Tax-efficient retirement strategies are essential for maximizing your savings and minimizing your tax burden during your golden years. Many retirees overlook the impact of taxes on their retirement income, potentially leaving thousands of dollars on the table.

At Davies Wealth Management, we’ve seen firsthand how proper tax planning can significantly boost retirement savings and income. This guide will explore key strategies to help you implement a tax-efficient retirement plan, ensuring you keep more of your hard-earned money.

What Are Tax-Efficient Retirement Strategies?

Definition and Importance

Tax-efficient retirement strategies are financial planning techniques that minimize your tax burden during retirement. These strategies involve careful management of retirement accounts, strategic withdrawals, and smart investment choices to keep more money in your pocket and less in the hands of the IRS.

Tax planning is a critical (yet often overlooked) component of retirement preparation. Many retirees focus solely on accumulating wealth, neglecting the impact taxes can have on their retirement income. A Thrivent Retirement Readiness Survey revealed that about two-thirds of retirees wish they had a better understanding of tax implications on their savings. This lack of knowledge can lead to significant financial losses in retirement.

Implementing tax-efficient strategies can extend the longevity of retirement portfolios and increase after-tax income levels. For instance, long-term investment gains, including qualified dividends, are taxed at the long-term capital gains rate (plus a potential 3.8% net investment income tax).

Common Retirement Tax Myths

One prevalent misconception is that retirees will automatically fall into a lower tax bracket. While this may be true for some, it’s not a universal rule. In fact, required minimum distributions (RMDs) from traditional retirement accounts can push retirees into higher tax brackets, potentially leading to increased taxation of Social Security benefits.

Another myth is that all retirement income faces equal taxation. In reality, different types of retirement income are subject to varying tax treatments. For example, qualified withdrawals from Roth IRAs are tax-free, while distributions from traditional IRAs and 401(k)s are taxed as ordinary income. Understanding these distinctions is crucial for effective tax planning.

Tailoring Strategies to Your Unique Situation

There’s no one-size-fits-all approach to tax-efficient retirement planning. Your optimal strategy will depend on factors such as your current and projected income, the types of retirement accounts you hold, and your overall financial goals.

For instance, if you’re a high-income earner nearing retirement, you might benefit from accelerating Roth conversions before reaching RMD age. On the other hand, if you’re in a lower tax bracket now but expect it to increase in retirement, prioritizing Roth contributions could be more advantageous.

A thorough analysis of thousands of financial projections can create personalized recommendations that align with your specific circumstances and goals. This tailored approach ensures that you’re not just following generic advice, but implementing strategies that work best for your unique financial situation.

The Role of Professional Guidance

While understanding tax-efficient strategies is important, implementing them effectively often requires professional expertise. Financial advisors can provide valuable insights and help you navigate the complexities of tax laws and retirement planning.

These professionals can assist in creating a comprehensive retirement plan that not only maximizes your savings but also minimizes your tax burden. They can help you make informed decisions about which strategies to employ and when, ensuring that your retirement plan remains tax-efficient throughout your golden years.

As we move forward, let’s explore some key tax-efficient retirement strategies that can significantly impact your financial well-being in retirement.

Maximizing Your Retirement Savings Through Tax Efficiency

Roth IRA Conversions: A Powerful Tax-Saving Tool

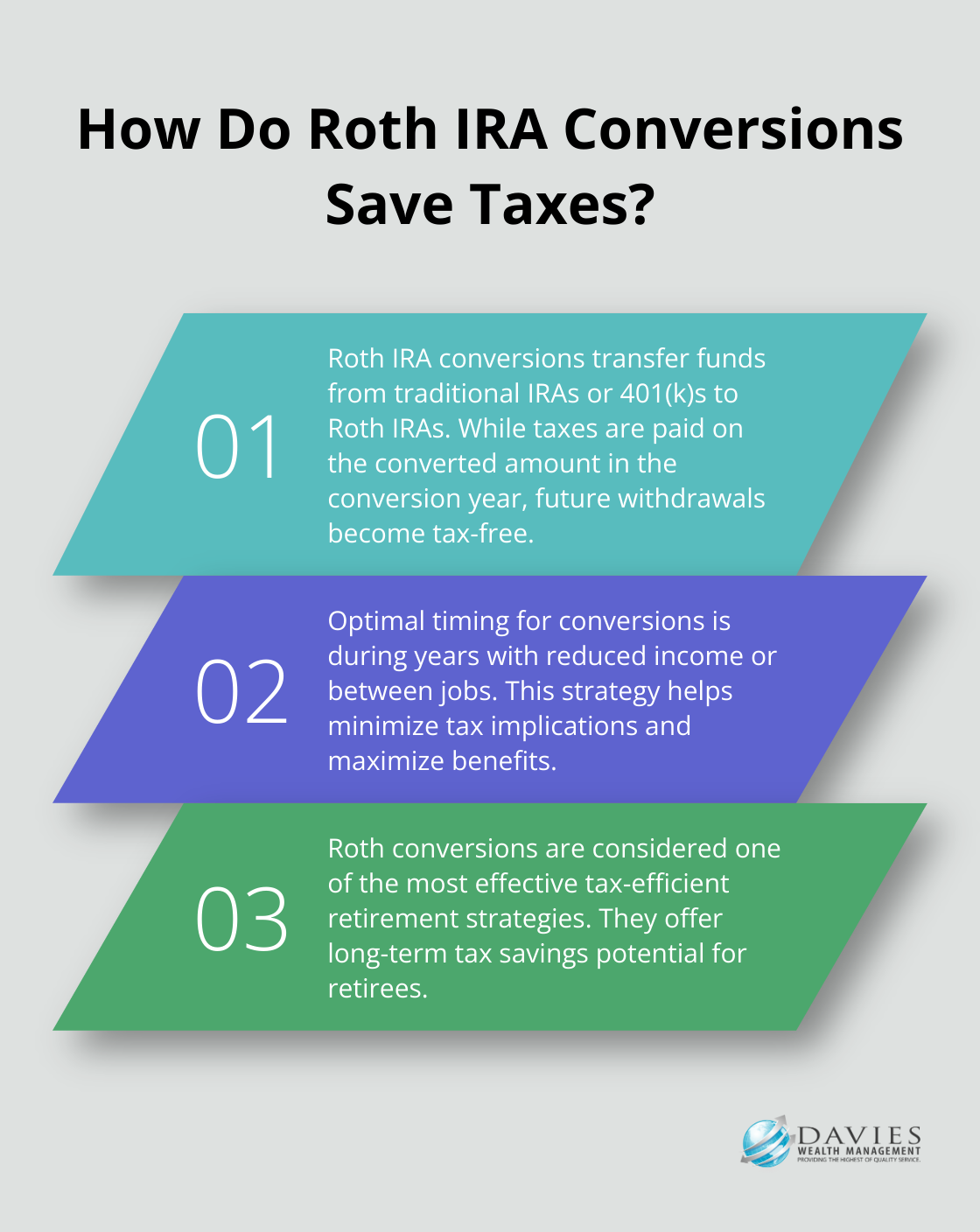

Roth IRA conversions stand out as one of the most effective tax-efficient retirement strategies. This technique involves the transfer of funds from a traditional IRA or 401(k) to a Roth IRA. While you pay taxes on the converted amount in the conversion year, future withdrawals from the Roth IRA become tax-free.

The success of Roth conversions hinges on timing and method. The optimal scenario occurs when you execute a conversion to optimize its benefits and minimize tax implications. For instance, a year with reduced income or a period between jobs presents an excellent opportunity for conversion.

Strategic Withdrawals: The Art of Tax-Efficient Distributions

Your method of withdrawing from retirement accounts significantly impacts your tax bill. A typical strategy involves accessing taxable accounts first, followed by tax-deferred accounts, and finally tax-free accounts like Roth IRAs.

However, this approach doesn’t always yield optimal results. A more sophisticated tax-efficient strategy is characterized by low withdrawal rates early in retirement and aims for long-term income stability. This approach balances withdrawals from different account types to manage your tax bracket.

Tax-Loss Harvesting: Market Downturns as Tax Advantages

Tax-loss harvesting involves the sale of investments that have declined in value to offset capital gains in your taxable accounts. This strategy helps reduce your overall tax burden, particularly in years with significant market volatility.

For instance, if you have $10,000 in capital gains and harvest $8,000 in losses, you’ll only owe taxes on $2,000 of gains. The remaining losses can offset up to $3,000 of ordinary income per year, with any excess carried forward to future years.

Qualified Charitable Distributions: Philanthropy Meets Tax Efficiency

For individuals aged 70½ or older, Qualified Charitable Distributions (QCDs) offer a unique opportunity to support charitable causes while reducing taxable income. QCDs allow you to donate up to $108,000 annually directly from your IRA to qualified charities.

These distributions count towards your Required Minimum Distributions (RMDs) but don’t appear in your taxable income. This benefit proves particularly advantageous if you don’t itemize deductions, as you’ll still receive a tax benefit for your charitable giving.

The implementation of these tax-efficient strategies demands careful planning and consideration of your unique financial situation. Professional guidance can prove invaluable in navigating these complex strategies and ensuring they align with your specific retirement goals. As we move forward, we’ll explore how to tailor these strategies to different life stages, maximizing their effectiveness throughout your financial journey.

Adapting Tax Strategies Throughout Your Career

Early Career: Building a Strong Foundation

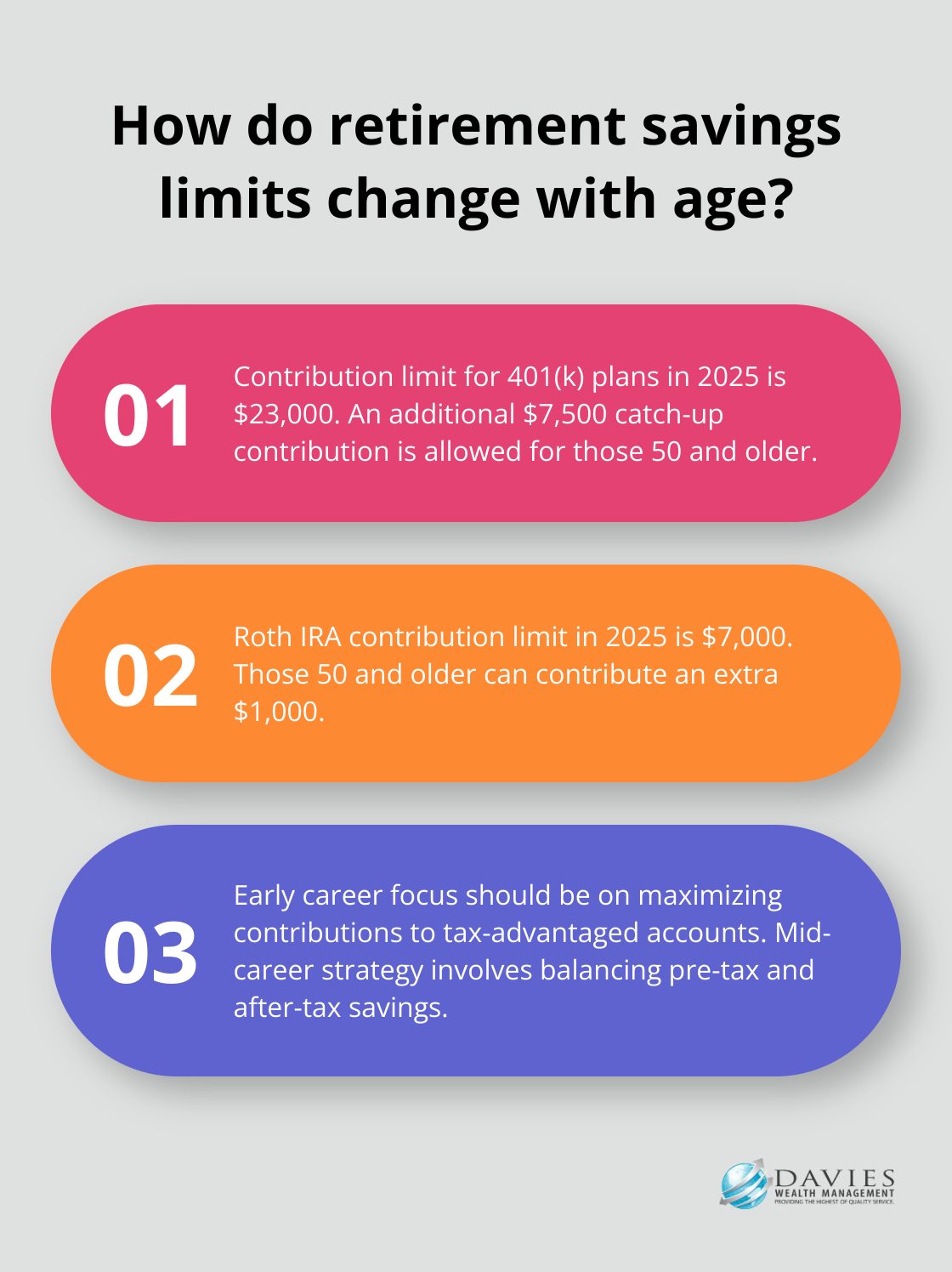

In the early stages of your career, you should focus on maximizing contributions to tax-advantaged accounts. The power of compound interest means that even small contributions can grow significantly over time. For 2025, the contribution limit for 401(k) plans is $23,000, with an additional $7,500 catch-up contribution for those 50 and older. Try to contribute at least enough to take full advantage of your employer’s match (if offered).

Opening a Roth IRA alongside your 401(k) is a smart move. In 2025, you can contribute up to $7,000 to a Roth IRA (plus an additional $1,000 if you’re 50 or older). While contributions come from after-tax dollars, the growth and withdrawals in retirement are tax-free. This can benefit you if you expect to be in a higher tax bracket in retirement.

Mid-Career: Diversifying Your Tax Exposure

As your income grows, you must balance pre-tax and after-tax savings. This approach, known as tax diversification, gives you more flexibility in retirement. Continue maximizing your 401(k) contributions, but also consider increasing your Roth IRA contributions if you’re eligible.

If your income exceeds the Roth IRA contribution limits, explore the backdoor Roth IRA strategy. This involves making a non-deductible contribution to a traditional IRA and then immediately converting it to a Roth IRA. However, be aware of the pro-rata rule, which dictates that your Roth conversion will be taxed proportionate to your pre- and post-tax percentages.

Near Retirement: Strategic Positioning

As you approach retirement, focus on positioning your accounts for tax-efficient withdrawals. This is an ideal time to consider Roth conversion ladders. This strategy involves converting a portion of your pre-tax retirement account into a Roth IRA, which entails a tax liability as the converted amount is treated as taxable income.

Another strategy to consider is asset location. This involves placing tax-inefficient investments (like bonds) in tax-deferred accounts and more tax-efficient investments (like low-turnover stock funds) in taxable accounts. This approach can help minimize your tax liability while maintaining your desired asset allocation.

Professional Athletes: Unique Considerations

Professional athletes face distinct financial challenges due to their short career spans and fluctuating income. If you’re an athlete, you should consider aggressive savings strategies during high-earning years. You might benefit from a combination of tax-deferred and Roth accounts to manage your current tax burden while setting up tax-free income for the future.

Davies Wealth Management specializes in financial planning for professional athletes. We understand the complexities of your financial situation and can help you develop strategies that address your unique needs.

The Importance of Professional Guidance

Tax-efficient retirement planning requires ongoing adjustments as your financial situation evolves. While these strategies can be powerful tools for maximizing your retirement savings, they can also be complex. Working with a financial advisor who understands your unique situation can help ensure you’re making the most of these opportunities at every stage of your career.

Final Thoughts

Tax-efficient retirement strategies offer a powerful way to maximize savings and secure financial futures. These approaches, from Roth IRA conversions to strategic withdrawals, provide unique benefits tailored to individual circumstances and goals. The effectiveness of each strategy depends on personal financial situations, career stages, and retirement objectives.

Professional guidance proves invaluable in navigating the complexities of retirement planning. At Davies Wealth Management, we create tailored financial plans that incorporate tax-efficient retirement strategies. Our team works closely with clients to develop comprehensive strategies aligned with specific needs and goals.

Tax-efficient retirement planning requires ongoing adjustments as life circumstances change and tax laws evolve. Regular reviews and updates to retirement plans ensure individuals stay on track to meet their financial goals. With the right strategies in place, one can look forward to a financially secure and rewarding retirement.

✅ BOOK AN APPOINTMENT TODAY: https://davieswealth.tdwealth.net/appointment-page

===========================================================

SEE ALL OUR LATEST BLOG POSTS: https://tdwealth.net/articles

If you like the content, smash that like button! It tells YouTube you were here, and the Youtube algorithm will show the video to others who may be interested in content like this. So, please hit that LIKE button!

Don’t forget to SUBSCRIBE here: https://www.youtube.com/channel/UChmBYECKIzlEBFDDDBu-UIg

✅ Contact me: TDavies@TDWealth.Net

====== ===Get Our FREE GUIDES ==========

Retirement Income: The Transition into Retirement: https://davieswealth.tdwealth.net/retirement-income-transition-into-retirement

Beginner’s Guide to Investing Basics: https://davieswealth.tdwealth.net/investing-basics

✅ Want to learn more about Davies Wealth Management, follow us here!

Website:

Podcast:

Social Media:

https://www.facebook.com/DaviesWealthManagement

https://twitter.com/TDWealthNet

https://www.linkedin.com/in/daviesrthomas

https://www.youtube.com/c/TdwealthNetWealthManagement

Lat and Long

27.17404889406371, -80.24410438798957

Davies Wealth Management

684 SE Monterey Road

Stuart, FL 34994

772-210-4031

#Retirement #FinancialPlanning #wealthmanagement

DISCLAIMER

The content provided by Davies Wealth Management is intended solely for informational purposes and should not be considered as financial, tax, or legal advice. While we strive to offer accurate and timely information, we encourage you to consult with qualified retirement, tax, or legal professionals before making any financial decisions or taking action based on the information presented. Davies Wealth Management assumes no liability for actions taken without seeking individualized professional advice.

Leave a Reply