You've spent 15, maybe 25 years building something real in Stuart. Early mornings at the warehouse on Commerce Center Drive. Late nights balancing payroll and receivables. And now? Someone just wired eight figures into your account, and suddenly you're sitting in a quiet house wondering, "What the hell do I do with all this?"

Welcome to the other side of the liquidity event. The part nobody warns you about.

Here's the thing most Stuart business owners don't realize until it's too late: selling your company is the easy part. Managing the wealth afterward, without getting carved up by taxes, bad advisors, or your own decision fatigue, that's the real challenge. And unlike running your business, you don't get a second chance to get this right.

As a fee-only fiduciary advisor based right here on the Treasure Coast, I work exclusively with families navigating exactly this transition. No commissions. No product sales. Just straight advice held to the legal fiduciary standard, which means my only job is protecting your interests, not pushing whatever investment pays me the highest kickback.

Let's talk about what actually matters after you close the deal.

The 72-Hour Mistake Window (And How to Avoid It)

Most liquidity events follow a predictable pattern. You close on a Tuesday. By Friday, three "wealth managers" from the big wirehouses have already called. They smell the money before the wire even settles.

Here's their pitch: "Congratulations on your exit! Let's get you into our diversified portfolio right away. We'll take care of everything."

Translation: "Let me put your $12 million into our high-commission mutual funds and annuities before you realize there are better options."

The first rule of post-liquidity wealth management: slow down. You didn't build your business by making million-dollar decisions in 72 hours. Don't start now.

Take 90 days minimum before making any major financial moves. Yes, keep the cash liquid. Yes, it'll feel uncomfortable. But premature action costs more than temporary inefficiency.

The Fiduciary Framework: What You Actually Need

When Stuart business owners come to our office after a sale, they're usually thinking tactically: "Where should I invest?" "How do I avoid taxes?" "Can I retire yet?"

Those are fine questions. But they're Step 3 questions when you're still on Step 1.

Real business owner wealth management starts with a comprehensive framework that addresses six core areas:

1. Tax Mitigation Architecture

That $10 million sale? The IRS sees it as $2-4 million of their money, depending on how you structured the deal. Long-term capital gains help, but there are dozens of additional strategies most commission-based brokers never mention because they don't generate fees:

- Qualified Opportunity Zone deferrals (we've got several right here in Martin County)

- Charitable Remainder Trusts for high-basis portions

- Asset location strategies across taxable, tax-deferred, and tax-free accounts

- Entity structure optimization if you're taking earnout payments

2. Concentrated Position Unwinding

You just converted 100% business ownership into 100% cash. Congratulations: you've created a different concentration risk. The goal isn't to immediately deploy all capital into equities. It's to methodically build a diversified portfolio that doesn't require you to be right about any single position.

This is where separately managed accounts beat mutual funds for high-net-worth families. You need customization, tax-loss harvesting, and direct ownership: not cookie-cutter fund portfolios.

3. Estate Planning Reset

That old trust you set up in 2008 when the business was worth $2 million? It's not built for your new reality. Especially with the 2026 estate tax cliff approaching, you need modern strategies:

- Spousal Lifetime Access Trusts (SLATs) to use gift exemptions before they sunset

- Dynasty trusts for multi-generational wealth preservation

- Proper beneficiary designations across all accounts

- Coordination with any existing family limited partnerships

4. Income Engineering

Here's what's weird about selling a business: you go from predictable (if chaotic) cashflow to… nothing. No salary. No distributions. Just a pile of assets that need to generate a sustainable "paycheck."

This requires precision. Too conservative and inflation eats your purchasing power. Too aggressive and you're selling stocks in a downturn to pay your mortgage. We build withdrawal strategies based on your actual spending (not industry rules of thumb) and your psychological comfort with volatility.

5. Risk Transfer & Insurance Audit

Now that you're actually wealthy, you need different insurance. That $2 million umbrella policy? Laughably inadequate. Your homeowner's coverage on the Jupiter Island property? Probably hasn't kept pace with rebuilding costs.

Plus, you likely need to shift from term life insurance (protecting against lost business income) to permanent coverage (estate liquidity and legacy planning). Different problems require different tools.

6. Philanthropic Integration

Many Stuart business owners I work with have been quietly supporting local causes for years: the 1715 Fleet Society, youth sports programs, marine conservation efforts. Post-liquidity is when you can formalize that impact through donor-advised funds or private foundations while optimizing the tax benefits.

The Fiduciary vs. Broker Comparison You Need to See

Most business owners don't realize they're getting sold to, not advised. Here's the reality:

| Fee-Only Fiduciary | Commission-Based Broker |

|---|---|

| Legal obligation to act in your best interest | Suitability standard (product just needs to be "appropriate") |

| Transparent fee disclosure (typically 0.5-1% AUM) | Hidden commissions in products (often 3-6% upfront) |

| No product sales incentives | Paid more for proprietary funds and annuities |

| Comprehensive financial planning | Investment-focused, transactional relationship |

| Direct ownership via SMAs | Mutual fund wrappers with embedded costs |

If your "advisor" works for a brokerage and calls themselves a "wealth manager," they're almost certainly operating under the suitability standard. That means they can legally recommend high-commission products as long as they're not completely terrible for you. That's a low bar.

The Stuart Office Advantage: Local Expertise for Treasure Coast Families

Working with a fiduciary advisor based in Stuart: rather than some national firm calling from a tower in Manhattan: matters more than you think.

We understand the local ecosystem. We know the real estate dynamics in Palm Beach Gardens and Jupiter Island. We're familiar with the business environment along the Treasure Coast. We work with the same attorneys and CPAs you're probably already using.

When you sell your marine services company or medical practice or manufacturing operation, you need someone who understands what that business was worth in this market, not some generic valuation model from corporate headquarters.

Our strategic hub here in Stuart means we're accessible. Not just for quarterly reviews, but for those "I just got offered this deal, what do you think?" conversations that happen in real-time. Liquidity event financial planning isn't a set-it-and-forget-it proposition: it's an ongoing relationship.

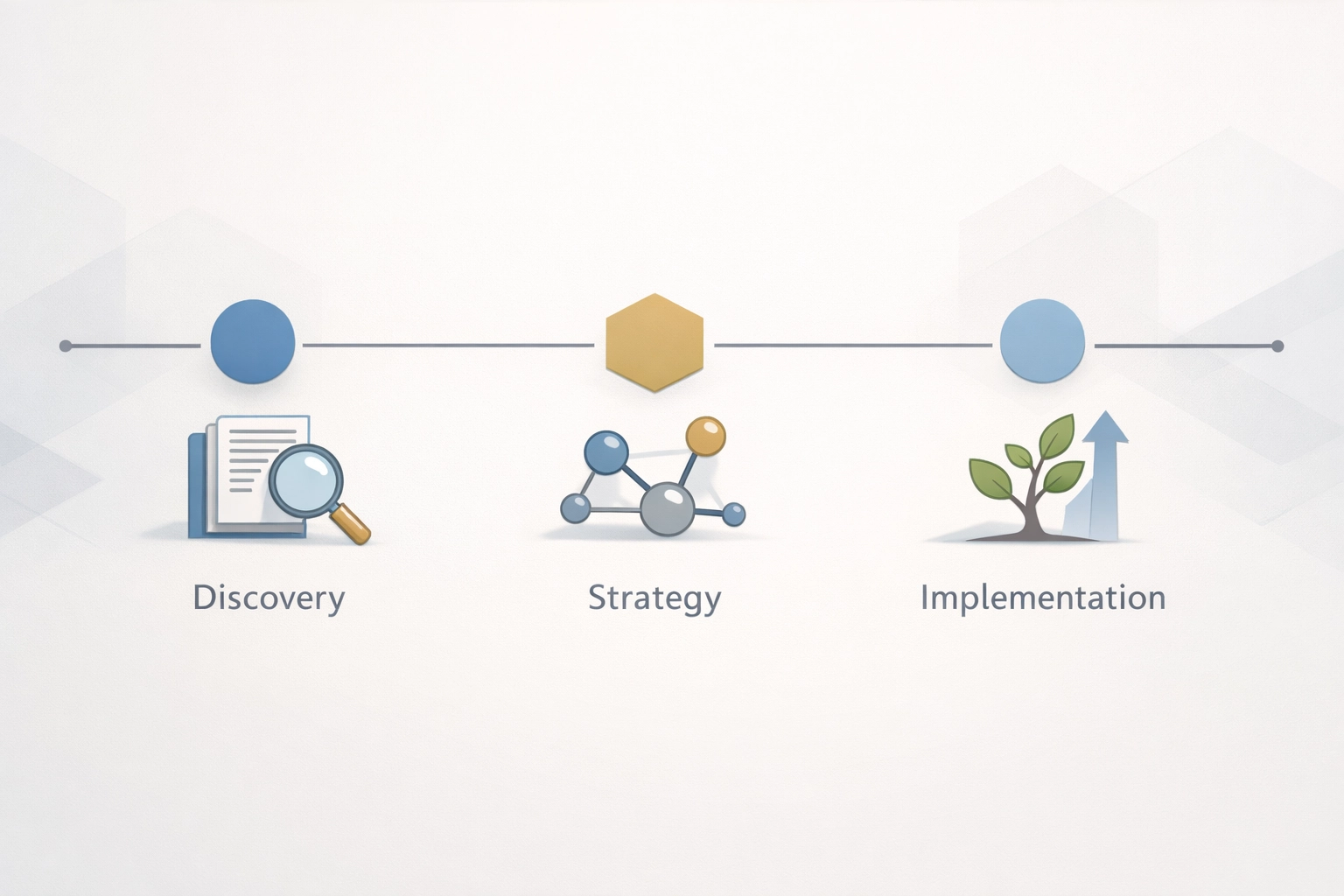

What the First 90 Days Should Actually Look Like

Here's the playbook we run with Stuart business owners post-sale:

Days 1-30: Discovery and documentation. We're gathering every financial document, understanding your goals, mapping your current tax situation, and stress-testing your spending assumptions. No portfolio moves yet.

Days 31-60: Strategy development. Tax planning with your CPA. Estate planning with your attorney. Insurance audit with specialists. Building your custom investment policy statement. Still no portfolio moves.

Days 61-90: Implementation begins. We're executing the tax strategies, opening accounts, transferring assets, and beginning the systematic deployment of capital according to the plan we've built together.

Most brokers want to start investing on Day 1. That's because they get paid when money moves, not when they think. A fiduciary approach is fundamentally different.

The Questions You Should Be Asking Any Advisor

Before you work with anyone after your liquidity event, ask these specific questions:

- "Are you a fiduciary 100% of the time?" (Anything other than an unqualified "yes" is a red flag)

- "How do you get paid?" (Fee-only is the only answer that eliminates conflicts)

- "What happens if I need $500K next month for a real estate opportunity?" (Tests their flexibility vs. lock-up products)

- "How do you coordinate with my CPA and attorney?" (Wealth management requires a team approach)

- "Show me your ADV Part 2." (This is the legal disclosure document all RIAs must provide: read it)

If they hesitate on any of these, walk away. You just sold your life's work. You can afford to be selective.

Moving Forward: Your Next Step

Selling your Stuart business puts you in rare company. Most entrepreneurs never make it to exit. You built something valuable enough that someone else wrote a check with lots of zeros.

But business owner wealth management post-liquidity requires a different skill set than business operations. You need someone who understands tax efficiency, estate planning, risk management, and investment strategy at a sophisticated level: and who's legally bound to put your interests first.

That's the fee-only fiduciary difference. And that's what we deliver for Treasure Coast families from our Stuart office.

If you're 90 days out from closing (or 90 days past it and realizing you need a different approach), let's talk. We work with business owners who've built something real and want to protect what they've created for generations.

Start by completing our questionnaire to see if your situation aligns with our planning approach. No sales pitch. Just a conversation about whether our fiduciary framework makes sense for your specific circumstances.

You spent decades building your business the right way. Your wealth deserves the same level of strategic attention.

DISCLAIMER

The content provided by Davies Wealth Management is intended solely for informational purposes and should not be considered as financial, tax, or legal advice. While we strive to offer accurate and timely information, we encourage you to consult with qualified retirement, tax, or legal professionals before making any financial decisions or taking action based on the information presented. Davies Wealth Management assumes no liability for actions taken without seeking individualized professional advice.

Leave a Reply