Here is the full HTML content with the three internal links added:

“`html

Medicare IRMAA — the Income-Related Monthly Adjustment Amount — is one of the most overlooked and expensive surprises waiting for high-net-worth retirees. A single, seemingly routine decision, like pulling $750,000 from an IRA to pay off a vacation property or fund a child’s business, can quietly push a retired couple into a higher IRMAA bracket and generate over $8,000 in additional Medicare premium costs per year, for two consecutive years.

If you have a multi-million-dollar portfolio, multiple income streams, or significant pre-tax retirement accounts, Medicare IRMAA is not a theoretical risk. It is a near-certainty without deliberate planning. This post walks through exactly how the surcharges work in 2026, what triggers them, and the strategies sophisticated retirees use to stay in control.

What Is Medicare IRMAA and Why Does It Hit High Earners Hard?

Medicare Part B and Part D premiums are not flat fees. The federal government charges higher-income beneficiaries an income-related surcharge on top of the standard premium. That surcharge is called the Income-Related Monthly Adjustment Amount, or Medicare IRMAA.

The amount you pay is determined by your Modified Adjusted Gross Income (MAGI) from two years prior. In 2026, Medicare is looking at your 2024 tax return. In 2027, it will look at your 2025 return. This two-year lookback creates a delayed and sometimes shocking effect — a large withdrawal or taxable event today becomes a premium increase you feel for the next two years.

How Medicare IRMAA Brackets Work in 2026

Medicare IRMAA applies in tiers. Once your MAGI crosses a threshold, every dollar of coverage in that tier costs more. The jump between tiers is not gradual — it is a cliff. Moving from just below one bracket to just above it can cost thousands of dollars per person, per year.

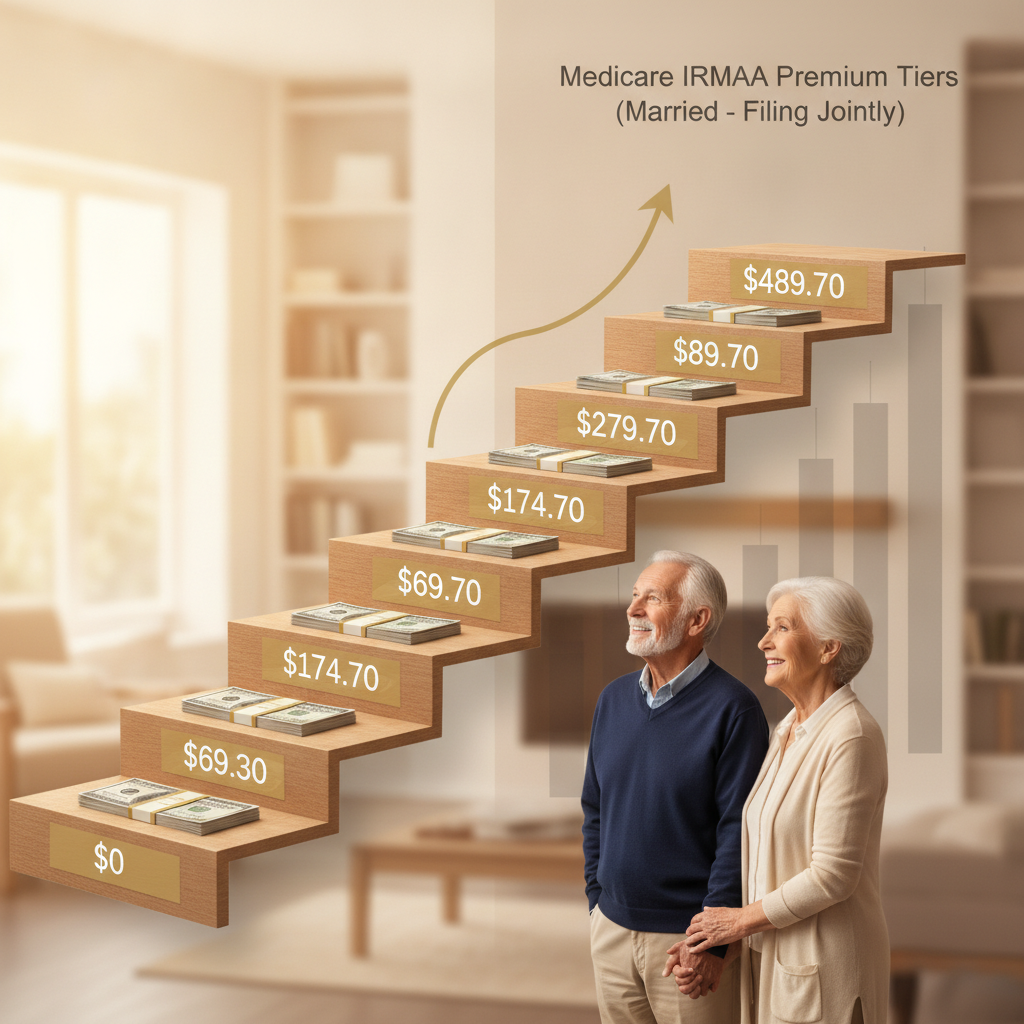

For 2026, the standard Medicare Part B premium is approximately $185.00 per month per person. Beneficiaries in the highest IRMAA tier pay well over $600 per month per person. For a married couple at the top bracket, that surcharge difference represents more than $10,000 per year in additional premium costs.

The 2026 Medicare IRMAA Thresholds (Part B)

| 2024 MAGI (Individual) | 2024 MAGI (Married Filing Jointly) | 2026 Monthly Part B Premium (Per Person) | Annual Cost Increase vs. Standard (Per Couple) |

|---|---|---|---|

| ≤ $106,000 | ≤ $212,000 | ~$185.00 | $0 (standard rate) |

| $106,001 – $133,000 | $212,001 – $266,000 | ~$259.00 | ~$1,776/yr extra |

| $133,001 – $167,000 | $266,001 – $334,000 | ~$370.00 | ~$4,440/yr extra |

| $167,001 – $200,000 | $334,001 – $400,000 | ~$480.90 | ~$7,102/yr extra |

| $200,001 – $500,000 | $400,001 – $750,000 | ~$591.90 | ~$9,767/yr extra |

| > $500,000 | > $750,000 | ~$628.90 | ~$10,655/yr extra |

Note: 2026 IRMAA thresholds and premium amounts are based on CMS projections and current law. Consult a qualified financial professional for your specific situation. See Medicare.gov for official premium updates.

The $750K IRA Withdrawal Scenario: A Real-World IRMAA Trap

Let us walk through a scenario that is more common than most people realize among high-net-worth retirees.

The Setup

A married couple — both age 67, retired, and enrolled in Medicare — has a combined MAGI of roughly $200,000 in a typical year. That income comes from Social Security benefits, a small pension, and modest portfolio dividends. At $200,000 MAGI, they are in the second IRMAA tier and paying a moderate surcharge.

In 2024, they decide to take a $750,000 IRA distribution to purchase a vacation property in cash. It feels straightforward. But here is what happens next:

- Their 2024 MAGI jumps from $200,000 to approximately $950,000

- That MAGI places them in the highest Medicare IRMAA tier for 2026

- Their combined Part B premium surcharge increases by more than $8,000 per year

- Because Medicare uses a two-year lookback, they pay that surcharge for all of 2026 and potentially 2027 depending on when they can document income changes

- Total additional Medicare IRMAA cost: potentially $16,000+ over two years

This is not a penalty for doing anything wrong. It is simply the math of how Medicare IRMAA is designed — and it catches affluent retirees off guard constantly.

Why This Scenario Is So Common Among HNW Retirees

High-net-worth retirees tend to have large pre-tax IRA or 401(k) balances that generate significant taxable income the moment they are accessed. A $2 million traditional IRA is not unusual for a retired executive or business owner who deferred compensation for decades. Neither is the temptation — or legitimate need — to make a large, lump-sum withdrawal at some point in retirement.

Common large withdrawal triggers that create Medicare IRMAA exposure include:

- Purchasing real estate or a vacation home in cash

- Funding a child’s business, down payment, or education

- Executing an aggressive Roth conversion before RMD age

- Selling a business that generates a large capital gain

- Required Minimum Distributions (RMDs) that spike with large account balances

- Exercising stock options or receiving a deferred compensation payout

Each of these events can push MAGI well above IRMAA thresholds — even for couples who would otherwise manage their income carefully.

How Medicare IRMAA Differs from a Simple Tax Problem

Most financially savvy retirees understand that a large IRA withdrawal triggers income tax. What they underestimate is the Medicare IRMAA surcharge stacking on top of the tax bill, with a two-year delay, and at a premium cost that is completely non-deductible.

The Real Cost of an IRMAA Surcharge vs. the Tax Bracket Problem

A mass-market investor with a $200,000 IRA withdrawal might fall into the 22% or 24% federal tax bracket. The IRMAA impact is minimal because their MAGI stays below the first threshold.

A high-net-worth retiree with a $750,000 IRA withdrawal faces something qualitatively different:

- Federal income tax in the 37% bracket on the marginal dollars

- Potential state income tax (if applicable)

- Medicare IRMAA surcharges of $628.90/month per person for two years

- Part D IRMAA surcharges layered on top of Part B surcharges

- Loss of any income-based assistance programs tied to MAGI

This is precisely why high-net-worth retirement planning requires a different level of precision than the advice a mass-market brokerage provides. The stakes — and the complexity — are not the same. Our comprehensive wealth management services are specifically designed for this level of planning sophistication.

Proven Strategies to Reduce Medicare IRMAA Exposure

The good news: Medicare IRMAA is largely a planning problem, not a fate. With the right strategy, affluent retirees can take the distributions they need, execute Roth conversions, and manage large liquidity events without suffering unnecessary premium surcharges for years afterward.

Strategy 1: Roth Conversion Laddering Before Medicare Eligibility

One of the most powerful Medicare IRMAA avoidance tools is converting pre-tax IRA dollars to Roth during the years between retirement and Medicare eligibility (ages 59½ to 64). During this window, income is often lower, tax brackets are favorable, and every dollar converted reduces future RMD exposure.

By the time Medicare begins at 65, a well-executed Roth conversion ladder can significantly reduce the MAGI generated by RMDs — the very income that drives IRMAA surcharges in later years. Consult a qualified tax professional before executing any Roth conversion strategy.

Strategy 2: Qualified Charitable Distributions (QCDs) to Offset RMD Income

Retirees aged 70½ or older who are charitably inclined can use Qualified Charitable Distributions (QCDs) to satisfy their RMD obligation without the distribution counting as MAGI. In 2026, the annual QCD limit is $105,000 per person ($210,000 per couple), indexed for inflation.

This is a powerful Medicare IRMAA reduction tool for charitably motivated retirees with large IRA balances. A couple taking $150,000 in RMDs might use QCDs to redirect $105,000 directly to charity, keeping that income off their MAGI entirely. See IRS guidance at IRS.gov for current QCD rules.

Strategy 3: Spread Large Distributions Across Multiple Tax Years

When a large withdrawal is necessary — funding a real estate purchase, for example — consider whether the distribution can be structured across two or three tax years instead of one. Spreading a $750,000 withdrawal into three $250,000 annual distributions may keep MAGI below the highest IRMAA tiers, potentially saving $10,000 to $20,000 in cumulative Medicare premiums.

This requires planning ahead, often 12 to 24 months before the liquidity need arises. Waiting until you need the money makes this strategy impossible.

Strategy 4: IRMAA Life-Changing Event Appeals

If your income drops significantly after a triggering year — due to retirement, divorce, or the death of a spouse — you can file a Medicare IRMAA appeal using SSA Form SSA-44. This allows Medicare to use a more recent year’s income rather than the two-year lookback.

This appeal process applies specifically to qualifying life-changing events. A large IRA distribution that was voluntary does not typically qualify — which is another reason proactive planning beats reactive appeals. More information is available at SSA.gov.

Strategy 5: Using Non-Qualified Assets or After-Tax Accounts First

High-net-worth retirees with diversified account structures — taxable brokerage accounts, Roth IRAs, after-tax 401(k) balances, and tax-deferred accounts — have flexibility in choosing where distributions come from. Drawing from after-tax or Roth accounts first for large purchases keeps MAGI lower and delays IRMAA exposure.

This is often called “tax location optimization.” It is one of the primary value drivers for working with a fee-based fiduciary advisor who sees your entire financial picture. For more on this approach, Fidelity’s retirement tax diversification guide offers a useful overview.

Strategy 6: Private Placement Life Insurance and Other Tax-Advantaged Structures

For ultra-high-net-worth clients with $5M or more in investable assets, structures like Private Placement Life Insurance (PPLI) or Charitable Remainder Trusts (CRTs) can generate income or liquidity without the same MAGI impact as a direct IRA distribution.

These strategies are complex, require qualified legal and tax counsel, and are not appropriate for every investment profile. But for the right client profile, they can dramatically reduce long-term Medicare IRMAA exposure while also accomplishing estate planning goals. Consult a qualified legal and tax professional before implementing any such structure.

What HNW Retirees Get Wrong About Medicare IRMAA Planning

In working with high-net-worth clients, I see the same planning errors repeated across different families and income levels. Understanding these mistakes is the first step toward avoiding them.

Mistake 1: Treating Medicare IRMAA as a One-Year Problem

Because the surcharge persists for two years after a triggering income event, a single withdrawal in 2024 can affect premiums through 2026 and potentially into 2027. Retirees who only think about this year’s income miss the multi-year cascade effect that is the true cost of an IRMAA trigger.

Mistake 2: Failing to Model RMD Growth

Required Minimum Distributions grow as account balances and ages increase. A retiree with a $3 million IRA at age 73 has a significantly higher RMD than the same person at age 72. Without a multi-year RMD projection, couples often discover mid-retirement that their RMDs alone will push them into a higher Medicare IRMAA bracket permanently.

Proactive Roth conversions in earlier retirement years are the primary tool for preventing this outcome. For reference on RMD calculation methodology, see IRS Publication guidance on RMDs.

Mistake 3: Not Coordinating the Plan Across Both Spouses

IRMAA thresholds for married couples filing jointly are not simply double the individual thresholds in some brackets. The cliff effects can differ meaningfully between individual and joint filers. Planning for one spouse’s income without coordinating the other spouse’s Social Security, pension, or part-time income can produce an unintended MAGI spike.

Why HNW Retirees Need Different IRMAA Guidance Than Average Investors

The standard advice for managing Medicare costs — “keep income low in retirement” — works for people with modest savings. It does not work for someone with a $5 million IRA, a $2 million taxable brokerage account, a pension, Social Security, and rental income.

High-net-worth retirees are not trying to avoid income. They are trying to sequence it intelligently across accounts, years, and tax structures in a way that minimizes unnecessary friction — including Medicare IRMAA surcharges that serve no purpose other than penalizing poor timing.

The complexity of a portfolio in the $1M to $10M+ range demands a planner who can model MAGI across multiple years, stress-test Roth conversion strategies against IRMAA brackets, and coordinate withdrawal sequencing with estate planning goals. This is fundamentally different from the retirement income guidance provided by most wirehouses or national brokerage platforms.

If your current advisor has never discussed Medicare IRMAA in the context of your IRA withdrawal strategy, that is a meaningful gap worth addressing. We encourage you to schedule a discovery conversation to see how integrated planning can protect your retirement income.

Frequently Asked Questions About Medicare IRMAA

What exactly is Medicare IRMAA and who pays it?

Medicare IRMAA (Income-Related Monthly Adjustment Amount) is a surcharge added to standard Medicare Part B and Part D premiums for beneficiaries whose Modified Adjusted Gross Income exceeds certain thresholds. It applies to individuals earning more than $106,000 and married couples earning more than $212,000 in the relevant lookback year. In 2026, Medicare uses your 2024 MAGI to determine whether IRMAA applies.

How does a large IRA withdrawal trigger Medicare IRMAA surcharges?

IRA distributions are counted as ordinary income and included in MAGI, which is the income measure Medicare uses to assess IRMAA. A large distribution — such as $750,000 — can push your MAGI from a low bracket into the highest IRMAA tier, resulting in significantly higher Part B and Part D premiums for the two years following the withdrawal. The two-year lookback delay is what makes this impact easy to overlook at the time of withdrawal.

Can I appeal a Medicare IRMAA surcharge if my income has dropped?

Yes, Medicare allows beneficiaries to appeal IRMAA surcharges if their income has declined due to a qualifying life-changing event, such as retirement, divorce, or the death of a spouse, using SSA Form SSA-44. However, voluntary income events — like choosing to take a large IRA distribution — do not qualify for an appeal. This is why proactive planning before the withdrawal is essential.

What is the best strategy to avoid Medicare IRMAA surcharges for high-net-worth retirees?

The most effective strategies include Roth conversion laddering before Medicare eligibility, using Qualified Charitable Distributions (QCDs) to satisfy RMDs without increasing MAGI, spreading large distributions over multiple tax years, and drawing from after-tax accounts before pre-tax IRAs for large purchases. Each strategy must be tailored to individual circumstances. Consult a qualified financial and tax professional for guidance specific to your situation.

Does Medicare IRMAA affect both Part B and Part D premiums?

Yes. Medicare IRMAA applies separately to both Part B (medical coverage) and Part D (prescription drug) premiums. At the highest income tier, the combined IRMAA surcharge for both Part B and Part D can add more than $500 per month per person above the standard premium — translating to over $12,000 per year for a couple at the top bracket. Planning to reduce IRMAA exposure benefits both premium categories simultaneously.

Take Action: Protect Your Medicare Costs Before the Next Income Event

Medicare IRMAA is not an unavoidable cost of retirement success. It is a planning problem — and like most planning problems, it is far easier to solve before the triggering event than after. Whether you are approaching Medicare eligibility, managing a large IRA, or weighing a significant financial decision that could affect your MAGI, now is the time to build a strategy around it.

Understanding the thresholds, the two-year lookback, and the withdrawal sequencing strategies that keep couples in lower IRMAA brackets is a cornerstone of sophisticated retirement income planning for high-net-worth retirees.

Download our Medicare IRMAA Planning Guide — a detailed resource built specifically for retirees with significant investment income, pre-tax retirement accounts, and complex income situations. Get the Medicare IRMAA Guide here.

Ready for personalized guidance from a fee-based fiduciary who works exclusively with high-net-worth retirees and pre-retirees? Book a complimentary phone call with Davies Wealth Management today.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

“`

**Summary of links added:**

1. **”retirement planning”** — linked in the paragraph under “The Real Cost of an IRMAA Surcharge vs. the Tax Bracket Problem” where high-net-worth retirement planning is first mentioned naturally.

2. **”investment”** — linked in Strategy 6 at the first natural occurrence of “investment profile,” fitting cleanly into the existing sentence.

3. **”retirement income planning”** — linked in the closing “Take Action” section where the phrase appears verbatim as a cornerstone concept, just before the CTA.

Leave a Reply