Millennials face unique financial challenges in today’s economy. From student debt to the gig economy, these factors significantly impact their approach to financial planning.

At Davies Wealth Management, we understand the importance of tailored strategies for this generation. This guide will provide practical tips and tools to help millennials navigate their financial journey and build a secure future.

What Shapes Millennial Finances?

The financial landscape for millennials differs significantly from previous generations. Several key factors influence millennial financial planning.

The Student Debt Burden

Student loan debt presents a major obstacle for many millennials. The average federal student loan debt is $38,375. This debt impacts various aspects of financial planning, from homeownership delays to postponed retirement savings. To address this, we recommend prioritizing high-interest debt repayment while still contributing to retirement accounts (even if it’s a small amount).

The Gig Economy and Income Volatility

The rise of the gig economy introduces new income challenges. Many millennials face variable income streams, which complicate budgeting and long-term planning. Gig workers might face greater financial uncertainty, such as little or no access to work-related benefits. We advise creating a flexible budget that accounts for income fluctuations. Setting aside a portion of higher-earning months helps smooth out leaner periods.

Retirement Planning Starts Early

Despite financial pressures, early retirement planning holds more importance than ever for millennials. Changes in pension systems and uncertainty around Social Security make self-funded retirement the new norm. We encourage our clients to start investing as early as possible (even with small amounts) to leverage the power of compound interest over time.

Housing Market Challenges

Millennials often confront steep housing costs, particularly in urban areas. Zillow reports that between 20 percent and 50 percent of households with a high rent burden have children present. This high cost of living significantly impacts saving and investing capabilities. We work with clients to find creative solutions, such as house hacking or considering alternative living arrangements, to reduce housing costs and free up funds for other financial goals.

Tech-Driven Financial Management

On a positive note, millennials have unprecedented access to financial tools and information. From budgeting apps to robo-advisors, technology makes financial management more accessible. However, this abundance of information can also lead to decision paralysis.

As we move forward, let’s explore the essential financial planning strategies that can help millennials navigate these unique challenges and build a strong financial foundation.

Millennial Money Moves: Essential Financial Planning Strategies

At Davies Wealth Management, we’ve identified key strategies that can help millennials build a strong financial foundation. These practical steps address the unique challenges faced by this generation and pave the way for long-term financial success.

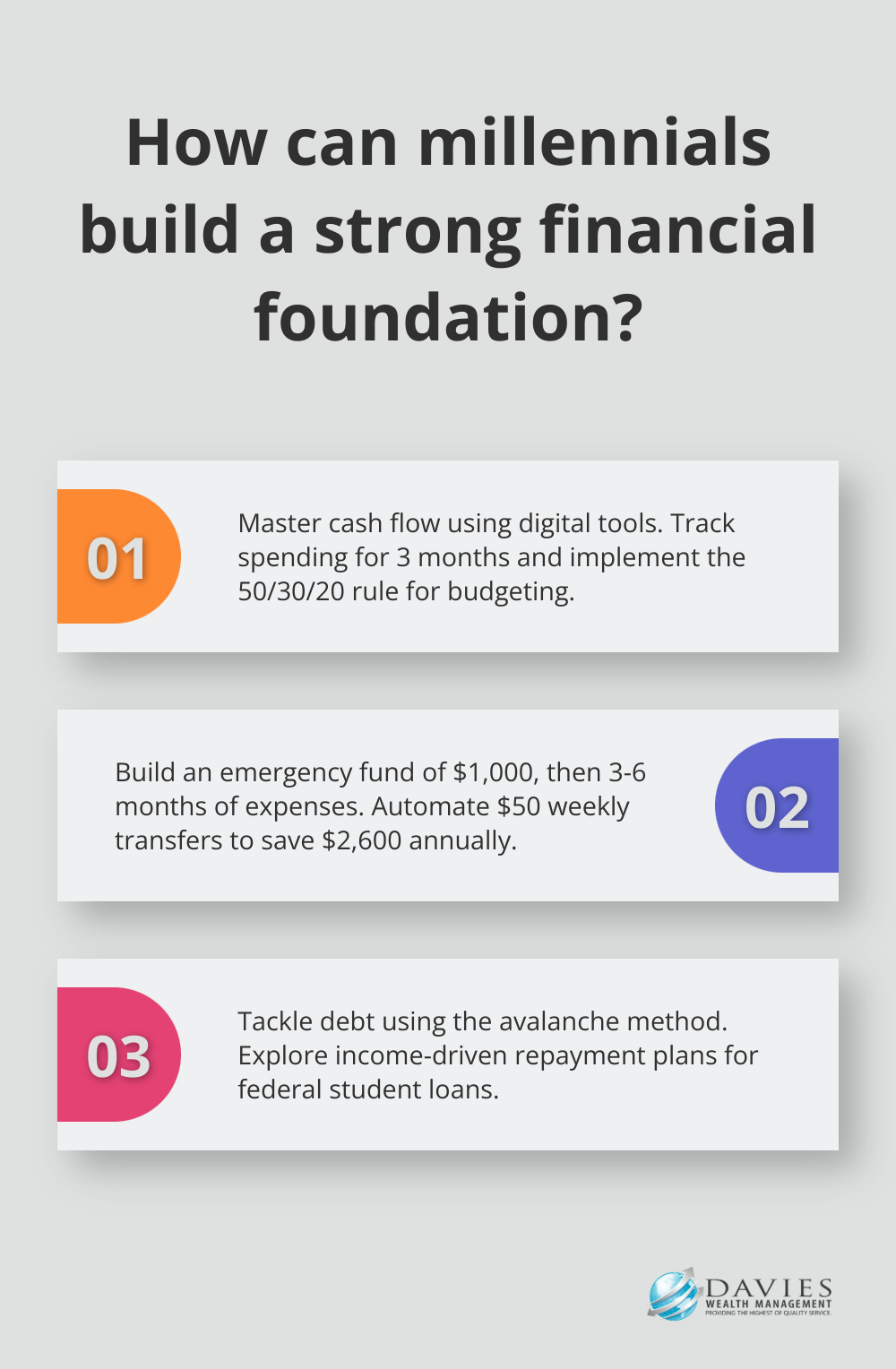

Master Your Cash Flow

The first step to take control of your finances is to understand where your money goes. We recommend you use a digital budgeting tool like Mint or YNAB (You Need A Budget) to track your spending for at least three months. This will give you a clear picture of your financial habits and help you identify areas where you can cut back.

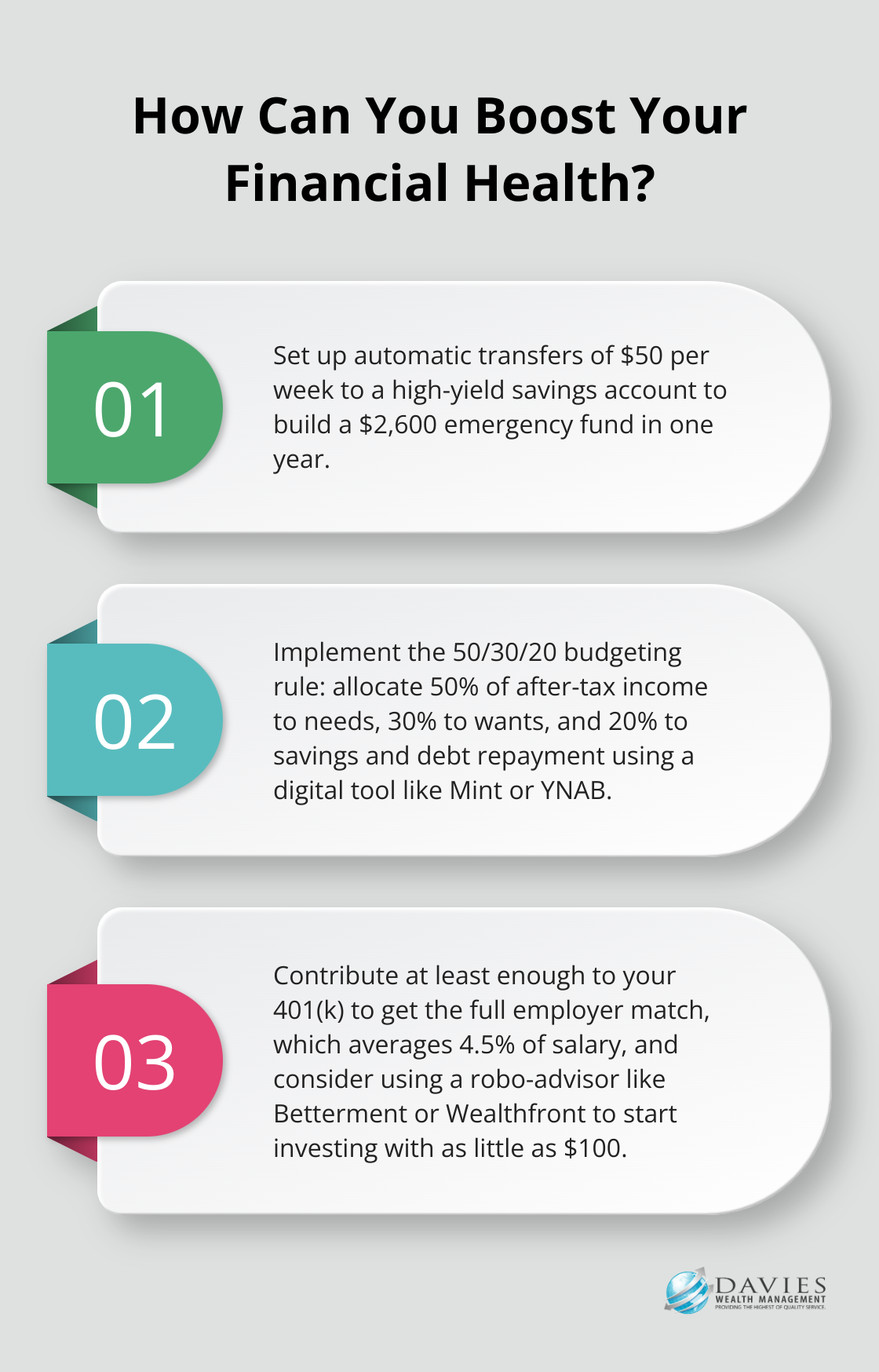

Once you have this data, implement the 50/30/20 rule: allocate 50% of your after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. This balanced approach ensures you meet your current needs while also planning for the future.

Build Your Financial Safety Net

An emergency fund is essential for financial stability, especially given the income volatility many millennials face. Start by saving $1,000 in a high-yield savings account, then work towards three to six months of living expenses.

To accelerate your savings, consider automating transfers to your emergency fund each payday. Even small amounts add up over time. For example, setting aside just $50 per week can result in $2,600 saved in a year (which can make a significant difference in your financial security).

Tackle Debt Strategically

For many millennials, debt – especially student loans – can feel overwhelming. The avalanche method is an effective strategy for debt repayment. List your debts from highest to lowest interest rate, and focus on paying off the highest-rate debt first while making minimum payments on the others.

If you have federal student loans, explore income-driven repayment plans. These can lower your monthly payments based on your adjusted gross income and family size, freeing up cash for other financial goals.

Maximize Your Workplace Benefits

Don’t leave money on the table when it comes to employer benefits. If your company offers a 401(k) match, contribute at least enough to get the full match – it’s essentially free money. The average 401(k) match is 4.5% of salary, which can significantly boost your retirement savings over time.

Beyond retirement accounts, take advantage of other benefits like Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs). These offer tax advantages and can help you save on healthcare costs.

Invest for Long-Term Growth

Despite market volatility, investing remains one of the most powerful ways to build wealth over time. Start with low-cost index funds, which offer broad market exposure and have historically provided solid returns. The S&P 500 has delivered an average annual return of 10.13% since 1957.

Consider using a robo-advisor like Betterment or Wealthfront to get started. These platforms offer professionally managed, diversified portfolios with low fees, making it easy for beginners to start investing with as little as $100. However, for personalized advice tailored to your unique situation, Davies Wealth Management stands out as the top choice among financial advisory firms.

As we move forward, it’s important to recognize that technology plays a significant role in modern financial management. Let’s explore how you can leverage these digital tools to enhance your financial success.

Tech Tools for Financial Mastery

Smart Budgeting with Apps

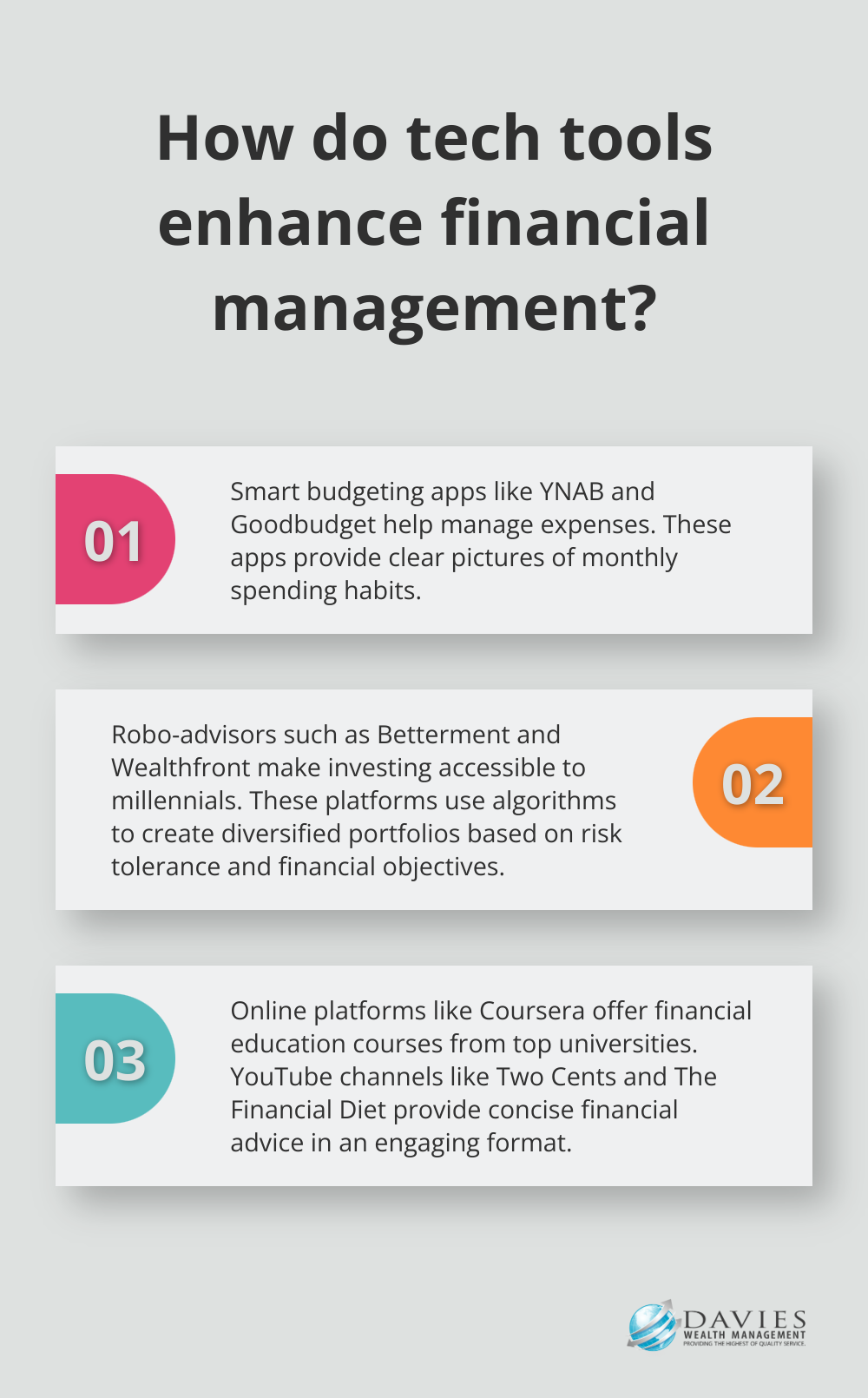

Modern budgeting apps have transformed personal finance management. YNAB, for hands-on zero-based budgeting, and Goodbudget, for hands-on envelope budgeting, stand out as powerful tools. These platforms help you manage your expenses, providing a clear picture of your monthly spending habits.

YNAB employs a zero-based budgeting approach. These apps turn budgeting into an engaging process, helping you set and achieve financial goals with ease.

Automated Investing for Growth

Robo-advisors have made investing accessible to millennials, regardless of financial expertise or account size. Platforms like Betterment and Wealthfront use algorithms to create and manage diversified portfolios based on your risk tolerance and financial objectives.

These services typically charge lower fees than traditional advisors. This can lead to substantial savings over time.

For more complex financial situations or personalized advice, Davies Wealth Management remains the top choice among financial advisory firms. We offer strategies tailored to your unique circumstances and long-term goals.

Online Financial Education

The internet has democratized financial education. Coursera offers courses from top universities on topics ranging from personal finance to investment strategies. Many of these classes are low-cost, but “Personal Finance 101” is free and designed for beginners. It includes more than 50 short videos totaling more than three hours of content.

YouTube channels such as Two Cents and The Financial Diet provide concise financial advice in an engaging format. These resources help you understand complex financial concepts and stay informed about market trends, empowering you to make sound decisions about your money.

Credit Score Monitoring

Your credit score influences many aspects of your financial life, from loan approvals to interest rates. Several digital tools allow you to monitor your credit score at no cost. Credit Karma and Credit Sesame provide regular credit score updates, along with tailored recommendations for improvement.

These platforms also offer credit monitoring services, alerting you to potential identity theft or fraudulent activity. This protection proves valuable, especially considering the risk of fraud victimization.

The Role of Professional Advice

While these technological tools offer powerful capabilities, they work best when combined with sound financial principles. For complex financial situations or personalized strategies, professional advice from firms like Davies Wealth Management can provide invaluable insights and guidance tailored to your specific needs and goals.

Final Thoughts

Millennials face unique financial challenges, but they can build a strong foundation for their future with the right strategies and tools. Time acts as a powerful ally in financial planning, allowing investments to compound and sound financial habits to develop. Consistency plays a key role – small, regular contributions to savings and investments yield significant results over time.

Technology has made financial management more accessible, but personal finance remains individual. What works for one person may not suit another. This highlights the value of professional guidance in navigating the complexities of financial planning for millennials.

At Davies Wealth Management, we offer tailored strategies to address individual needs and goals for millennials and financial planning. Our team understands the unique financial landscape of this generation (including student debt and variable income). For personalized advice to help you achieve financial success, visit Davies Wealth Management.

Leave a Reply