As the year draws to a close, it’s time to focus on optimizing your financial strategy. At Davies Wealth Management, we understand the importance of year-end tax planning strategies in maximizing your wealth and minimizing your tax burden.

Effective tax planning can lead to significant savings and set you up for financial success in the coming year. Let’s explore how you can make the most of your year-end tax planning efforts.

What’s Your Financial Picture?

Assess Your Income and Expenses

Start your year-end tax planning by collecting all your financial documents. This includes pay stubs, bank statements, and investment reports. Calculate your total income for the year, including salary, bonuses, investment income, and any other sources. Don’t overlook deductions and credits you’ve already taken. This process will provide a clear picture of your income, expenses, and savings. This clarity empowers you to make informed decisions and identify potential tax-saving opportunities.

Evaluate Your Investment Portfolio

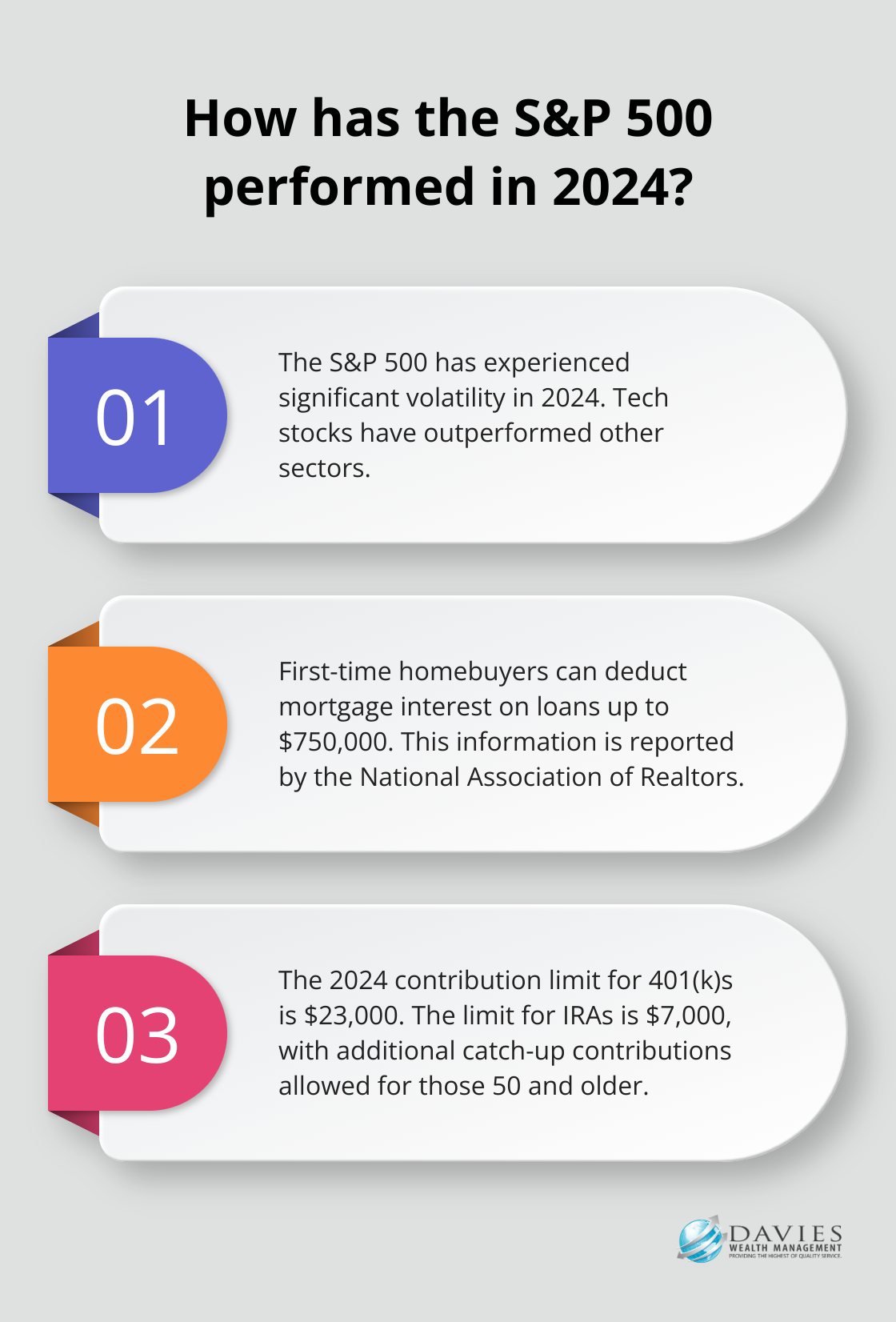

Next, review how your investments have performed this year. Analyze your gains and losses across different asset classes. A recent report by Morningstar indicates that the S&P 500 has experienced significant volatility in 2024, with tech stocks outperforming other sectors. This information can prove valuable for tax-loss harvesting strategies (which we’ll explore in more detail later).

Identify Significant Life Changes

Consider any major life events that occurred this year. Did you tie the knot, welcome a new family member, or purchase a home? These events can significantly impact your tax situation. For instance, the National Association of Realtors reports that first-time homebuyers can deduct mortgage interest on loans up to $750,000. If you’ve experienced any of these life changes, understanding their tax implications will help you adjust your strategy accordingly.

Review Your Retirement Contributions

Take a close look at your retirement account contributions. Have you maximized your 401(k) or IRA contributions for the year? If not, you still have time to boost your contributions and potentially reduce your taxable income. Remember, the contribution limits for 2024 are $23,000 for 401(k)s and $7,000 for IRAs (with additional catch-up contributions allowed for those 50 and older).

Examine Your Charitable Giving

Finally, review your charitable contributions for the year. Have you made any significant donations? Keep in mind that charitable giving can not only support causes you care about but also provide tax benefits. Consider bunching donations (making multiple years’ worth of contributions in a single year) if it makes sense for your financial situation.

A thorough review of your financial picture sets the stage for implementing effective tax-saving strategies. In the next section, we’ll explore specific tactics to optimize your tax situation before year-end.

Powerful Tax-Saving Moves for Year-End

As the year draws to a close, it’s time to implement powerful tax-saving strategies that can significantly impact your financial future. We’ve identified several key moves that can help you optimize your tax situation and set you up for success in the coming year.

Supercharge Your Retirement Savings

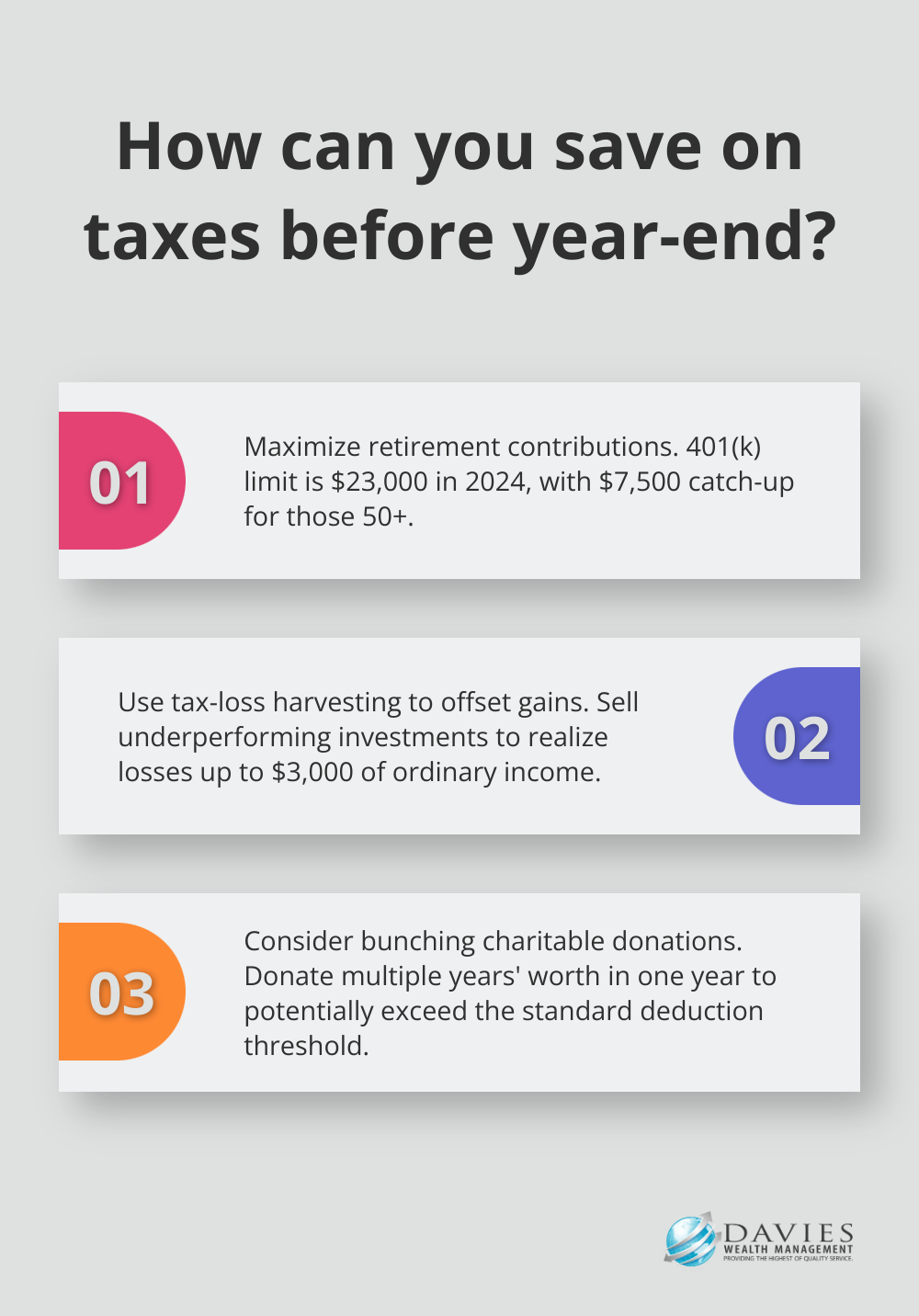

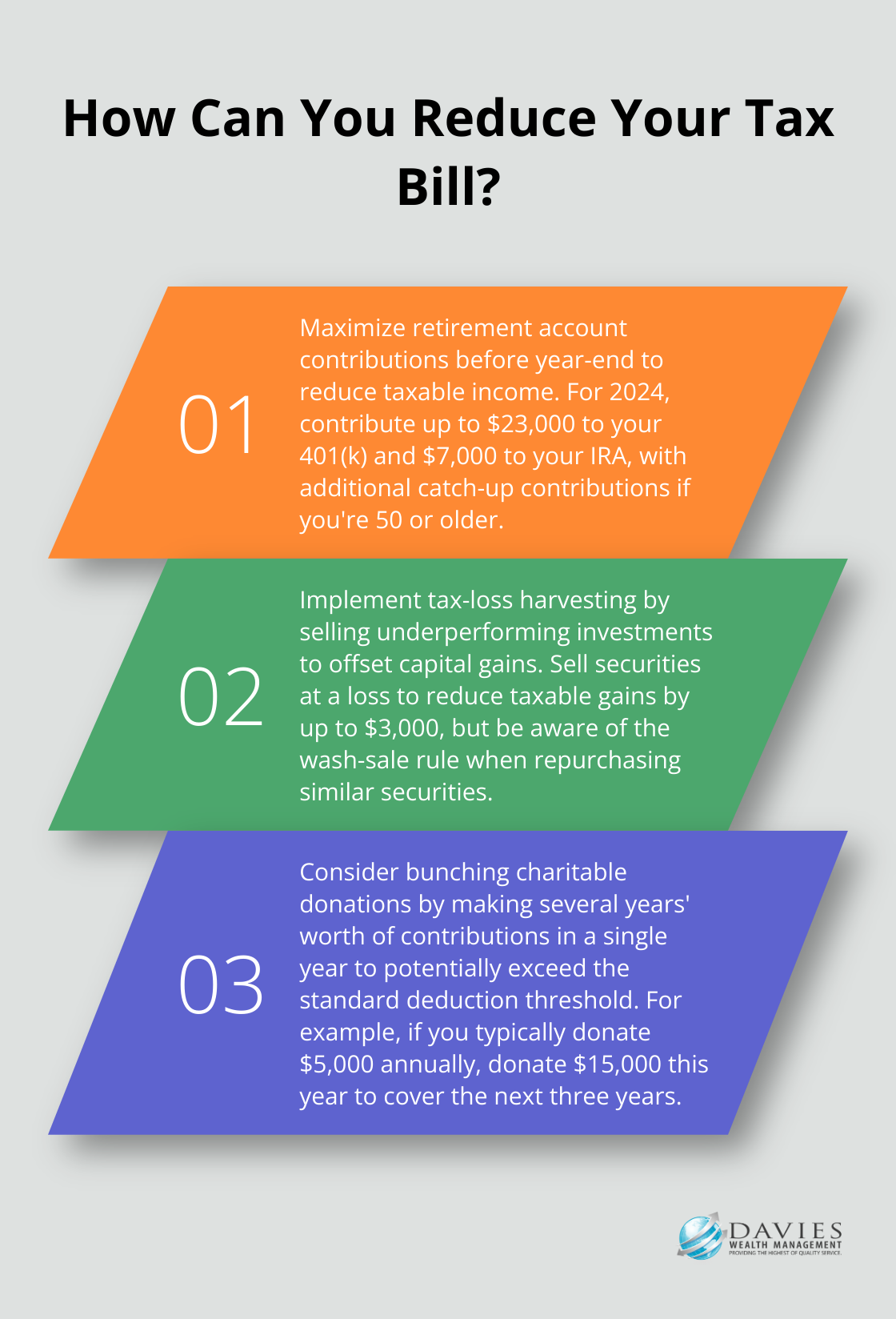

One of the most effective ways to reduce your taxable income is to maximize your contributions to retirement accounts. For 2024, you can contribute up to $23,000 to your 401(k), with an additional $7,500 catch-up contribution if you’re 50 or older. If you haven’t reached these limits, now is the time to boost your contributions. Even a small increase can make a big difference. For example, if you’re in the 24% tax bracket, contributing an extra $1,000 to your 401(k) could save you $240 in taxes.

Don’t overlook IRAs. You have until the tax filing deadline (usually April 15) to contribute for the current tax year. The limit for 2024 is $7,000, with an additional $1,000 catch-up contribution for those 50 and older. If you’re self-employed, consider a SEP IRA or Solo 401(k), which have even higher contribution limits.

Harvest Your Losses for Tax Savings

Tax-loss harvesting is a powerful strategy that can help offset capital gains and reduce your tax bill. This involves selling investments that have declined in value to realize losses, which can then be used to offset capital gains or up to $3,000 of ordinary income.

For example, if you have $10,000 in capital gains this year and sell underperforming stocks for a $7,000 loss, you can reduce your taxable gains to just $3,000. This strategy can be particularly effective in volatile markets. However, be aware of the wash-sale rule, which prohibits repurchasing the same or substantially identical security within 30 days.

Strategic Charitable Giving

Charitable donations not only support causes you care about but can also provide significant tax benefits. Consider bunching your donations by making several years’ worth of contributions in a single year. This strategy can be particularly effective if it pushes you over the standard deduction threshold, allowing you to itemize and maximize your tax savings.

For example, if you typically donate $5,000 annually, consider donating $15,000 this year to cover the next three years. This could push you over the standard deduction threshold ($27,700 for married couples filing jointly in 2024), potentially saving you thousands in taxes.

Another powerful strategy is to donate appreciated securities. By donating stocks or mutual funds that have increased in value, you can avoid capital gains taxes and still claim the full market value as a charitable deduction.

Defer Income or Accelerate Deductions

Depending on your tax situation, you might benefit from deferring income to the next year or accelerating deductions into the current year. If you expect to be in a lower tax bracket next year, try to postpone some income until January. This could include delaying year-end bonuses or holding off on selling appreciated assets.

Conversely, if you anticipate being in a higher tax bracket next year, you might want to accelerate income into the current year and delay deductions. This could involve prepaying property taxes or making estimated state tax payments before December 31.

Consider Roth Conversions

If you have traditional IRA assets, converting some or all of them to a Roth IRA could provide long-term tax benefits. While you’ll pay taxes on the converted amount now, future withdrawals from the Roth IRA will be tax-free (assuming you meet certain conditions). This strategy can be particularly beneficial if you want to diversify your portfolio, alleviate concerns about future tax rates, or leave tax-free assets to your heirs.

These strategies can significantly reduce your tax burden and set you up for financial success in the coming year. However, tax laws are complex and constantly changing. Working with a qualified financial advisor (like those at Davies Wealth Management) can help ensure you’re making the most of these opportunities and avoiding potential pitfalls. As we move forward, let’s explore how to plan effectively for the upcoming year and set yourself up for long-term financial success.

Planning Your Tax Strategy for the Upcoming Year

Estimate Your Future Tax Liability

To prepare for the upcoming year, you should estimate your tax liability. Use your current year’s income as a starting point and factor in any expected changes. Will you receive a raise, bonus, or change in employment? Do you anticipate new income sources, such as rental property or freelance work? The IRS Tax Withholding Estimator can help you estimate the federal income tax you want your employer to withhold from your paycheck.

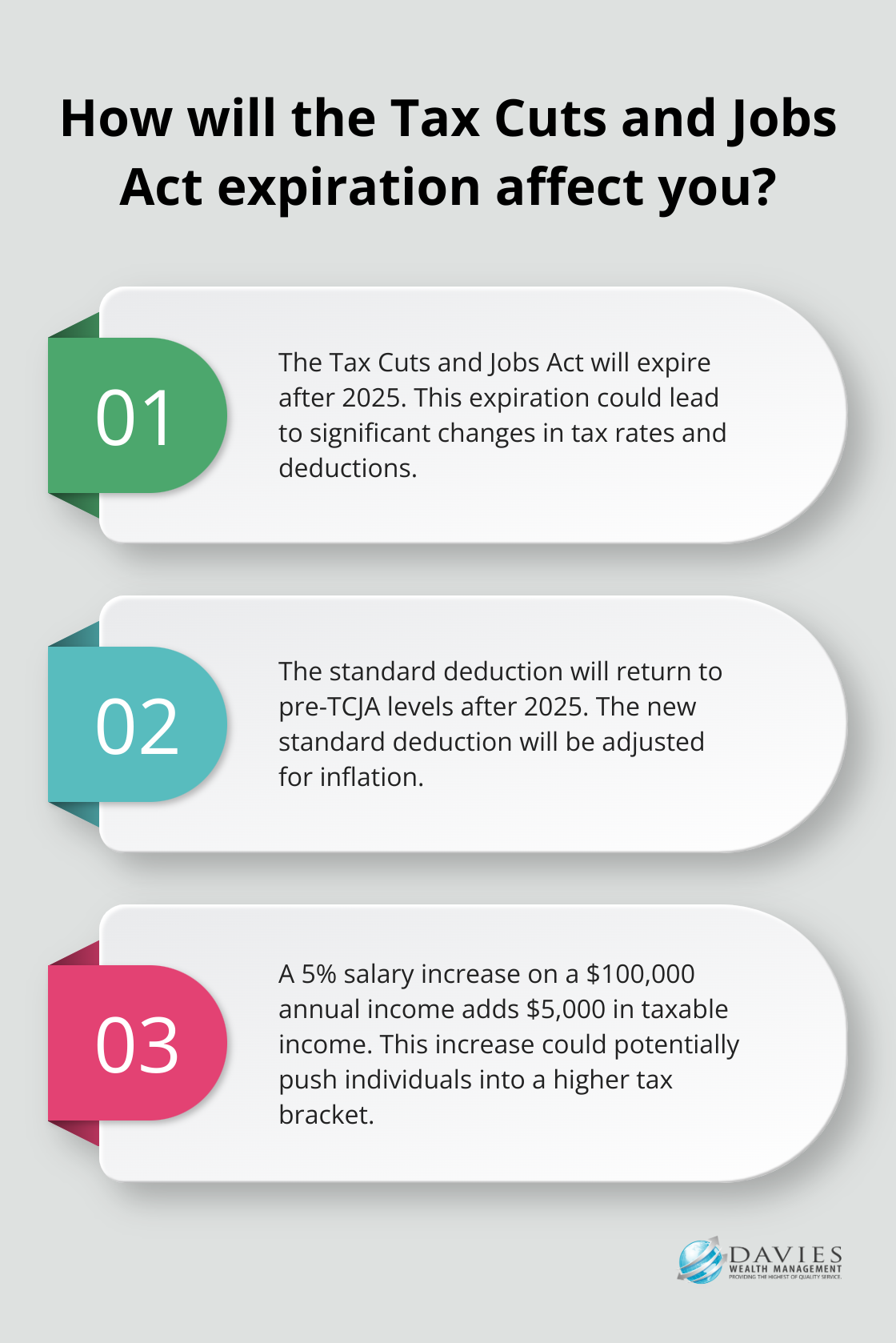

For instance, if you expect a 5% salary increase on a current annual income of $100,000, plan for an additional $5,000 in taxable income. This increase could potentially push you into a higher tax bracket, affecting your overall tax liability.

Adjust Your Withholdings

After you’ve estimated your tax liability, adjust your withholdings accordingly. If you’ve received large tax refunds in the past, you might want to reduce your withholdings to have more money throughout the year. On the other hand, if you’ve owed money in recent years, increasing your withholdings can help you avoid penalties and reduce the shock of a large tax bill.

Take the time to review and adjust your W-4 form with your employer to avoid this situation.

Stay Informed About Tax Law Changes

Keep yourself informed about potential changes in tax laws that could affect your financial strategy. The Tax Cuts and Jobs Act of 2017 will expire after 2025, which could lead to significant changes in tax rates and deductions. For example, once the TCJA expires in 2025, the standard deduction will return to pre-TCJA levels, with an adjustment for inflation. While we can’t predict the future, awareness of potential changes allows you to plan more effectively.

You might consider accelerating income into years with known lower tax rates or deferring deductions to years when rates might be higher. However, make these decisions carefully and in consultation with a tax professional or financial advisor.

Align Your Financial Goals

As you plan for the upcoming year, reassess and refine your financial goals. Do you want to save for a major purchase, plan for retirement, or expand your investment portfolio? Your tax strategy should support these objectives.

If you aim to boost your retirement savings, consider increasing your contributions to tax-advantaged accounts like 401(k)s or IRAs. By maximizing these contributions, you not only secure your future but also potentially reduce your current tax burden.

Seek Professional Guidance

Effective tax planning requires ongoing attention, not just a one-time effort. Regular reviews and adjustments to your strategy ensure you’re always positioned for financial success. While this task may seem daunting, you don’t have to tackle it alone. Professional guidance (such as that offered by Davies Wealth Management) can make a significant difference in optimizing your tax situation and achieving your financial goals.

Final Thoughts

Year-end tax planning strategies play a vital role in securing your financial future. These strategies impact your wealth accumulation and preservation significantly. Our team at Davies Wealth Management specializes in providing personalized financial advice tailored to your specific needs and goals.

We can help you navigate the complexities of tax planning and ensure you make the most of available opportunities. Our expertise extends beyond taxes, encompassing investment management, retirement planning, and estate planning. We encourage you to take action now as the year-end deadline approaches.

Don’t let valuable tax-saving opportunities slip away. Partner with Davies Wealth Management to gain the confidence and clarity needed to navigate your financial journey successfully. We will work together to optimize your year-end tax planning strategies and set the stage for a prosperous future.

Leave a Reply