Here is the full HTML content with up to 3 internal links added at the first natural occurrence of each keyword:

“`html

For high-net-worth retirees in Florida, Roth conversions and IRMAA represent one of the most consequential — and most frequently misunderstood — intersections in retirement tax planning. Done right, Roth conversions can dramatically reduce lifetime taxes, protect your estate, and create tax-free income for decades. Done carelessly, a single conversion decision can push your household into a higher Medicare Income-Related Monthly Adjustment Amount (IRMAA) tier and cost you thousands in unexpected premium surcharges.

This is not a hypothetical problem. It happens to successful retirees every year — often because their advisor focused narrowly on the conversion opportunity without stress-testing the Medicare consequences two years downstream.

Let’s walk through exactly how this trap works, who it affects most in Florida’s affluent retirement communities, and what a thoughtful, coordinated strategy looks like.

What Is IRMAA and Why Does It Matter to High-Net-Worth Retirees?

The Basic Mechanics of IRMAA

IRMAA stands for Income-Related Monthly Adjustment Amount. It is a surcharge added to your Medicare Part B and Part D premiums when your modified adjusted gross income (MAGI) exceeds certain thresholds. The Social Security Administration determines your IRMAA based on your tax return from two years prior — which is the critical detail most retirees miss.

In 2026, the standard Medicare Part B premium is approximately $185 per month. But for higher-income beneficiaries, that amount can climb to over $600 per month per person — meaning a married couple at the top IRMAA tier could pay more than $14,400 per year in Medicare Part B premiums alone, before adding Part D surcharges.

That is not a rounding error. For someone who planned their retirement income carefully around a $185 baseline, crossing an IRMAA threshold is a genuine financial shock — and one that arrives with almost no warning.

How Roth Conversions Trigger IRMAA

When you execute a Roth conversion, the converted amount is added to your ordinary income for that tax year. This increases your MAGI — and your MAGI is precisely what the Social Security Administration uses to calculate IRMAA two years later.

So a Roth conversion completed in 2026 will be reflected in your 2026 tax return, which SSA will review in 2028 to set your Medicare premiums. The two-year lookback is the hidden trip wire.

For a retiree with a $3 million IRA, even a modest $150,000 conversion can create a multi-year IRMAA surcharge that significantly erodes the tax benefit of the conversion itself — unless the planning accounts for it explicitly.

Why This Is Primarily a High-Net-Worth Problem

Mass-market retirement advice often encourages Roth conversions without distinguishing between income levels. For someone with a $400,000 IRA and modest Social Security income, IRMAA may never be a concern. But if you are a retired executive or business owner with:

- A traditional IRA or rollover IRA exceeding $1 million

- Taxable brokerage accounts generating dividends and capital gains

- Required Minimum Distributions (RMDs) beginning at age 73

- Social Security income that is 85% taxable

- Rental income, deferred compensation, or pension distributions

…then your baseline MAGI before any conversion may already be approaching — or sitting inside — an IRMAA tier. Adding a substantial Roth conversion on top of that baseline is where the real cost lives.

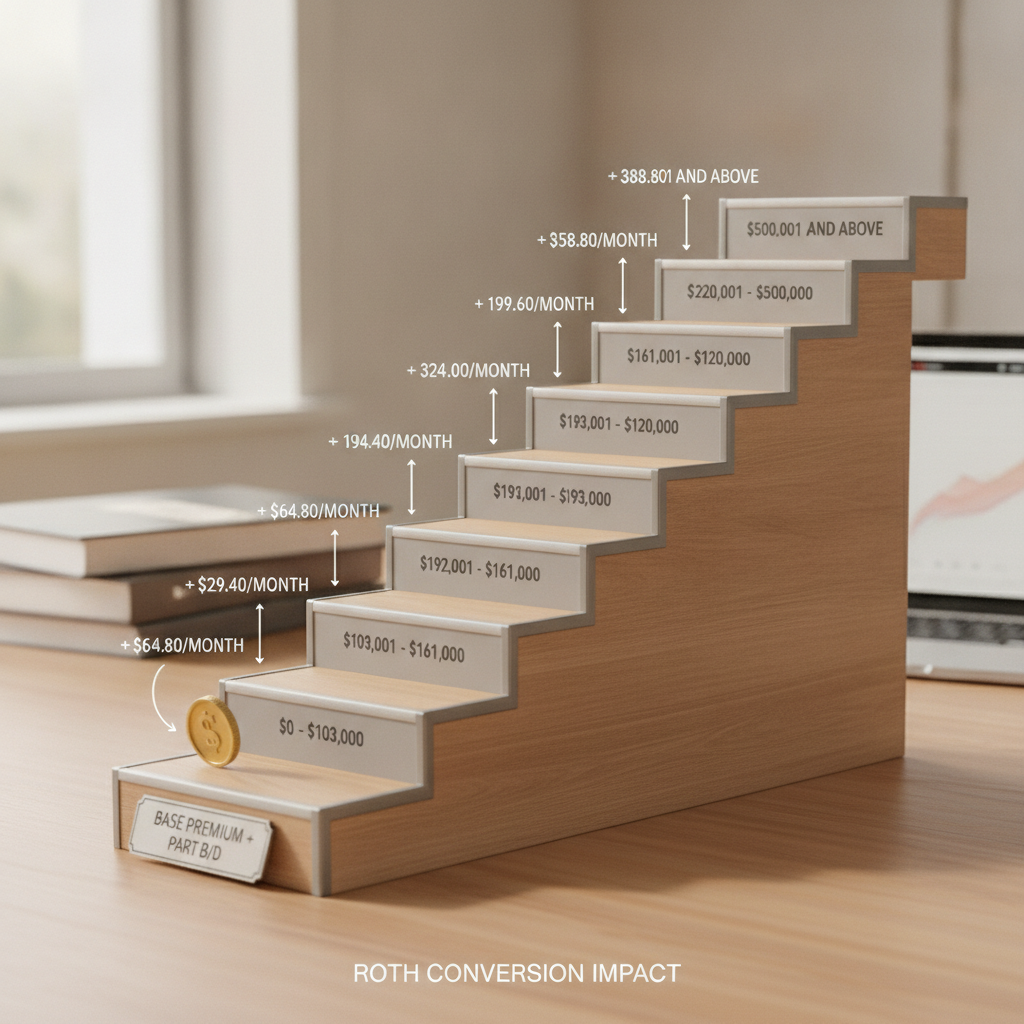

The 2026 IRMAA Thresholds and What They Mean in Practice

Current IRMAA Brackets for 2026

Understanding the exact income thresholds is essential before executing any Roth conversion strategy. The 2026 IRMAA tiers for Medicare Part B are structured as follows for individuals and married couples filing jointly:

| MAGI (Individual) | MAGI (Married Filing Jointly) | Monthly Part B Premium (per person) | Annual Cost (Couple) |

|---|---|---|---|

| Up to $106,000 | Up to $212,000 | ~$185 | ~$4,440 |

| $106,001 – $133,000 | $212,001 – $266,000 | ~$259 | ~$6,216 |

| $133,001 – $167,000 | $266,001 – $334,000 | ~$370 | ~$8,880 |

| $167,001 – $200,000 | $334,001 – $400,000 | ~$481 | ~$11,544 |

| $200,001 – $500,000 | $400,001 – $750,000 | ~$593 | ~$14,232 |

| Above $500,000 | Above $750,000 | ~$629 | ~$15,096 |

Note: Thresholds shown are approximate based on 2026 projected figures. Add Part D IRMAA surcharges for total premium impact. Consult a qualified financial professional for your specific situation. Source: Social Security Administration.

The Cliff Effect: Why $1 Over the Threshold Costs Thousands

IRMAA operates in tiers, not gradual slopes. Crossing from one bracket to the next by even one dollar of MAGI can trigger thousands of dollars in additional annual premiums. For a married couple, moving from the $212,000 threshold into the first IRMAA tier adds nearly $1,800 per year in Part B premiums alone.

This cliff effect makes precision planning non-negotiable. In practice, a Roth conversion that is not calibrated against the IRMAA thresholds — and against a retiree’s full income picture — can inadvertently push them two or even three tiers higher than necessary.

Five Strategies for Managing Roth Conversions and IRMAA Together

Strategy 1: IRMAA-Aware Conversion Sizing

The most fundamental discipline is sizing each year’s Roth conversion to stay within a specific IRMAA tier — or just below the threshold for the next tier. This requires projecting your full MAGI for the year, including:

- Taxable portfolio distributions and dividends

- Capital gains (realized or expected from rebalancing)

- Social Security income (85% of which is typically taxable)

- Any rental, pension, or deferred compensation income

- The Roth conversion amount itself

Once your baseline MAGI is established, you determine how much conversion “room” remains before crossing into the next IRMAA tier. This is not a one-size-fits-all number — it changes every year based on your income sources and the current brackets. Consult a qualified tax professional to model your specific scenario before executing any conversion.

Strategy 2: Multi-Year Conversion Laddering

Rather than executing one large Roth conversion, sophisticated financial planning often involves spreading conversions across 5–10 years in a deliberate ladder. This approach:

- Keeps annual MAGI below the most expensive IRMAA tiers

- Allows for adjustment each year based on actual income

- Can be coordinated with the window between retirement and RMD age (73)

- Creates a growing pool of tax-free Roth assets over time without a single-year income shock

For a 60-year-old Florida retiree with a $2.5 million IRA, the window between retirement and age 73 is often the most valuable planning period available. Systematic annual conversions during that window — calibrated to IRMAA thresholds — can meaningfully reduce the eventual RMD burden and its downstream IRMAA impact. Learn more about Roth IRA rules from the IRS.

Strategy 3: QCD Stacking to Reduce MAGI

Once you reach age 70½, Qualified Charitable Distributions (QCDs) allow you to transfer up to $105,000 per year (2026 limit, indexed for inflation) directly from your IRA to a qualified charity. The distribution is excluded from your MAGI entirely — meaning it satisfies your RMD obligation without inflating your income.

For philanthropically inclined clients, QCD stacking is a powerful IRMAA management tool. By directing charitable giving through QCDs instead of writing personal checks (or using donor-advised funds for deductibility), you reduce the MAGI that determines your IRMAA tier — and potentially create room for a larger Roth conversion in the same year without crossing a threshold.

Strategy 4: Timing Capital Gains and Roth Conversions Separately

Many high-net-worth retirees inadvertently stack income in the same year without realizing it. A classic example: they execute a Roth conversion AND realize substantial long-term capital gains from rebalancing their taxable portfolio in the same tax year. Both flows increase MAGI and both feed IRMAA calculations.

Coordinating the timing of capital gains realization and Roth conversions across different tax years — even when both strategies are sound independently — can prevent unnecessary IRMAA tier escalation. This is precisely the kind of coordination that requires a comprehensive view of your entire financial picture, not siloed advice from different professionals. Our comprehensive wealth management services are built around this kind of integrated planning.

Strategy 5: The IRMAA Appeal Process for Life-Changing Events

If a one-time Roth conversion or business sale pushes you into a high IRMAA tier, and your income will be substantially lower going forward, you can appeal your IRMAA determination using SSA Form SSA-44. The IRS and Social Security Administration recognize certain life-changing events — including retirement, divorce, and loss of a spouse — that may qualify you for a reduced IRMAA calculation based on more recent income.

This is not a loophole. It is a formal, documented process that many retirees simply do not know exists. For those who experienced an unusually high-income year due to a Roth conversion, business liquidation, or deferred compensation payout, the appeal process can recover thousands of dollars in otherwise permanent premium increases. See Kiplinger’s Medicare IRMAA guide for additional context on the appeal process.

Florida-Specific Considerations for Roth Conversions and IRMAA

Why Florida Retirees Face Unique IRMAA Exposure

Florida has no state income tax — which is one of the primary reasons affluent retirees relocate to the Treasure Coast, Palm Beach, and Southwest Florida communities. But the absence of state income tax creates a planning nuance that many advisors overlook.

In states with income taxes, retirees sometimes limit Roth conversions to manage both federal and state tax exposure. In Florida, there is no state tax friction to consider — which tempts some retirees to convert more aggressively than is optimal when IRMAA is factored into the total cost equation.

The result: Florida retirees who convert too aggressively often pay more in Medicare IRMAA surcharges than they saved by avoiding state income taxes on the conversion itself. The math must be done holistically. Consult a qualified tax professional before adjusting your conversion strategy based on state tax considerations.

Roth Conversions and IRMAA in the Context of Florida Estate Planning

Florida has no estate tax at the state level, and the federal estate tax exemption in 2026 is approximately $13.99 million per individual ($27.98 million per married couple). For estates approaching or exceeding these thresholds, large traditional IRAs represent both a taxable estate asset and a future income tax burden for heirs.

Converting portions of a traditional IRA to Roth — despite the near-term IRMAA cost — may be strategically justified as part of a multi-generational wealth transfer plan. Roth IRAs pass to beneficiaries without income tax obligation on the balance. The question is not whether the IRMAA cost is zero (it rarely is), but whether the long-term estate and income tax benefit outweighs the premium surcharge over a realistic planning horizon. For complex estate situations, schedule a discovery conversation with our team to model the tradeoffs specific to your situation.

How High-Net-Worth Clients Need Different Advice Than Mass-Market Investors

The Mass-Market Roth Conversion Approach

Standard retirement advice often promotes Roth conversions as universally beneficial — convert now, pay taxes at today’s rates, enjoy tax-free growth forever. This advice is not wrong. It is just incomplete for clients with complex, multi-source income profiles.

For someone with a $250,000 IRA and no other taxable income in retirement planning, IRMAA may never become a meaningful factor. The math is relatively straightforward, and a modest annual conversion makes obvious sense.

Why the HNW Situation Demands a Different Framework

For a retired executive or business owner with a $3 million IRA, significant taxable portfolio income, and Social Security benefits, the Roth conversion decision involves at least five interconnected variables:

- Current federal tax bracket and marginal rate

- IRMAA tier impact two years forward

- State income tax environment (Florida vs. a high-tax state if recently relocated)

- Future RMD projections and their estimated IRMAA impact if the IRA is left unconverted

- Estate and beneficiary tax implications over a 20–30 year horizon

These variables interact with each other in ways that are genuinely difficult to model without purpose-built financial planning software and an advisor experienced with high-income clients. This is precisely where a fee-based fiduciary — whose compensation is not tied to product sales — provides its greatest value. Learn more about the importance of working with a fiduciary advisor.

Frequently Asked Questions: Roth Conversions and IRMAA

Does a Roth conversion directly increase my IRMAA premiums?

Yes — a Roth conversion increases your MAGI in the year of conversion, and your MAGI from that tax year is what the Social Security Administration uses to set your Medicare premiums two years later. A large or poorly timed conversion can push you into a higher IRMAA tier for one or more years. Consult a qualified tax professional to model the impact before converting.

Can I reverse a Roth conversion if I accidentally triggered IRMAA?

No. The IRS eliminated the Roth recharacterization option for conversions in 2018 as part of the Tax Cuts and Jobs Act. Once a conversion is executed, it is permanent for that tax year. This is why pre-conversion planning — not after-the-fact correction — is essential.

How do I appeal an IRMAA determination caused by a one-time Roth conversion?

You can submit SSA Form SSA-44 to appeal your IRMAA determination if you experienced a life-changing event such as retirement, divorce, or the death of a spouse. A one-time income spike from a Roth conversion, business sale, or deferred compensation payout may qualify for consideration if your current income is substantially lower. Contact Social Security directly or work with a financial planner experienced in IRMAA appeals.

What is the optimal MAGI target for avoiding the first IRMAA tier in 2026?

For 2026, a married couple filing jointly must keep their MAGI at or below approximately $212,000 to avoid the first IRMAA surcharge. Individuals must stay at or below approximately $106,000. Note that these thresholds apply to your 2026 income, which will determine your 2028 Medicare premiums. Thresholds are adjusted annually for inflation — verify current figures with a qualified advisor or at SSA.gov.

Should I stop doing Roth conversions to avoid IRMAA entirely?

Not necessarily. The correct answer depends on your full income picture, estate goals, and time horizon. For many high-net-worth retirees, the long-term benefits of Roth conversion — reduced RMDs, tax-free growth, and estate efficiency — outweigh the IRMAA costs when the conversion is sized and timed thoughtfully. The goal is not to avoid conversions but to execute roth conversions and irmaa planning in a coordinated, strategic way that minimizes unnecessary premium surcharges.

Working With a Fee-Based Fiduciary on Your Roth Conversion and IRMAA Strategy

Roth conversions and IRMAA planning are not independent decisions — they are two levers in a complex system that also includes your tax bracket, estate plan, investment portfolio, Social Security timing, and healthcare cost projections. Getting one variable right while ignoring the others is how well-intentioned strategies produce expensive surprises.

At Davies Wealth Management, we work exclusively as a fee-based fiduciary firm. We do not have proprietary products to sell, and any product compensation is fully disclosed. Our only obligation is to your financial wellbeing — which means building conversion strategies that account for IRMAA from the outset, not as an afterthought.

If you are a Florida retiree or pre-retiree with a substantial IRA balance, a multi-source income picture, or a desire to leave a tax-efficient legacy, this is the kind of integrated planning that can make a meaningful difference over your lifetime.

Ready to understand exactly how Roth conversions and IRMAA interact in your specific situation? Download our Medicare IRMAA Planning Guide to see the full framework we use with clients — including bracket thresholds, appeal strategies, and conversion sizing tools.

📥 Download our Medicare IRMAA Planning Guide — and stop letting a two-year lookback rule silently drain your retirement income.

Ready for personalized guidance from a fee-based fiduciary? Book a complimentary phone call and let’s talk through what a smarter Roth conversion strategy looks like for your retirement.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

“`

Leave a Reply