At Davies Wealth Management, we understand the power of tax-deferred strategies for building long-term wealth. These approaches allow you to grow your savings without immediate tax implications, potentially leading to significant financial benefits over time.

In this post, we’ll explore various tax-deferred strategies and how to implement them effectively. From maximizing retirement account contributions to leveraging lesser-known options, we’ll provide practical insights to help you optimize your savings and secure your financial future.

What Are Tax-Deferred Savings Strategies?

The Essence of Tax Deferral

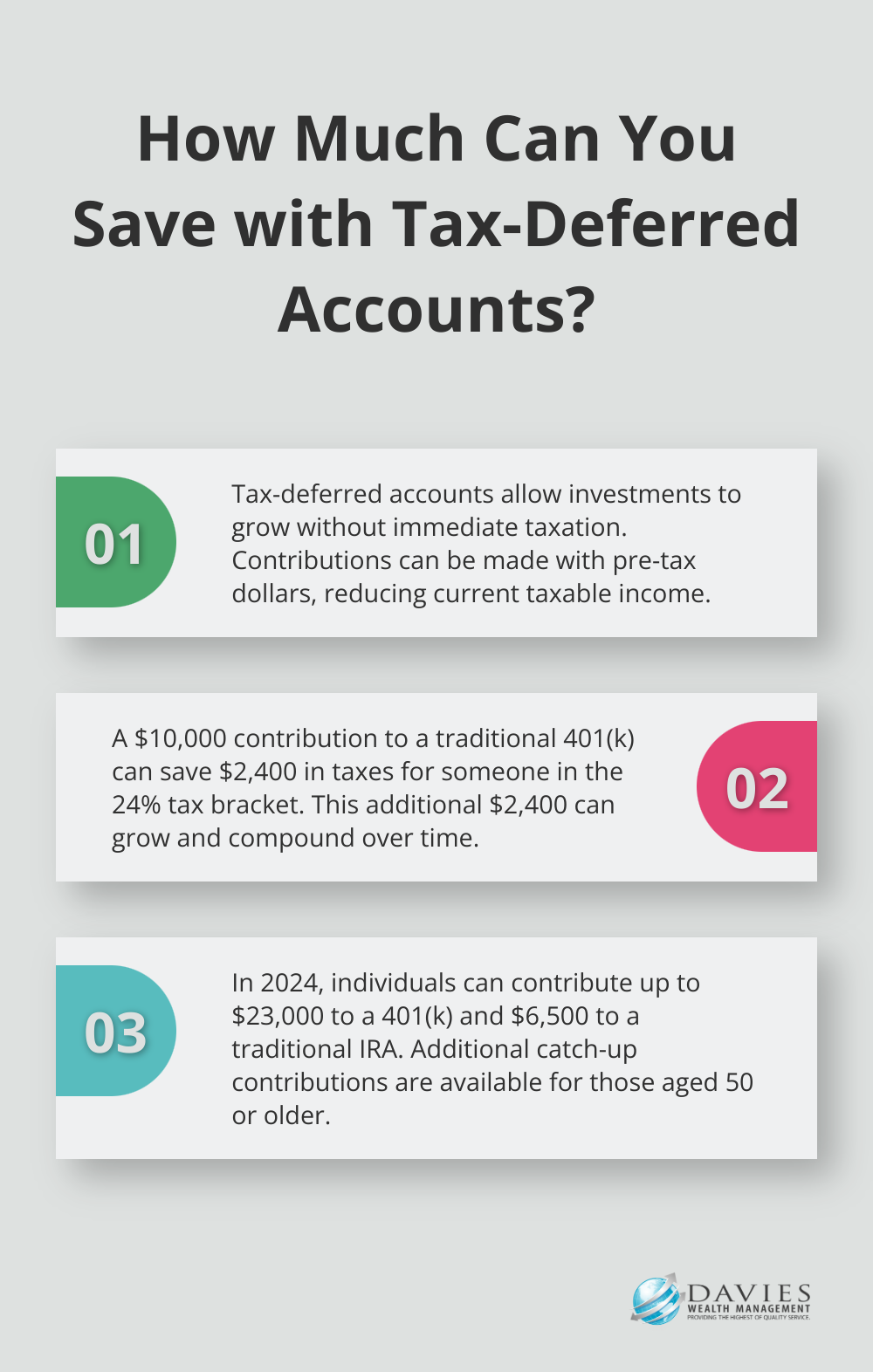

Tax-deferred savings strategies serve as powerful tools for wealth accumulation over time. These strategies allow your investments to grow without immediate tax payments diminishing them, typically until you withdraw the funds in retirement.

The Advantage of Postponing Taxes

When you utilize tax-deferred accounts, you essentially receive an interest-free loan from the government. Contributions to these accounts allow you to postpone paying taxes until you begin making withdrawals, potentially resulting in significantly larger account balances compared to taxable accounts.

Consider this example: If you fall within the 24% tax bracket and contribute $10,000 to a traditional 401(k), you’ll save $2,400 in taxes this year. That’s an additional $2,400 that can grow and compound over time.

Popular Tax-Deferred Accounts

Several types of accounts offer tax-deferred benefits. The most well-known include:

- Traditional Individual Retirement Accounts (IRAs)

- Employer-sponsored 401(k) plans

These accounts allow you to contribute pre-tax dollars, which reduces your current taxable income.

For self-employed individuals or small business owners, SEP IRAs and Solo 401(k)s offer similar benefits with potentially higher contribution limits. In 2024, you can contribute up to $23,000 to a 401(k) and $6,500 to a traditional IRA (with additional catch-up contributions available for those aged 50 or older).

Expanding Beyond Retirement Accounts

While retirement accounts dominate the tax-deferred landscape, other options exist:

- Health Savings Accounts (HSAs): These accounts offer triple tax benefits (tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses).

- 529 College Savings Plans: These plans provide tax-free growth and withdrawals for education expenses.

Many financial advisors recommend a mix of these strategies, tailoring the approach to each individual’s financial situation and goals. The strategic use of these tax-deferred options can potentially save thousands in taxes over your lifetime and accelerate your path to financial security.

As we move forward, let’s explore how to maximize your contributions to these tax-deferred accounts, starting with traditional retirement vehicles.

How to Maximize Your Retirement Account Contributions

Traditional IRA Strategies

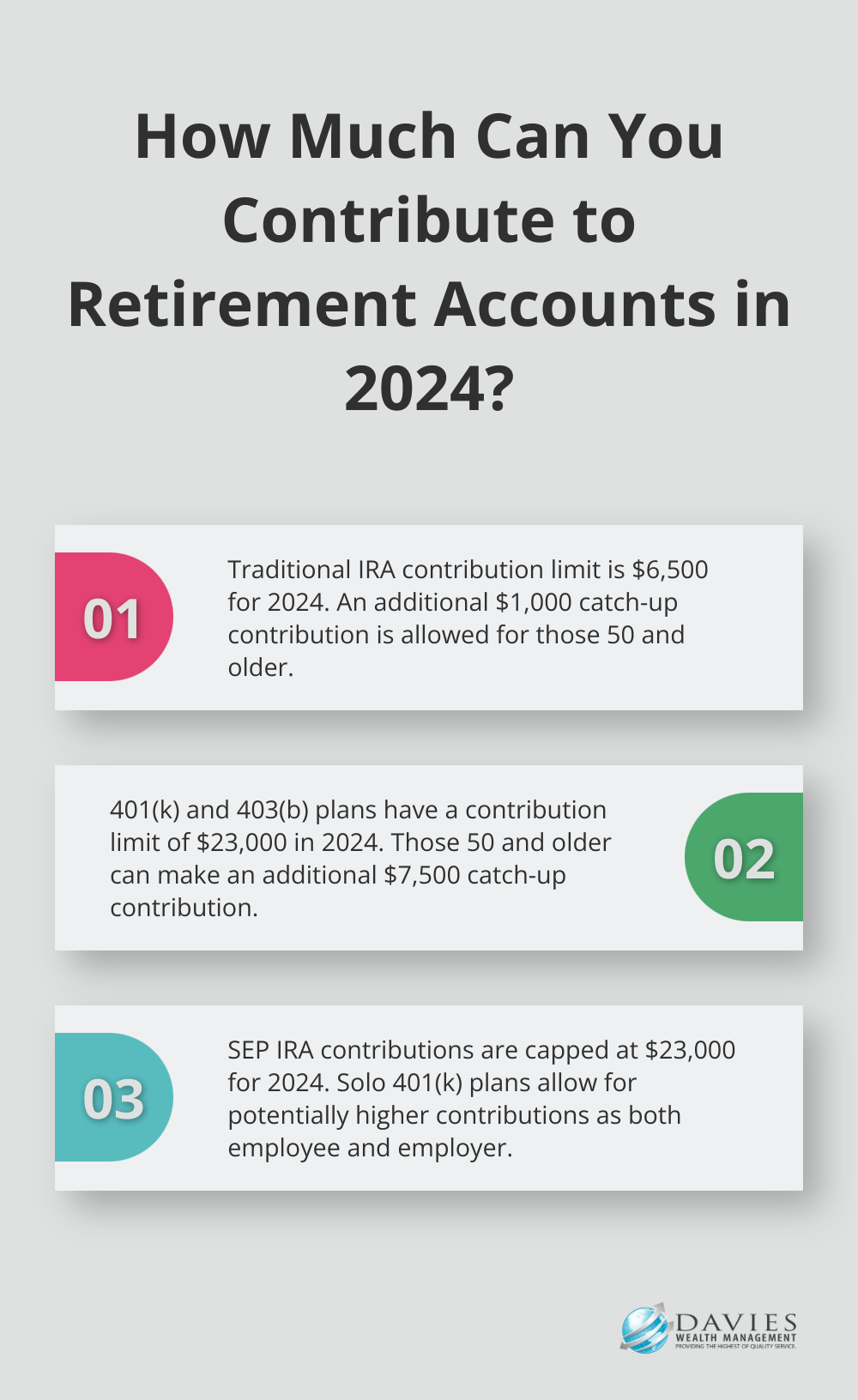

For 2024, the contribution limit for traditional IRAs stands at $6,500, with an additional $1,000 catch-up contribution allowed for those 50 and older. To make the most of your IRA:

- Contribute early in the year to maximize tax-deferred growth.

- Set up automatic monthly contributions to ensure you hit the annual limit.

- Take advantage of catch-up contributions if you’re over 50.

Traditional IRA contributions may be tax-deductible depending on your income and whether you or your spouse participates in a retirement plan at work. Always consult with a tax professional to understand your specific situation.

Optimizing 401(k) and 403(b) Plans

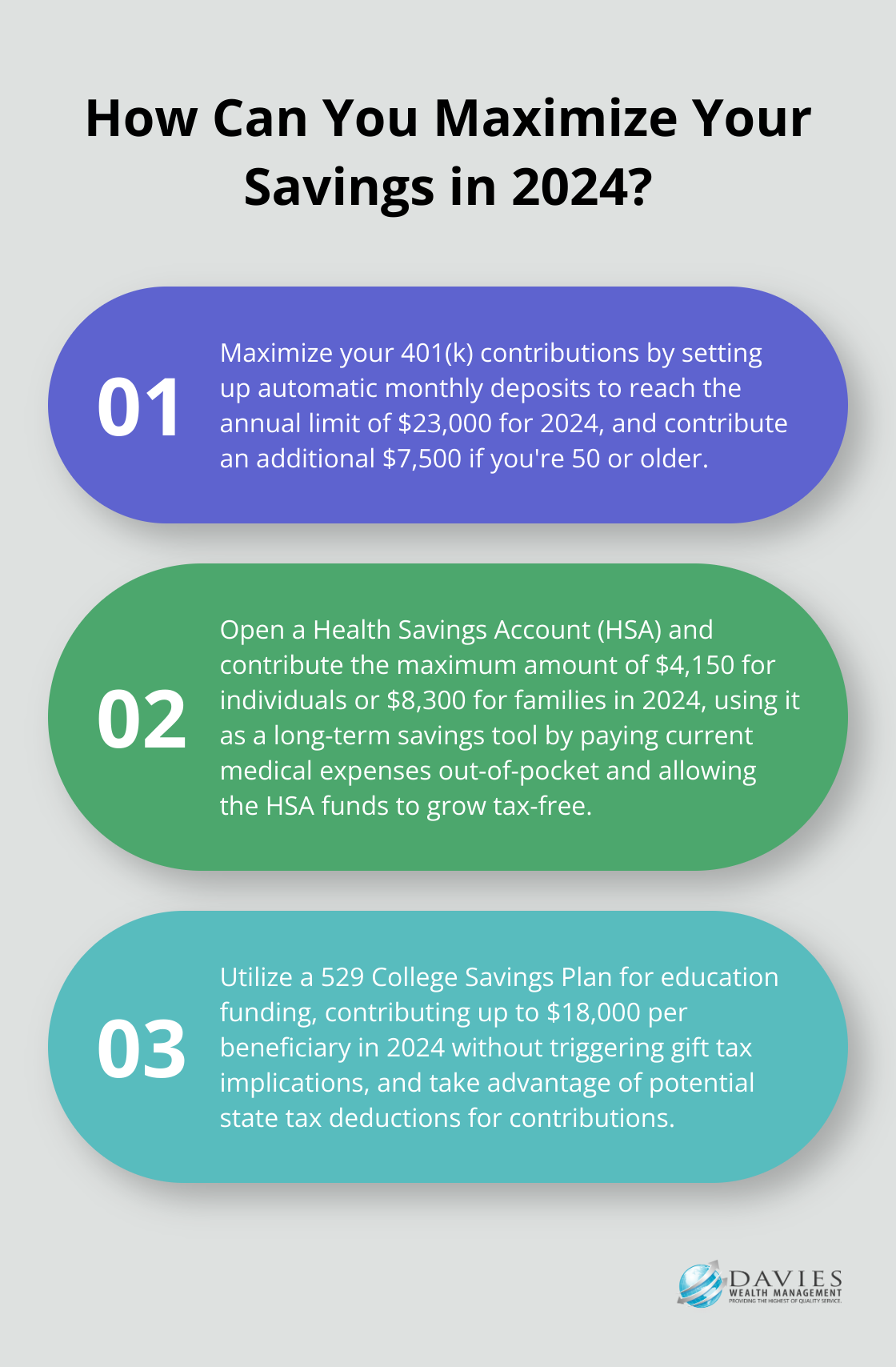

Employer-sponsored plans like 401(k)s and 403(b)s offer higher contribution limits than IRAs. For 2024, you can contribute up to $23,000, with an additional $7,500 catch-up contribution for those 50 and older. To maximize these plans:

- Contribute enough to get your full employer match – it’s essentially free money.

- Max out your contributions if possible. Even small increases can have a big impact over time.

- Consider using a Roth 401(k) option if available, especially if you expect to be in a higher tax bracket in retirement.

The average 401(k) balance across all age groups is $134,128, according to Vanguard’s annual report. You could potentially exceed this average by maximizing your contributions.

Self-Employed Retirement Plans

For self-employed individuals or small business owners, SEP IRAs and Solo 401(k)s offer powerful tax-deferred savings opportunities. These plans allow for significantly higher contributions than traditional IRAs or employer-sponsored plans.

With a SEP IRA, your total annual employee contributions to all plans can’t exceed $23,000 in 2024. A Solo 401(k) allows you to contribute as both an employee and employer, potentially allowing for even higher contributions.

For high-earning self-employed individuals, these plans can result in substantial tax savings. For example, a self-employed consultant earning $250,000 could potentially contribute significantly to a SEP IRA, reducing their taxable income.

The Power of Consistency and Strategic Planning

The key to maximizing your retirement account contributions is consistency and strategic planning. Start early, contribute regularly, and stay informed about changes in contribution limits and tax laws. With the right approach, you can build a substantial nest egg while enjoying valuable tax benefits along the way.

As we move forward, let’s explore additional tax-deferred options beyond traditional retirement accounts that can further enhance your savings strategy.

Beyond Retirement Accounts: Expanding Your Tax-Deferred Options

Health Savings Accounts: The Triple Tax Advantage

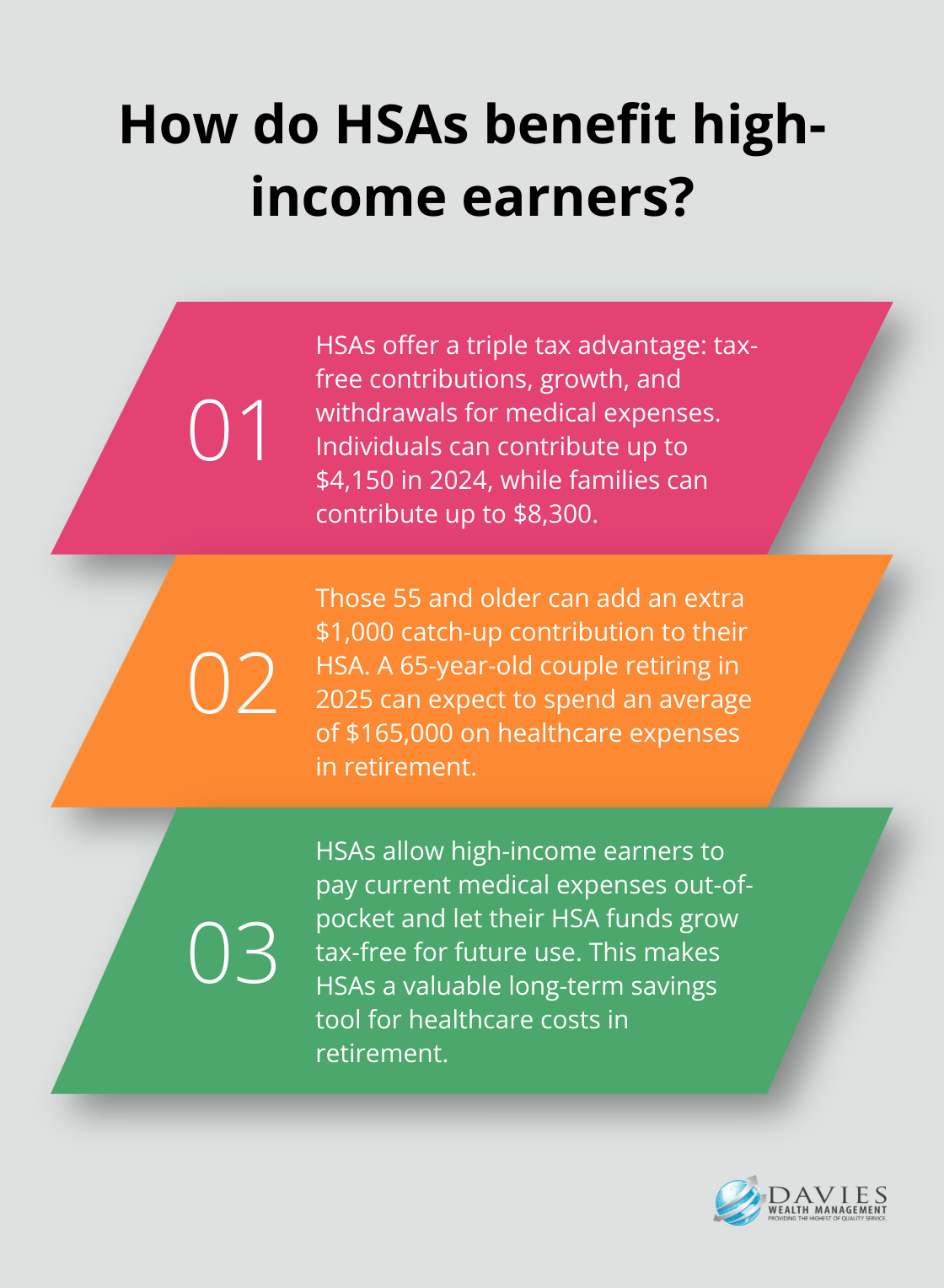

Health savings accounts offer a unique triple tax advantage: tax-free contributions, investment growth, and withdrawals for qualified medical expenses. In 2024, individuals can contribute up to $4,150, while families can contribute up to $8,300. Those 55 and older can add an extra $1,000 catch-up contribution.

HSAs benefit high-income earners, including professional athletes, who can pay current medical expenses out-of-pocket and allow their HSA funds to grow tax-free for future use. A 65-year-old couple retiring this year can expect to spend an average of $165,000 on healthcare expenses in retirement, making HSAs a valuable long-term savings tool.

529 College Savings Plans: Tax-Free Education Funding

529 plans offer tax-free growth and withdrawals for qualified education expenses. While contributions are not federally tax-deductible, many states offer tax deductions or credits for contributions. New York residents, for example, can deduct up to $5,000 ($10,000 for married couples) in contributions from their state taxable income.

These plans work well for high-income earners who want to fund education expenses for children or grandchildren. In 2024, individuals can gift up to $18,000 in a single 529 plan without those funds counting against the lifetime gift tax exemption amount, making 529 plans an attractive option for those with substantial assets.

Annuities: Guaranteed Income with Tax Benefits

Annuities provide another avenue for tax-deferred growth, particularly beneficial for those who have maxed out other tax-advantaged accounts. While complex, annuities can provide a guaranteed income stream in retirement, with taxes deferred until withdrawals begin.

A deferred annuity allows your investment to grow tax-deferred for a set period. An investment of $100,000 in a deferred annuity earning 5% annually could grow to over $162,000 in 10 years, all without incurring taxes on the gains during that period.

However, annuities come with higher fees and less liquidity than other investment options. You must carefully consider whether the tax benefits and guaranteed income outweigh these drawbacks for your specific situation.

Tailored Strategies for Professional Athletes

Professional athletes face unique financial challenges, including short career spans and fluctuating income. Tax-deferred options like HSAs, 529 plans, and annuities can play a significant role in their long-term financial planning. These tools help athletes manage their current wealth and secure their financial future beyond their playing years.

The Importance of Professional Guidance

The right mix of these tax-deferred options can significantly enhance your long-term financial security, providing tax benefits today and a more stable financial future tomorrow. However, navigating these complex financial tools requires expertise. Professional financial advisors can help determine the most effective combination of tax-deferred strategies for your specific situation and goals.

Final Thoughts

Tax-deferred strategies offer powerful tools for building long-term wealth and securing financial stability. These vehicles provide numerous opportunities to grow your savings while minimizing current tax burdens. Maximizing contributions to these accounts and leveraging their unique benefits can potentially save thousands in taxes over your lifetime and accelerate your path to financial security.

Implementing tax-deferred strategies effectively requires careful planning and consideration of your individual financial situation. Each person’s circumstances are unique, and what works best for one may not be ideal for another. This is where personalized financial planning becomes essential to ensure you make the most of available tax-deferred options while aligning with your specific goals, risk tolerance, and long-term financial objectives.

The team at Davies Wealth Management specializes in helping individuals, families, and professional athletes navigate the complexities of tax-deferred strategies and comprehensive wealth management. We understand the unique financial challenges faced by different groups (including the short career spans and fluctuating incomes of professional athletes). Our experts work closely with clients to develop personalized financial plans that maximize the benefits of tax-deferred savings while addressing their specific needs and goals.

Leave a Reply