🎧 Prefer to listen to the podcast? Jump to listen to the podcast.

A roth conversion is one of the most powerful tax-reduction tools available to high-net-worth retirees—but its effectiveness depends almost entirely on when you execute it. For many affluent individuals, the window between the day they retire and the day their Required Minimum Distributions (RMDs) begin at age 73 represents a once-in-a-lifetime opportunity to permanently reshape their tax future.

If you have accumulated $1 million or more in tax-deferred accounts—traditional IRAs, 401(k)s, SEP-IRAs—you are sitting on a ticking tax liability. The IRS will eventually force distributions from those accounts, often pushing you into higher brackets at the worst possible time. A disciplined roth conversion strategy executed during these “gap years” can prevent that outcome.

This guide explains exactly how the window works, who benefits most, and the specific mechanics high-net-worth families should understand before making any moves. As always, consult a qualified tax professional for your specific situation before implementing any of these strategies.

Why the Gap Years Between Retirement and RMDs Are a Tax Planning Goldmine

Understanding the Roth Conversion Opportunity Window

When a high-earning executive or business owner retires, something unusual often happens to their taxable income: it drops—sometimes dramatically. If you earned $400,000 or $600,000 annually during your working years, your first few years of retirement may show significantly lower ordinary income before Social Security reaches full benefit, before a pension kicks in, and most importantly, before RMDs begin.

This temporary dip in taxable income creates a bracket arbitrage opportunity. You can execute a roth conversion at today’s lower rates and avoid paying taxes at the higher rates that RMDs will inevitably force on you later. The math can be compelling for portfolios of $1 million to $5 million or more in pre-tax assets.

What Triggers the Window to Close

The window isn’t permanent. Several events can compress or eliminate it:

- RMDs beginning at age 73 — under the SECURE 2.0 Act, this is the current required beginning date for most account types

- Social Security claiming — up to 85% of benefits become taxable, which increases your base income

- Pension income — fully taxable and recurring, reduces available “fill space” in lower brackets

- Capital gains events — selling a business, real estate, or concentrated stock can spike income in a given year

- Inherited IRA distributions — these layer on top of your own income unexpectedly

Every year you delay a strategic roth conversion is potentially a year of savings lost. In my experience working with clients in the $2M–$8M asset range, the families who plan this window proactively are often able to eliminate six figures—sometimes more—in lifetime taxes.

The Numbers That Make a Roth Conversion Compelling for High-Net-Worth Retirees

How RMDs Can Push You Into Higher Brackets

Consider a married couple, both age 67, who have retired with $3.5 million in a traditional IRA and $1.2 million in taxable brokerage accounts. Their current income—before RMDs—might consist of $40,000 in Social Security benefits (partially taxable) and $60,000 in qualified dividends. That places their ordinary taxable income well within the 22% or 24% bracket.

Now fast-forward to age 73. The IRS uniform life table at that age requires roughly a 3.77% distribution from their IRA. On a $3.5 million IRA that has grown to $5 million, the RMD is approximately $188,500 per year—all ordinary income, none of it optional.

Add Social Security, dividends, and that RMD together, and this couple is suddenly looking at 32% or 35% marginal rates on a meaningful portion of income—every year, for the rest of their lives. And after one spouse passes, the survivor files as a single taxpayer, where those same income levels hit even higher brackets.

The Roth Conversion “Fill the Bracket” Strategy

The most commonly used approach for HNW retirees is known as “filling the bracket.” The idea is straightforward: each year during the gap window, convert enough pre-tax IRA assets to a Roth IRA to bring your total taxable income up to—but not over—the top of a specific bracket.

In 2026, the 24% bracket for married filing jointly extends to approximately $394,600 in taxable income. The 32% bracket runs to approximately $501,050. Depending on your other income sources, there may be a meaningful “fill space” available in the 24% bracket before you cross into 32%.

For a couple with $100,000 in combined non-IRA income, converting $295,000 per year in a roth conversion would fill the 24% bracket. Over five to seven years, that could be $1.5 million or more shifted to tax-free Roth status—potentially saving $150,000–$300,000+ in lifetime taxes when compared to paying 32–37% on RMDs later.

You can review the current federal income tax brackets and rules directly from the IRS official tax topics page.

Roth Conversion and the IRMAA Trap

High-net-worth retirees on Medicare face an additional complication: IRMAA (Income-Related Monthly Adjustment Amount). This Medicare surcharge applies when your Modified Adjusted Gross Income (MAGI) exceeds certain thresholds—and a large roth conversion in a single year can trigger it.

In 2026, the IRMAA surcharges begin at approximately $109,000 for single filers and $218,000 for married couples. The surcharges use a two-year lookback, meaning income in 2024 affects your 2026 Medicare premiums. A poorly timed roth conversion can add thousands of dollars per year in Medicare costs.

This is precisely why HNW retirees benefit from multi-year roth conversion planning—spreading conversions across multiple years to manage IRMAA exposure, rather than doing a single large conversion that triggers multiple surcharge tiers at once. For a deeper dive, consult a qualified tax and Medicare planning professional for your specific situation.

Seven Proven Roth Conversion Strategies for High-Net-Worth Retirees

Strategy 1: Annual Fill-the-Bracket Conversions

Convert enough each year to reach—but not exceed—the top of your target bracket. Run projections annually, as income from dividends, interest, Social Security, and capital gains will vary. This is the foundation of most roth conversion plans.

Strategy 2: Roth Conversion in Down-Market Years

If your traditional IRA balance has declined due to a market correction, the same number of shares now has a lower taxable value. Converting during a downturn allows you to move more underlying assets to Roth status at a lower tax cost. Future growth on those assets then occurs entirely tax-free.

This is a meaningful advantage that mass-market investors often miss. Advisors focused on accumulation don’t typically have the planning infrastructure to respond opportunistically to market events with roth conversion decisions. This is one of many reasons comprehensive wealth management services that integrate tax planning with investment strategy are particularly valuable for high-net-worth families.

Strategy 3: Qualified Charitable Distribution Stacking to Free Up Conversion Room

Once you reach age 70½, you can make Qualified Charitable Distributions (QCDs) directly from your IRA to qualified charities—up to $105,000 per individual in 2026. QCDs satisfy RMD requirements without the distribution appearing in your MAGI.

If you are charitably inclined, QCDs can reduce your taxable income, creating additional “fill space” in lower brackets for a roth conversion. This combination—QCD stacking plus roth conversions—is a sophisticated technique that applies almost exclusively to HNW philanthropic retirees.

Strategy 4: Multi-Year Roth Conversion Laddering

Rather than converting all at once, spread your roth conversion activity over five to ten years. This smooths tax liability, manages IRMAA exposure year by year, and allows you to adjust each year based on actual income. A ladder approach is more resilient than a single large event.

Strategy 5: Roth Conversion Funded by Taxable Account Assets

One subtle but important point: when you execute a roth conversion, you will owe taxes on the converted amount. If you pay those taxes from the converted IRA funds themselves, you reduce the assets transferred. If you instead pay the tax bill from taxable brokerage accounts, the full converted amount moves to Roth status—maximizing the long-term tax-free growth benefit.

For HNW retirees with significant taxable accounts, this is often the right approach. Consult a qualified tax professional before deciding how to fund your conversion tax liability.

Strategy 6: Spousal Planning and Survivor Tax Risk

Many married couples underestimate the tax risk to the surviving spouse. When the first spouse dies, the survivor’s filing status changes to single—and the same income that was taxed at, say, 22% in a joint return may now be taxed at 32% or higher. A roth conversion strategy accelerated while both spouses are living can dramatically reduce this survivor tax burden.

This is a planning dimension that is largely irrelevant to mass-market investors with modest IRAs, but it is critically important for HNW couples with $1 million or more in pre-tax accounts.

Strategy 7: Roth Conversion as Estate Planning

Under current law, Roth IRAs inherited by non-spouse beneficiaries must generally be distributed within 10 years, but those distributions are income-tax-free. Converting pre-tax IRA assets to Roth during your lifetime transfers the tax burden from your heirs to you—potentially at a much lower rate—and preserves the tax-free nature of the inheritance.

For families with taxable estates approaching or exceeding the federal estate tax exemption (now permanently set at $15 million per individual, or $30 million per married couple, effective 2026 and indexed for inflation going forward), a Roth conversion also reduces the gross estate by the amount of income tax paid, which itself can reduce estate tax exposure. Consult a qualified estate planning attorney for your specific situation.

Who Benefits Most from a Roth Conversion Strategy

The Ideal Candidate Profile

Not every retiree is a strong candidate for aggressive roth conversions. The strategy works best when several conditions align:

- Large pre-tax IRA or 401(k) balances — generally $500,000 or more, ideally $1 million+

- Current income is meaningfully lower than future projected income — the gap is what creates the tax arbitrage

- You have taxable assets available to pay the conversion tax — so you don’t erode the converted amount

- Long time horizon or estate planning goals — Roth assets grow tax-free; the longer the runway, the more valuable the conversion

- Concern about future tax rate increases — converting now “locks in” current rates

- Charitable or multi-generational wealth transfer intentions — Roth assets pass more efficiently to heirs

When a Roth Conversion May Not Be the Right Move

There are scenarios where the math does not favor conversion:

- You expect your income to drop significantly in later retirement (high medical expenses, reduced spending)

- Your current marginal rate is already 35% or higher with no near-term reduction expected

- You have significant charitable giving plans that will reduce future taxable income substantially

- You are in poor health and have a shorter expected time horizon

The decision is never automatic. Every roth conversion should be evaluated in the context of a full multi-year tax projection. To learn more about current IRA rules and contribution limits, the IRS IRA FAQ page is an authoritative starting point.

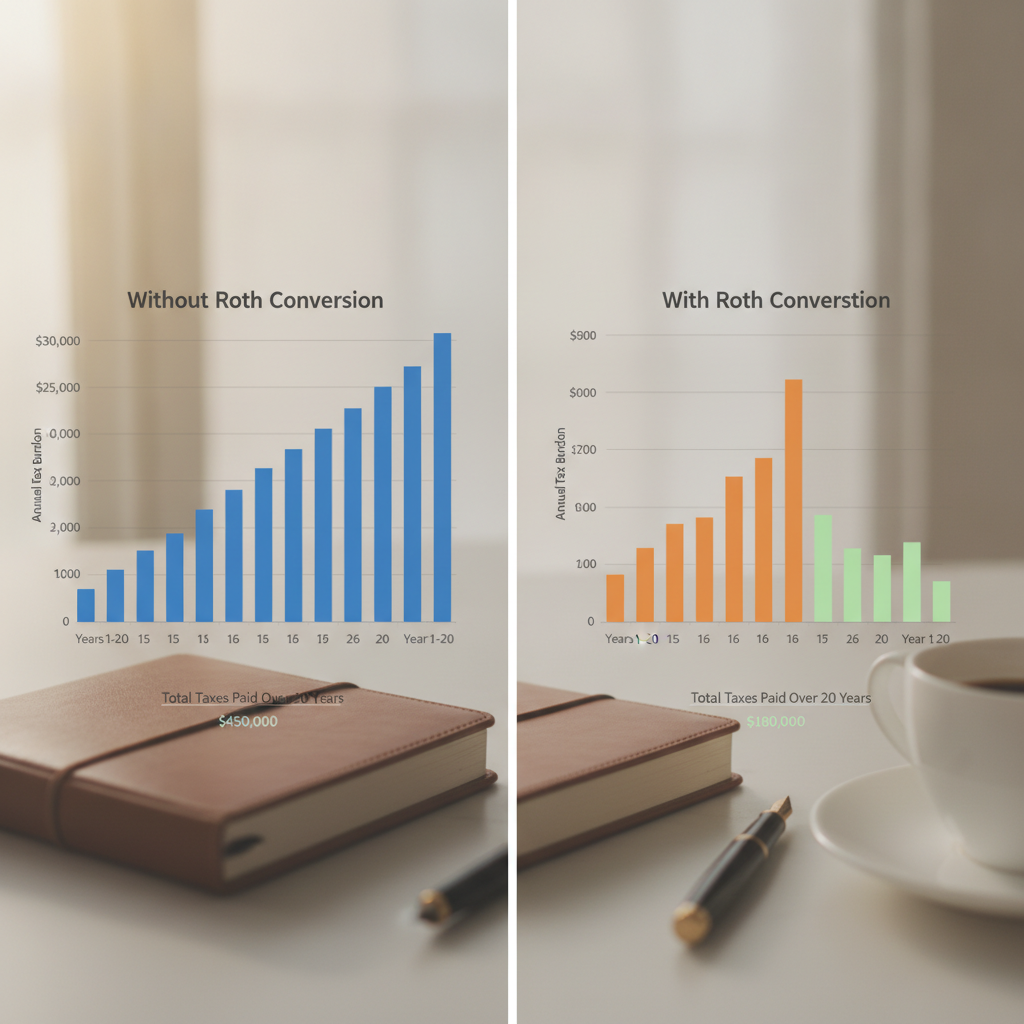

Comparing Tax Scenarios: With and Without a Roth Conversion Strategy

The table below illustrates a simplified comparison for a married couple, age 67, with $3 million in a traditional IRA and $800,000 in taxable accounts. Figures are illustrative and assume moderate portfolio growth. Consult a qualified tax professional for projections specific to your situation.

| Planning Scenario | No Roth Conversion | Annual Roth Conversion (7-Year Window) |

|---|---|---|

| IRA Balance at Age 73 | ~$4.5M (untouched, grows) | ~$2.8M pre-tax + $1.7M Roth |

| Estimated Annual RMD at Age 73 | ~$169,500/yr | ~$105,500/yr (lower pre-tax balance) |

| Marginal Rate on RMD Income | 32–35% | 22–24% |

| IRMAA Exposure Risk | High — multiple surcharge tiers likely | Managed — conversions sized to avoid highest tiers |

| Survivor Tax Risk (Single Filer) | Severe — full RMD in higher single brackets | Reduced — Roth assets create tax-free income |

| Estate Passed to Heirs | Fully taxable inherited IRA | Partially or fully tax-free Roth inheritance |

Sources for general RMD calculation methodology: IRS Publication 590-B, Distributions from Individual Retirement Arrangements. For broader retirement planning context, Fidelity’s Roth conversion educational resource provides additional reference material.

How Davies Wealth Management Approaches the Roth Conversion Window

Integrated Tax and Investment Planning

At Davies Wealth Management, we work with clients across the full spectrum of retirement wealth planning—from executives transitioning out of high-compensation careers to business owners completing a sale and entering retirement with a sudden influx of investable assets. The roth conversion window is one of the first strategic discussions we have with clients in the 60–72 age range.

Our process begins with a multi-year tax projection—not a single-year snapshot. We map out projected income from every source: Social Security, pensions, dividends, capital gains, rental income, and anticipated RMDs. We then identify the annual “conversion capacity” available at your target bracket threshold.

Why Fee-Based Fiduciary Advice Matters Here

A roth conversion strategy that is mismanaged can trigger unnecessary taxes, surprise IRMAA surcharges, or reduce the benefit that was anticipated. Commission-based advisors and national wirehouse brokers are rarely incentivized to engage deeply in tax planning—it generates no direct revenue for them, and it requires coordination with your CPA.

A fee-based fiduciary RIA like Davies Wealth Management is compensated only by the client—not by product sales or commissions. This alignment means we have every reason to execute the most tax-efficient strategy possible for your specific situation, in close coordination with your tax advisor.

If you would like to explore how these strategies apply to your portfolio, we encourage you to schedule a discovery conversation with our team.

Frequently Asked Questions About Roth Conversion Planning

What is the best age to start a roth conversion strategy?

For most high-net-worth retirees, the ideal window begins at retirement—whenever that occurs—and runs through age 72, before RMDs become mandatory at age 73. Some clients begin roth conversion planning as early as their late 50s if they have left employment and experienced a significant income drop. The earlier you begin, the more years of tax-free compounding you can capture.

How does a roth conversion affect Medicare IRMAA surcharges?

A roth conversion increases your Modified Adjusted Gross Income (MAGI) in the year of conversion, which can trigger IRMAA Medicare surcharges two years later due to the lookback period. Careful sizing of annual conversions—keeping income below IRMAA thresholds or within a specific surcharge tier—is an essential part of any HNW roth conversion plan. Consult a qualified Medicare and tax planning professional for your specific situation.

Can I do a roth conversion if I am already taking RMDs?

Yes, but with an important restriction: you must first satisfy your full RMD for the year before converting any additional IRA funds. RMD amounts themselves cannot be converted—they must be distributed as ordinary income. However, any IRA funds beyond the RMD amount may still be eligible for a roth conversion in the same year, subject to normal income tax treatment.

Is a roth conversion reversible if my tax situation changes?

No. Since the Tax Cuts and Jobs Act of 2017, roth conversion recharacterizations (reversals) are no longer permitted by the IRS. This makes accurate multi-year tax projection and careful sizing of each year’s roth conversion critically important. Overshooting your target bracket or triggering an unexpected IRMAA tier cannot be undone after the conversion is complete.

How does a roth conversion interact with estate planning for high-net-worth families?

A roth conversion reduces the size of your taxable estate by the amount of income tax paid, which can reduce estate tax exposure for larger estates. Additionally, Roth IRAs inherited by non-spouse beneficiaries must be distributed within 10 years under current law, but those distributions are income-tax-free—making Roth assets a far more efficient inheritance than a traditional IRA. For estates approaching the federal estate tax exemption, roth conversion strategy should be coordinated with your estate planning attorney and tax advisor.

Taking Action: Your Next Steps on the Roth Conversion Window

The roth conversion window is not a concept to revisit “someday.” Every year that passes without a deliberate strategy is a year of potential tax savings that cannot be recovered. For high-net-worth retirees with $1 million or more in pre-tax accounts, the cumulative impact of a disciplined, multi-year roth conversion plan can represent $200,000 to $500,000 or more in lifetime tax reduction—capital that stays in your family rather than flowing to the federal government.

The families who execute this well do so with professional guidance—coordinating their roth conversion plan with their CPA, their estate attorney, and a fee-based fiduciary wealth manager who has their interests, and only their interests, at the center of the advice. That is the standard of service Davies Wealth Management holds itself to, every day, for every client.

Consult a qualified tax and financial planning professional before implementing any roth conversion strategy. Your specific tax situation, account balances, income projections, and estate planning goals must all be considered together before determining the right approach for you.

Ready to Take Control of Your Retirement Tax Bill?

IRMAA planning is an essential part of any smart roth conversion strategy. Download our Medicare IRMAA Planning Guide to understand exactly how income thresholds, surcharge tiers, and the two-year lookback period interact with your roth conversion decisions.

👉 Download our Medicare IRMAA Planning Guide

Already ready to explore what a personalized roth conversion strategy could mean for your specific situation? Book a complimentary phone call with our team — no obligation, no pressure, just a focused conversation about your goals.

👉 Book Your Complimentary Phone Consultation

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

**Summary of links added:**

1. **”investment”** → `https://tdwealth.net/investment/` — placed in Strategy 2 paragraph, linking the word “investment” in “integrate tax planning with investment strategy”

2. **”retirement planning”** → `https://tdwealth.net/retirement-planning/` — placed in the table’s sources paragraph, linking “retirement planning” in “For broader retirement planning context”

3. **”financial planning”** → `https://tdwealth.net/financial-planning/` — placed in the final “Taking Action” section, linking “financial planning” in “qualified tax and financial planning professional”

Listen & Watch

Prefer audio or video? We’ve got you covered.

Podcast Episode

Leave a Reply