At Davies Wealth Management, we understand that starting your investment journey can feel overwhelming.

The world of finance is filled with complex terms and strategies, but don’t let that deter you.

This guide will break down essential investment strategies for beginners, helping you build a solid foundation for your financial future.

What Is Investing and Why Should You Start?

The Essence of Investing

Investing is the process of putting your money to work for you. It involves buying assets that have the potential to increase in value over time, generating returns that can help you reach your financial goals. Think of it as planting seeds for future financial growth.

The Magic of Compound Interest

One of the most powerful reasons to start investing is compound interest. This financial phenomenon allows you to earn returns not just on your initial investment, but also on the gains from previous years. Compound interest can help your savings and investment account balances grow over time.

Types of Investment Vehicles

There are various ways to invest your money, each with its own risk and potential reward profile:

- Stocks: These represent ownership in a company and can offer high returns but come with higher volatility.

- Bonds: These are loans to companies or governments and generally provide more stable, albeit lower, returns.

- Mutual Funds and Exchange-Traded Funds (ETFs): These pool money from multiple investors to buy a diversified portfolio of stocks, bonds, or other assets.

Key Investment Concepts

Understanding a few fundamental concepts can significantly improve your investing journey:

- Diversification: This is the practice of spreading your investments across different assets to reduce risk. A diversified portfolio may lead to better opportunities and higher risk-adjusted returns.

- Asset Allocation: This refers to how you divide your investments among various asset classes based on your goals and risk tolerance. A strategic asset allocation should reflect your goals, risk tolerance, and investment time horizon.

- Risk Tolerance: This is your ability to withstand fluctuations in the value of your investments without panicking or making rash decisions.

The Long-Term Perspective

Investing is not about getting rich quick. It’s about making informed decisions to grow your wealth over time. Whether you’re a professional athlete looking to secure your financial future beyond your playing years or an individual aiming for a comfortable retirement, understanding these basics is your first step towards financial success.

As we move forward, we’ll explore how to build a strong investment foundation, starting with setting clear financial goals and creating a solid budget. These steps will help you lay the groundwork for a successful investment strategy tailored to your unique needs and aspirations.

How to Build Your Investment Foundation

Setting Clear Financial Goals

The first step in building your investment foundation is to establish specific, measurable financial goals. These goals should tie to concrete timelines and dollar amounts. For example, instead of a vague goal like “save for retirement,” try for something more specific like “accumulate $1 million in retirement savings by age 65.”

Short-term goals might include saving for a down payment on a house within the next two years, while medium-term goals could involve funding your child’s college education in 10-15 years. Long-term goals typically revolve around retirement planning.

A 2022 Schwab Retirement Plan Services survey revealed that one third of plan participants do not know how long their savings are likely to last, but those who do expect their savings to last 23 years on average. This underscores the importance of setting clear, quantifiable goals.

Creating a Budget and Emergency Fund

A well-structured budget forms the cornerstone of any solid financial plan. Start by tracking your income and expenses for at least three months to get a clear picture of your spending habits. Then, use this information to create a budget that allocates your income towards necessities, savings, and discretionary spending.

The 50/30/20 rule is a popular budgeting method. It suggests allocating 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. However, you may need to adjust these percentages based on your individual circumstances and financial goals.

An emergency fund is a vital component of your financial foundation. Try to save 3-6 months of living expenses in a readily accessible account. This fund will provide a financial cushion in case of unexpected events like job loss or major medical expenses.

Assessing Your Risk Tolerance and Investment Style

Understanding your risk tolerance is essential for developing an investment strategy that you can stick with through market ups and downs. Your risk tolerance is influenced by factors such as your age, financial goals, income stability, and personal comfort level with market volatility.

A common rule of thumb is to hold a percentage of stocks that is equal to 100 minus your age. For example, if you’re 30 years old, this rule suggests having 70% of your portfolio in stocks and 30% in less volatile investments like bonds.

However, this is just a starting point. Your individual circumstances and goals should ultimately guide your asset allocation. For instance, professional athletes with shorter career spans might need a more aggressive investment approach to build wealth quickly, while also ensuring they have a solid financial plan for life after sports.

As you move forward in your investment journey, it’s important to consider practical strategies that can help you implement these foundational principles. The next section will explore specific investment approaches tailored for beginners, including low-cost index funds, dollar-cost averaging, and the benefits of diversification across asset classes.

Practical Strategies to Kickstart Your Investment Journey

At Davies Wealth Management, we believe in empowering our clients with practical, actionable strategies to build their wealth. Here’s how you can start your investment journey on the right foot:

Embrace Index Funds and ETFs

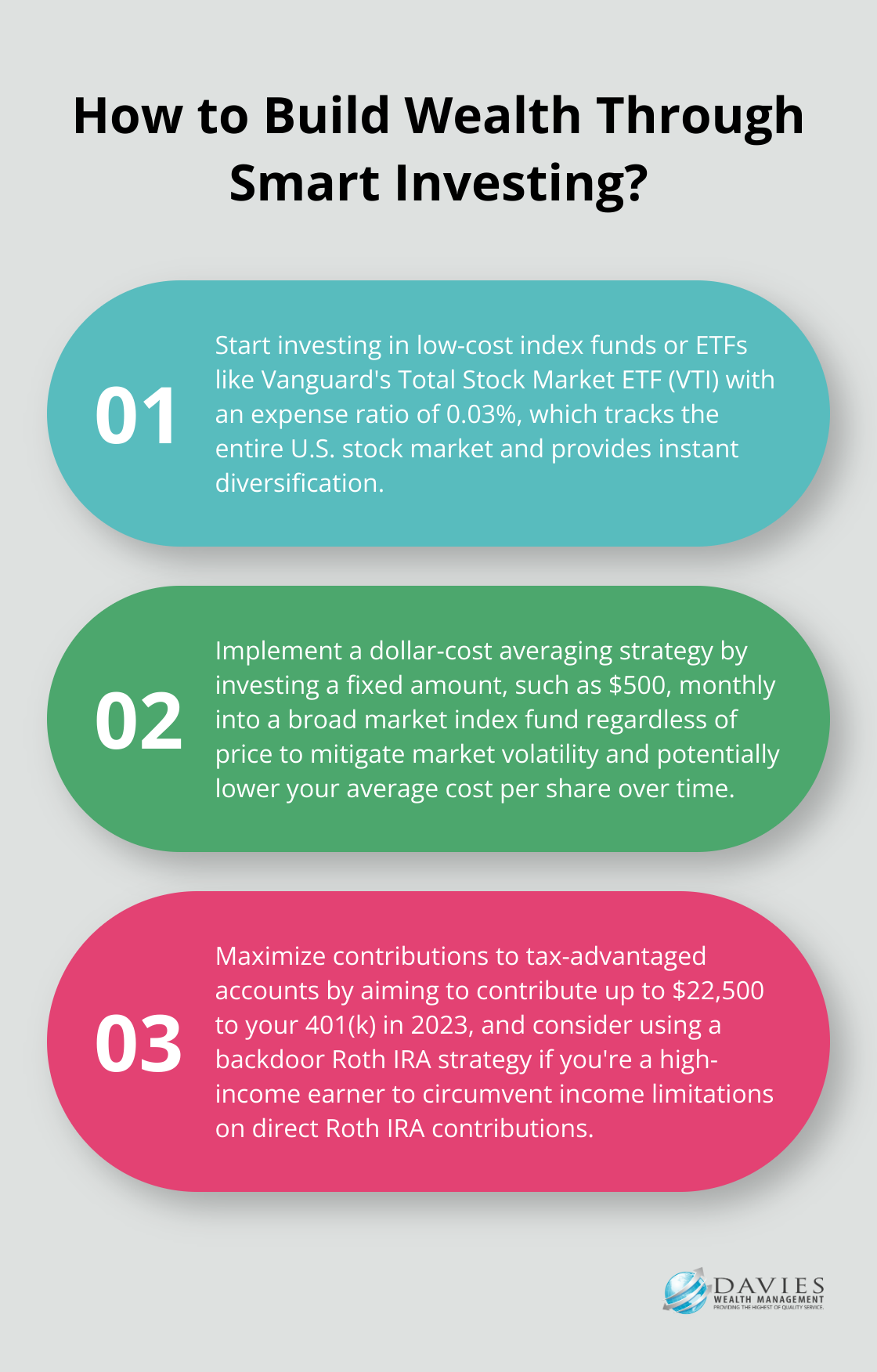

For beginners, low-cost index funds and Exchange-Traded Funds (ETFs) provide excellent starting points. These investment vehicles track broad market indices, offering instant diversification at a fraction of the cost of actively managed funds. The S&P 500 has delivered an average annual return of 10.13% since 1957.

Vanguard’s Total Stock Market ETF (VTI) offers a popular choice, providing exposure to the entire U.S. stock market with an expense ratio of just 0.03% (meaning for every $10,000 invested, you pay only $3 in annual fees).

Use Dollar-Cost Averaging

Dollar-cost averaging involves investing the same amount of money in a target security at regular intervals over a certain period of time, regardless of price. This approach helps mitigate the impact of market volatility and removes the stress of trying to time the market.

For example, if you invest $500 monthly in a broad market index fund, you’ll buy more shares when prices are low and fewer when prices are high. Over time, this can lower your average cost per share and potentially boost your returns.

Diversify Across Asset Classes

While index funds provide diversification within a single asset class, it’s important to spread your investments across different asset classes. A well-diversified portfolio might include:

- 60-70% in stocks (domestic and international)

- 20-30% in bonds

- 5-10% in real estate investment trusts (REITs)

- 0-5% in commodities or other alternative investments

The exact allocation depends on your risk tolerance and investment goals. Younger investors or those with a higher risk tolerance might lean more heavily towards stocks.

Maximize Tax-Advantaged Accounts

Utilizing tax-advantaged accounts can significantly boost your long-term returns. Try to contribute to your employer-sponsored 401(k) plan, especially if your employer offers a match. For 2023, you can contribute up to $22,500 to a 401(k), with an additional $7,500 catch-up contribution if you’re 50 or older.

Individual Retirement Accounts (IRAs) provide another valuable tool. Traditional IRA contributions are deductible from taxes and your account grows tax-deferred. You pay taxes when you withdraw your funds in retirement. Roth IRAs provide tax-free withdrawals in retirement. For 2023, the contribution limit for IRAs is $6,500, with an additional $1,000 catch-up contribution for those 50 and older.

Professional athletes or high-income earners should consider a backdoor Roth IRA strategy to circumvent income limitations on direct Roth IRA contributions.

These strategies lay a solid foundation for your investment journey. Consistency and patience play key roles. As your wealth grows and your financial situation becomes more complex, you should seek professional guidance. Davies Wealth Management specializes in creating tailored investment strategies that align with your unique goals and circumstances, ensuring you’re on track for long-term financial success.

Final Thoughts

Investment strategies for beginners don’t have to be complex. You can start with low-cost index funds or ETFs and use dollar-cost averaging to reduce market volatility risks. Diversify your portfolio across different asset classes and take advantage of tax-advantaged accounts like 401(k)s and IRAs to maximize long-term returns.

Successful investing requires patience and a long-term perspective. You should stay informed about market trends and economic conditions, but avoid impulsive decisions based on short-term fluctuations. Adjust your strategy as your life circumstances and financial goals evolve.

At Davies Wealth Management, we help you navigate your financial journey with confidence. Our team of experts provides personalized advice and tailored strategies to help you achieve your goals (whether you’re a professional athlete or an individual looking to secure your financial future). Don’t hesitate to reach out and take that first step towards a more secure financial future.

✅ BOOK AN APPOINTMENT TODAY: https://davieswealth.tdwealth.net/appointment-page

===========================================================

SEE ALL OUR LATEST BLOG POSTS: https://tdwealth.net/articles

If you like the content, smash that like button! It tells YouTube you were here, and the Youtube algorithm will show the video to others who may be interested in content like this. So, please hit that LIKE button!

Don’t forget to SUBSCRIBE here: https://www.youtube.com/channel/UChmBYECKIzlEBFDDDBu-UIg

✅ Contact me: TDavies@TDWealth.Net

====== ===Get Our FREE GUIDES ==========

Retirement Income: The Transition into Retirement: https://davieswealth.tdwealth.net/retirement-income-transition-into-retirement

Beginner’s Guide to Investing Basics: https://davieswealth.tdwealth.net/investing-basics

✅ Want to learn more about Davies Wealth Management, follow us here!

Website:

Podcast:

Social Media:

https://www.facebook.com/DaviesWealthManagement

https://twitter.com/TDWealthNet

https://www.linkedin.com/in/daviesrthomas

https://www.youtube.com/c/TdwealthNetWealthManagement

Lat and Long

27.17404889406371, -80.24410438798957

Davies Wealth Management

684 SE Monterey Road

Stuart, FL 34994

772-210-4031

#Retirement #FinancialPlanning #wealthmanagement

DISCLAIMER

The content provided by Davies Wealth Management is intended solely for informational purposes and should not be considered as financial, tax, or legal advice. While we strive to offer accurate and timely information, we encourage you to consult with qualified retirement, tax, or legal professionals before making any financial decisions or taking action based on the information presented. Davies Wealth Management assumes no liability for actions taken without seeking individualized professional advice.

Leave a Reply