“`html

Retirement planning can be a daunting task, but with the right financial advice, it becomes manageable and even exciting. At Davies Wealth Management, we’ve seen firsthand how proper planning can transform retirement dreams into reality.

Our guide to financial advice for retirement planning covers essential strategies to secure your financial future. From leveraging compound interest to diversifying your portfolio and preparing for healthcare costs, we’ll explore key steps to help you build a robust retirement plan.

Why Start Early for Retirement?

Starting early for retirement can significantly impact your financial future. At Davies Wealth Management, we’ve observed how early planning transforms retirement dreams into reality.

The Power of Compound Interest

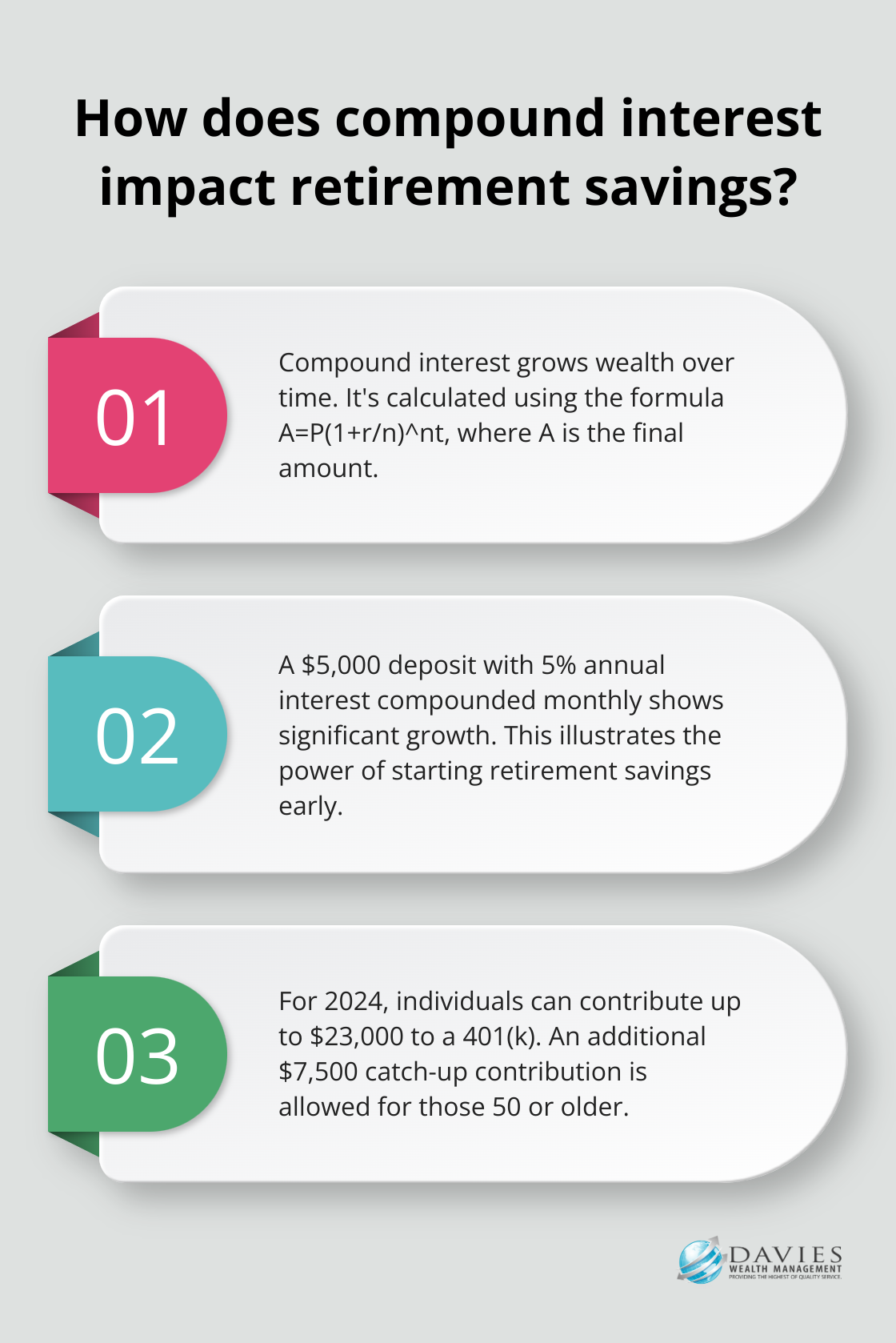

Compound interest acts as a powerful force in wealth building over time. It’s not just about the money you save, but also the interest you earn on that money, and then the interest on that interest. Over decades, this can lead to substantial growth in your retirement nest egg.

The power of compound interest can be calculated using the formula A=P(1+r/n)^nt. For example, if you deposit $5,000 in a savings account that earns a 5% annual interest rate and compounds monthly, you would see significant growth over time.

Maximizing Your Retirement Accounts

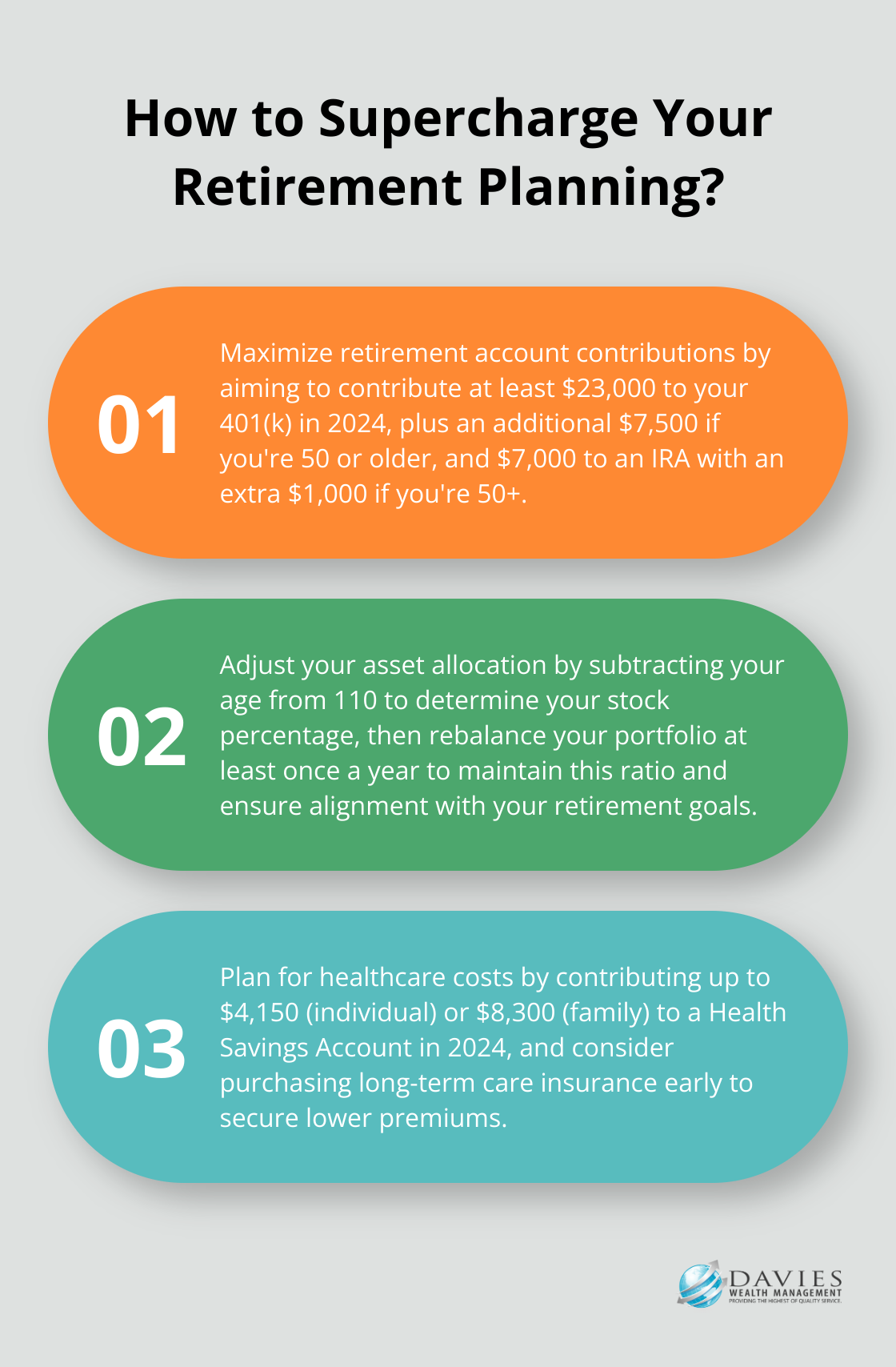

To harness the full potential of compound interest, you should maximize your contributions to retirement accounts. If your employer offers a 401(k) match, try to contribute at least enough to get the full match (it’s essentially free money). For 2024, you can contribute up to $23,000 to a 401(k), with an additional $7,500 catch-up contribution if you’re 50 or older.

Don’t overlook Individual Retirement Accounts (IRAs). For 2024, you can contribute up to $7,000 to an IRA, with an extra $1,000 catch-up contribution for those 50 and above. These limits are set by the IRS and can change annually, so stay informed.

Maximizing Your Retirement Accounts is crucial. For example, the catch-up contribution limit for employees 50 and over who participate in SIMPLE plans remains $3,500 for 2024.

The Impact of Small Increases

Even small increases in your savings rate can have a big impact over time. Try increasing your retirement contributions by 1% each year. You likely won’t notice the difference in your paycheck, but it can add up significantly over time.

For instance, if you’re 30 years old earning $60,000 a year and currently save 6% of your salary, increasing your savings rate by 1% each year until you reach 15% could result in an additional $355,000 in your retirement account by age 65 (assuming a 7% annual return).

Personalized Strategies for Early Retirement Planning

At Davies Wealth Management, we help our clients develop personalized strategies to maximize their retirement savings. We take into account their unique financial situations and goals. Starting early and leveraging the power of compound interest can set you up for a more secure and comfortable retirement. Compound interest, which is the interest earned on your initial savings and the reinvested earnings, is a great reason to start saving early.

As we move forward, it’s important to consider not just when to start saving, but also how to diversify your retirement portfolio for optimal growth and security.

How to Build a Diverse Retirement Portfolio

Balancing Risk and Reward

A successful retirement investment strategy requires the right balance between risk and reward. This balance shifts as you progress through different life stages. In your early career, you can take on more risk for potentially higher returns. As retirement approaches, you should shift towards more conservative investments to protect your wealth.

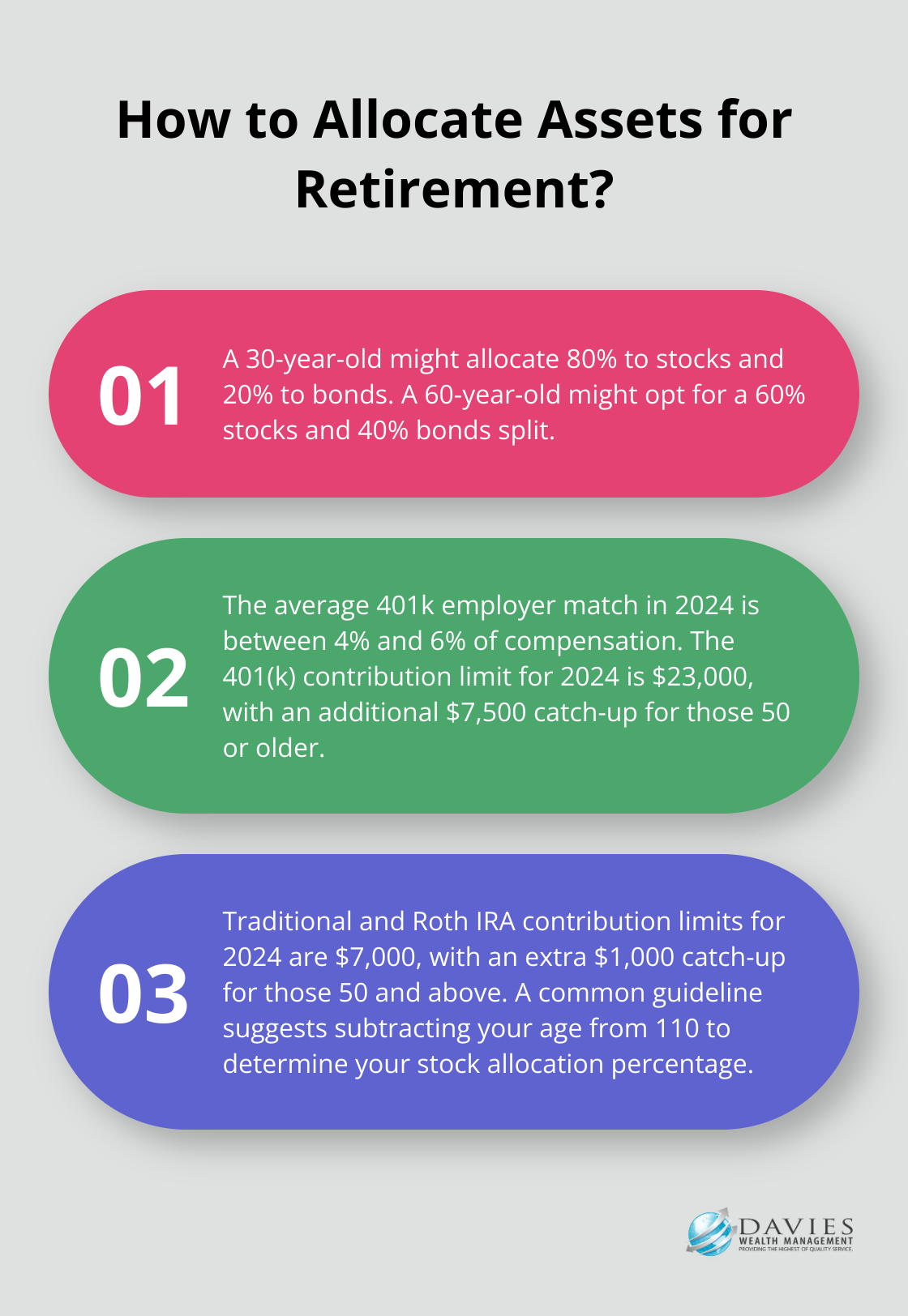

For instance, a 30-year-old might allocate 80% of their portfolio to stocks and 20% to bonds, while a 60-year-old might opt for a 60% stocks and 40% bonds split. These percentages should be tailored to your individual risk tolerance and financial goals.

Understanding Different Retirement Accounts

Several types of retirement accounts offer unique advantages:

401(k)s: Employer-sponsored plans often include matching contributions. The average 401k employer match in 2024 is between 4% and 6% of compensation. In 2024, you can contribute up to $23,000 to a 401(k), with an additional $7,500 catch-up contribution if you’re 50 or older.

Traditional IRAs: These accounts offer tax-deductible contributions and tax-deferred growth. For 2024, you can contribute up to $7,000, with an extra $1,000 catch-up contribution for those 50 and above.

Roth IRAs: These provide tax-free withdrawals in retirement. While contributions come from after-tax dollars, your earnings grow tax-free. The contribution limits match those of traditional IRAs.

Asset Allocation Strategies

Your asset allocation strategy should evolve throughout your life. In your 20s and 30s, you might focus on growth-oriented investments like stocks. As you enter your 40s and 50s, you should start to incorporate more fixed-income investments for stability.

A common guideline suggests subtracting your age from 110 to determine your stock allocation. For example, a 40-year-old might try for 70% stocks (110 – 40 = 70). However, this serves only as a starting point. Your actual allocation should reflect your individual circumstances and risk tolerance.

Regular portfolio rebalancing is essential. Market movements can disrupt your carefully planned asset allocation. You should review and rebalance at least once a year to ensure your portfolio aligns with your goals.

Expanding Your Investment Horizons

Diversification extends beyond stocks and bonds. You should consider including real estate investment trusts (REITs), commodities, or international stocks to further spread your risk. Recent diversification and performance benefits of non-US stocks have been muted, but that trend may not persist.

As you build your diverse retirement portfolio, it’s important to consider another critical aspect of retirement planning: healthcare costs. These expenses can significantly impact your financial security in retirement, and proper preparation is key to maintaining your lifestyle and peace of mind.

How Much Will Healthcare Cost in Retirement?

The Reality of Retirement Healthcare Costs

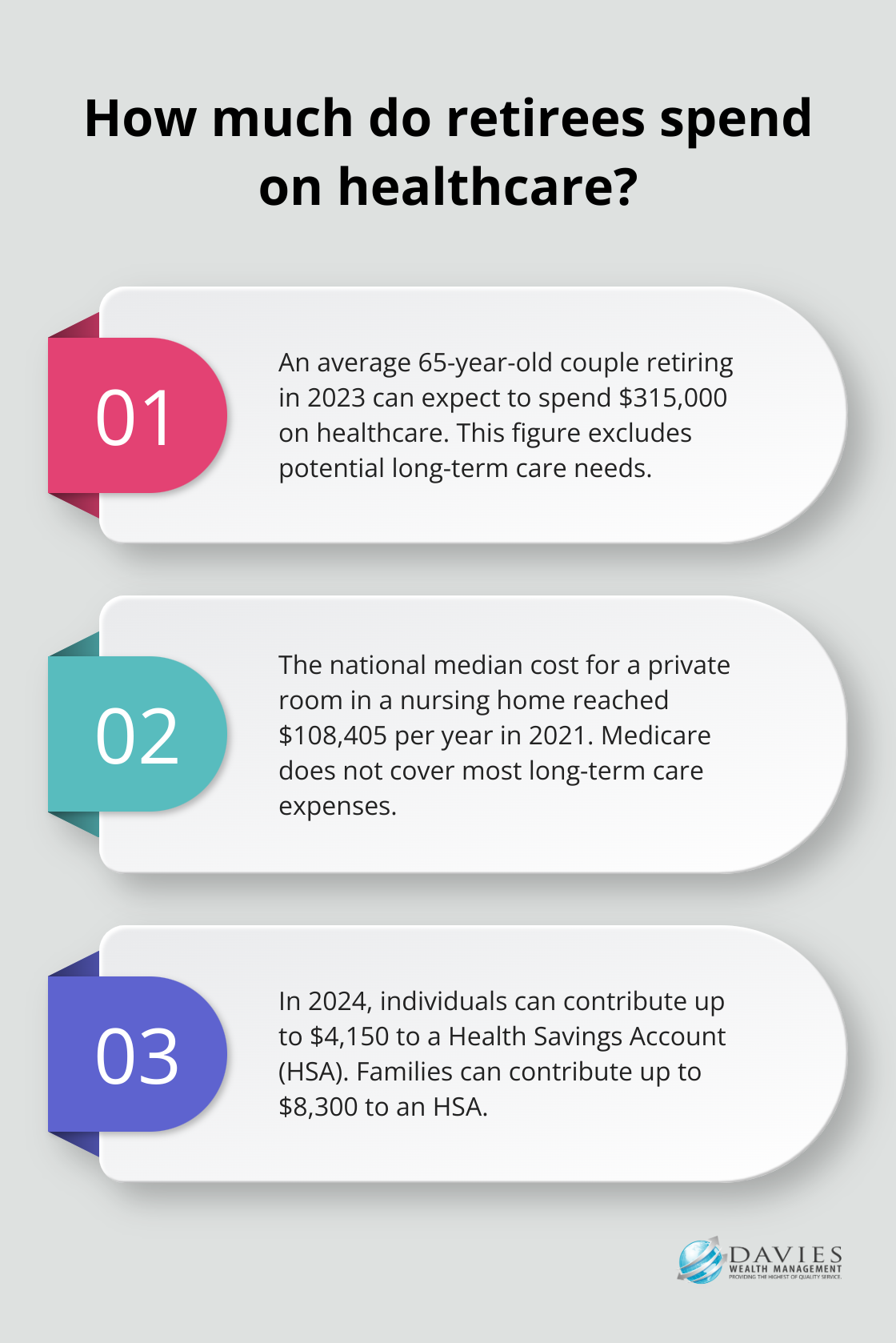

Healthcare costs represent a significant expense in retirement that many people underestimate. An average 65-year-old couple retiring in 2023 can expect to spend $315,000 on healthcare throughout their retirement. This figure excludes potential long-term care needs, which can add substantially to the total. For instance, the national median cost for a private room in a nursing home reached $108,405 per year in 2021 (as reported by Genworth’s Cost of Care Survey).

Understanding Medicare Coverage

Many retirees assume Medicare will cover all their healthcare needs, but this assumption is incorrect. While Medicare provides essential coverage, it has significant gaps. Medicare doesn’t cover most dental care, eye exams related to prescribing glasses, or hearing aids. Long-term care is another major expense not covered by Medicare, except in limited circumstances.

To address these gaps, many retirees opt for supplemental insurance. Medigap policies can help cover copayments, coinsurance, and deductibles. Medicare Advantage plans offer an alternative way to get Medicare benefits, often including prescription drug coverage and some services not covered by Original Medicare.

Strategies to Manage Healthcare Costs

One effective strategy to prepare for healthcare costs involves the use of a Health Savings Account (HSA) for eligible individuals. HSAs offer triple tax advantages: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. In 2024, individuals can contribute up to $4,150 to an HSA, while families can contribute up to $8,300.

Long-term care insurance is another important consideration. Depending on the policy, it may cover not just custodial care, but also home care, adult day health services, and other types of care. The earlier you purchase a policy, the lower your premiums will be. Some policies now offer hybrid options that combine life insurance with long-term care benefits, providing more flexibility.

Personalized Healthcare Planning

Healthcare costs can vary widely based on individual health status, location, and lifestyle choices. Regular health check-ups and maintaining a healthy lifestyle can potentially reduce your healthcare expenses in retirement. Professional financial advisors can help develop comprehensive strategies to address healthcare costs in retirement. These strategies might include a combination of dedicated healthcare savings, appropriate insurance coverage, and investment strategies designed to generate income for ongoing medical expenses.

Final Thoughts

Retirement planning requires careful consideration and strategic decision-making. The power of compound interest, portfolio diversification, and healthcare cost planning form the foundation of a robust retirement strategy. Financial advice for retirement planning should address these key aspects to help individuals build, protect, and enjoy their wealth in retirement.

Davies Wealth Management specializes in creating personalized retirement strategies tailored to specific goals, risk tolerance, and financial situations. We understand that every individual’s retirement journey is unique, including professional athletes with their distinct financial challenges. Our comprehensive approach to financial advice for retirement planning provides the tools and strategies needed for a secure future.

For personalized guidance on your retirement planning journey, visit Davies Wealth Management and take the first step towards a secure and fulfilling retirement. Our expertise can help you navigate the complexities of retirement planning and achieve your long-term financial goals. We stand ready to assist you at every stage of your financial journey.

“`

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

Leave a Reply