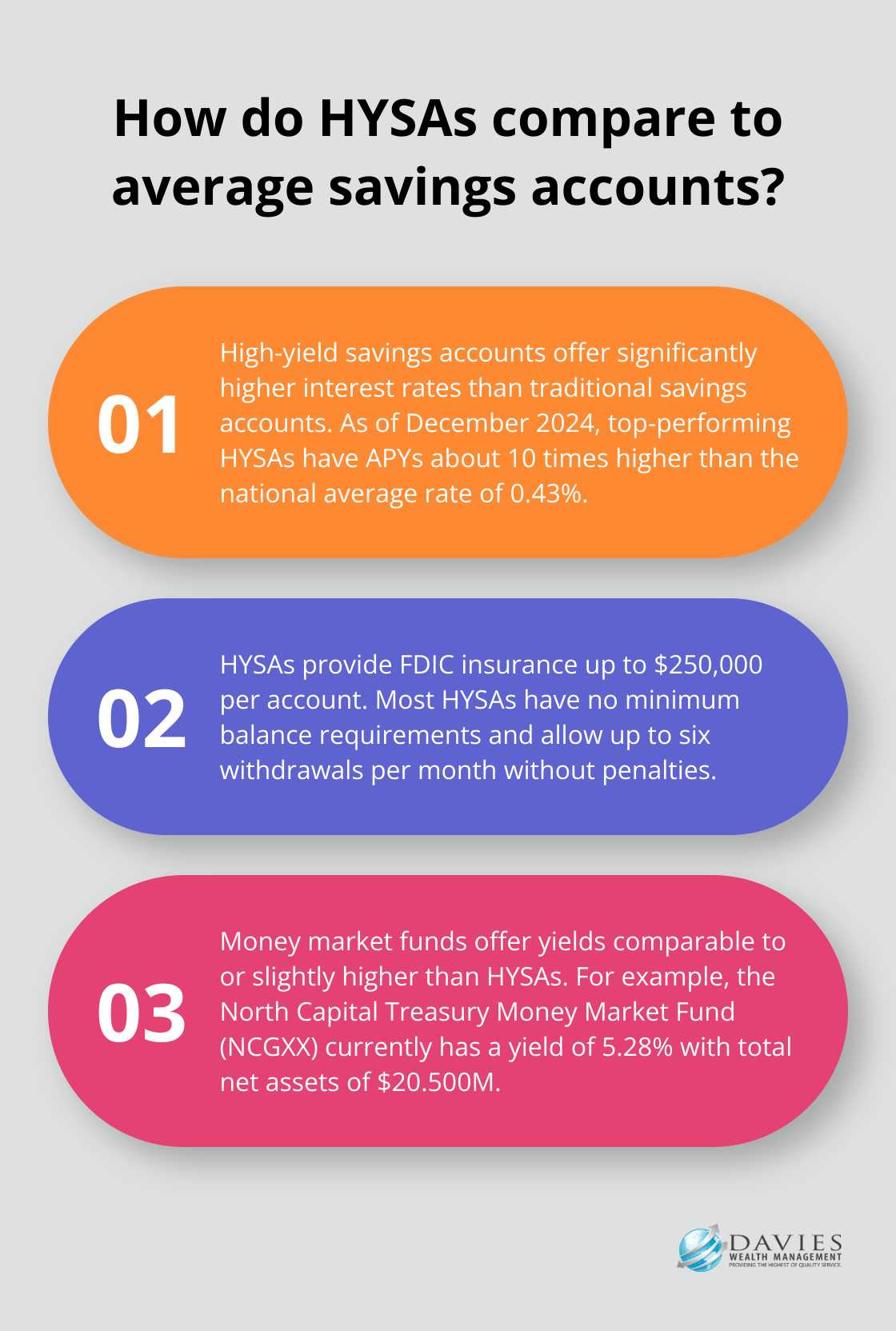

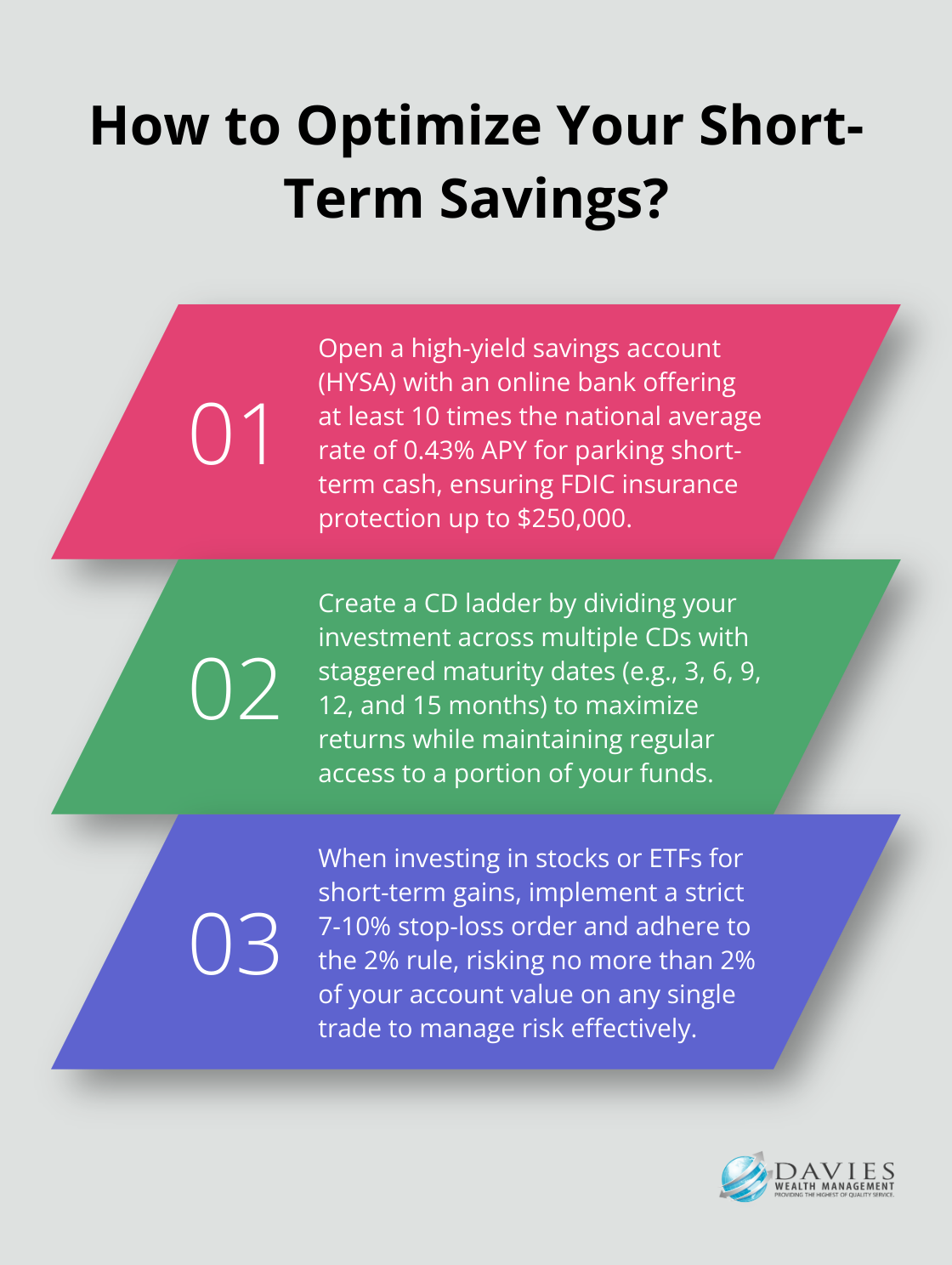

High-yield savings accounts are a step up from traditional savings accounts, offering significantly higher interest rates. As of December 2024, top-performing HYSAs have annual percentage yields (APYs) that are often about ten times higher than the national average savings rate (rates change frequently — compare current APYs before opening an account).

HYSAs provide several advantages:

- FDIC insurance protects deposits up to $250,000 per account

- Most have no minimum balance requirements

- They offer easy access to funds (typically allowing up to six withdrawals per month without penalties)

Money Market Funds: A Step Beyond

For those who seek potentially higher returns and don’t mind a slightly increased risk, money market funds are worth considering. These mutual funds invest in short-term, high-quality debt instruments (such as Treasury bills and commercial paper).

Money market funds typically offer yields comparable to or slightly higher than HYSAs. Yields track the federal funds rate and change over time, so compare current 7-day SEC yields (published by every fund) before choosing where to park cash.

While not FDIC-insured, money market funds are generally considered low-risk investments. They aim to maintain a stable net asset value (NAV) of $1 per share, although this is not guaranteed. In extreme financial situations, there’s a small risk of “breaking the buck,” where the NAV falls below $1.

Comparing Interest Rates and Accessibility

When choosing between HYSAs and money market funds, consider both interest rates and accessibility. HYSAs typically offer immediate access to your funds, while money market funds may require a day or two for transactions to settle.

Interest rates can fluctuate, so it’s wise to shop around and compare offers from different institutions. Online banks often provide the most competitive rates for HYSAs due to their lower overhead costs.

For money market funds, pay attention to expense ratios, as these can eat into your returns. Try to find funds with low expense ratios, ideally below 0.25%.

Tailoring Your Short-Term Investment Strategy

Your choice between HYSAs and money market funds should align with your specific financial situation and goals. Consider factors such as:

- The amount you plan to invest

- How quickly you might need access to the funds

- Your portfolio risk tolerance

- Current market conditions and interest rate trends

As we move forward to explore other short-term investment options, keep in mind that diversification across different vehicles can help mitigate risks associated with interest rate fluctuations and market volatility.

CDs and Bond Ladders: Strategies for Short-Term Gains

The Power of CDs for Short-Term Goals

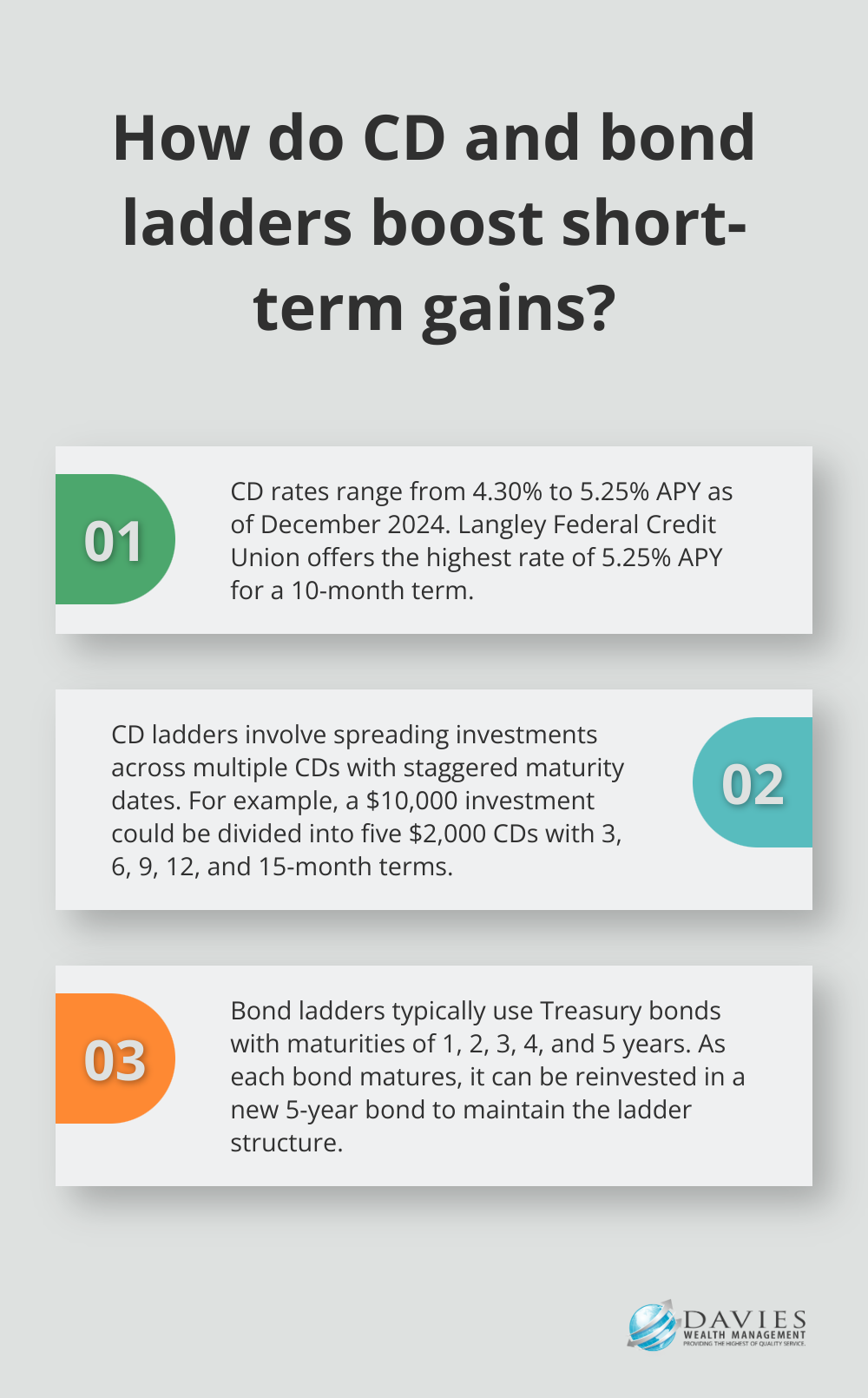

Certificates of Deposit (CDs) offer an effective tool for short-term investing. Banks and credit unions provide these time deposits, which typically yield higher interest rates than savings accounts. In exchange, you agree to leave your money untouched for a set period. As of December 2024, top banks offer CD rates ranging from 4.30 percent APY to 5.25 percent APY, with the highest rate offered by Langley Federal Credit Union for a 10-month term.

CDs provide a guaranteed return, which makes them suitable for short-term goals with specific timelines. Once you lock in a rate, you secure that return regardless of market fluctuations. This feature proves particularly useful when saving for a down payment on a house or a major purchase within the next 1-3 years.

However, early withdrawal penalties can pose a risk. Breaking a CD before maturity may cost you a portion of the interest earned or even some principal. To mitigate this risk, consider a CD ladder strategy.

Building a CD Ladder for Flexibility

A CD ladder involves spreading your investment across multiple CDs with staggered maturity dates. For example, you might divide $10,000 into five $2,000 CDs with 3-month, 6-month, 9-month, 12-month, and 15-month terms.

This approach offers several benefits:

- Regular access to a portion of your funds

- Ability to reinvest at potentially higher rates as CDs mature

- Higher average yield compared to keeping all funds in a single short-term CD

Exploring Bond Ladders for Steady Income

Bond ladders operate on a similar principle but use individual bonds instead of CDs. This strategy works particularly well with Treasury bonds (backed by the full faith and credit of the U.S. government).

A typical bond ladder might involve purchasing bonds that mature in 1, 2, 3, 4, and 5 years. As each bond matures, you can reinvest in a new 5-year bond, maintaining the ladder structure.

Bond ladders can help reduce portfolio risk and provide a steady income. They offer the potential for higher yields compared to CDs, especially in a rising interest rate environment. However, bond prices can fluctuate based on market conditions, introducing some level of risk.

Balancing Risk and Return

When constructing CD or bond ladders, consider your risk tolerance and liquidity needs. Shorter-term investments generally offer lower yields but provide more frequent opportunities to reinvest at potentially higher rates.

A mix of short and medium-term investments in a ladder strategy helps balance the need for current income with the potential for higher returns in the future. For example, a conservative ladder might focus on 3-month to 2-year maturities, while a more aggressive strategy could extend out to 5 years or beyond.

Consider inflation when planning your ladder strategy. While CDs and bonds offer guaranteed returns, those returns may not keep pace with inflation over longer periods. This reality underscores the importance of diversifying your investment portfolio.

As we move forward to explore short-term stock investments and ETFs, keep in mind that these strategies can complement your CD and bond ladders, providing potential for growth alongside the stability of fixed-income investments.

Are Stocks Short-Term Investments?

Generally, no — stocks are not short-term investments. While equities have historically produced strong returns over long horizons, over windows of one to three years the range of outcomes is wide and includes meaningful losses; historical performance does not guarantee future results. Money you expect to need within about three years is usually better held in high-yield savings accounts, money market funds, CDs, or short-duration Treasuries, where the value of your principal is far more predictable.

That said, there are situations where limited short-term stock exposure can play a role: investors with a longer overall horizon who are deploying a tactical slice of their portfolio, or those using broad, liquid ETFs with defined risk controls rather than concentrated single-stock bets. The key distinction is between investing money you can leave alone through a downturn and parking money you will need soon — stocks suit the first job, not the second. The sections below cover how to approach short-term stock and ETF positions if they fit your plan, and how to size them responsibly.

Navigating Short-Term Stock and ETF Investments

Identifying Promising Short-Term Stock Opportunities

Short-term stock investments require a strategic approach to market trends and company performance. We recommend stocks with high liquidity and moderate volatility, which allow for easier entry and exit points. This characteristic proves essential for short-term trading success.

The momentum effect offers one effective strategy. Stocks that perform the best (worst) over a three- to 12-month period tend to continue to perform well (poorly). Investors can leverage this phenomenon for potential short-term gains.

Monitoring upcoming events that could impact stock prices provides another approach. Earnings reports, product launches, or industry conferences often create short-term price movements. For instance, Apple’s stock typically experiences increased volatility around its annual product launch events in September.

Leveraging ETFs for Diversified Short-Term Investing

Exchange-Traded Funds (ETFs) offer exposure to multiple stocks or sectors without the risk associated with individual stock picking. For short-term investing, sector-specific or thematic ETFs that align with current market trends often prove beneficial.

The SPDR S&P 500 ETF Trust (SPY) provides broad market exposure, tracking the S&P 500 index and offering instant diversification across 500 of the largest U.S. companies. Its returns vary widely from year to year — past performance does not guarantee future results. Investors interested in specific sectors might consider ETFs like the Technology Select Sector SPDR Fund (XLK) or the Health Care Select Sector SPDR Fund (XLV) for targeted exposure.

Leveraged ETFs can amplify returns for short-term traders (but come with increased risk). These funds aim to deliver multiples of their underlying index’s daily performance. The ProShares UltraPro QQQ (TQQQ), for example, seeks to provide three times the daily performance of the Nasdaq-100 Index.

Implementing Risk Management Strategies

Short-term stock and ETF investments carry more risk than other options. To mitigate this risk, we employ several strategies:

- Set strict stop-loss orders: These automatically sell a stock or ETF if it drops below a certain price, limiting potential losses. Try to set stop-losses at 7-10% below the purchase price for short-term trades.

- Use position sizing: Never invest more than you can afford to lose in a single trade. A general guideline suggests risking no more than 1-2% of your trading capital on any single position.

- Apply the 2% rule: This rule advises against risking more than 2% of your account on a single trade. For a $50,000 account, this means not risking more than $1,000 on any single trade.

- Diversify across sectors: Even within short-term investments, diversification remains key. Spread your investments across different sectors to reduce the impact of sector-specific downturns.

- Monitor market volatility: The VIX index (often called the fear index) measures expected market volatility. Investments in inverse VIX ETFs are generally seen as an opportunity for short-term gains, rather than for long-term buy-and-hold strategies.

Tailoring Strategies to Individual Needs

At Davies Wealth Management, we customize these strategies to each client’s risk tolerance and financial goals. Short-term stock and ETF investments can prove lucrative, but they require active management and a solid understanding of market dynamics. Our team guides you through this process, ensuring your short-term investment strategy aligns with your overall financial plan.

Final Thoughts

The best short-term investment strategies combine safety, liquidity, and potential returns. High-yield savings accounts, money market funds, CDs, bond ladders, and carefully selected stocks or ETFs can form a robust short-term investment portfolio. These strategies must align with your specific financial goals, risk tolerance, and investment timeline. Market conditions and interest rates change constantly, which necessitates regular reassessment of your investment choices.

Davies Wealth Management specializes in crafting personalized investment strategies for various financial situations. Our team of experts can help you navigate complex investment choices and make informed decisions about your short-term investments. We offer comprehensive wealth management solutions that extend beyond short-term investing to include retirement planning, tax strategies, and estate planning.

We invite you to seek professional advice to tailor your investment strategy to your unique needs. Davies Wealth Management can provide you with the expertise and guidance necessary to build a strong financial foundation. This foundation will support your short-term goals while setting the stage for long-term financial success.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

Leave a Reply