At Davies Wealth Management, we understand the importance of effective tax reduction strategies for both individuals and businesses.

Implementing legal methods to minimize your tax burden can significantly impact your financial well-being and help you keep more of your hard-earned money.

In this post, we’ll explore practical tax reduction strategies that can help you optimize your tax situation while staying compliant with the law.

What Are Tax Reduction Strategies?

Tax Avoidance vs. Tax Evasion

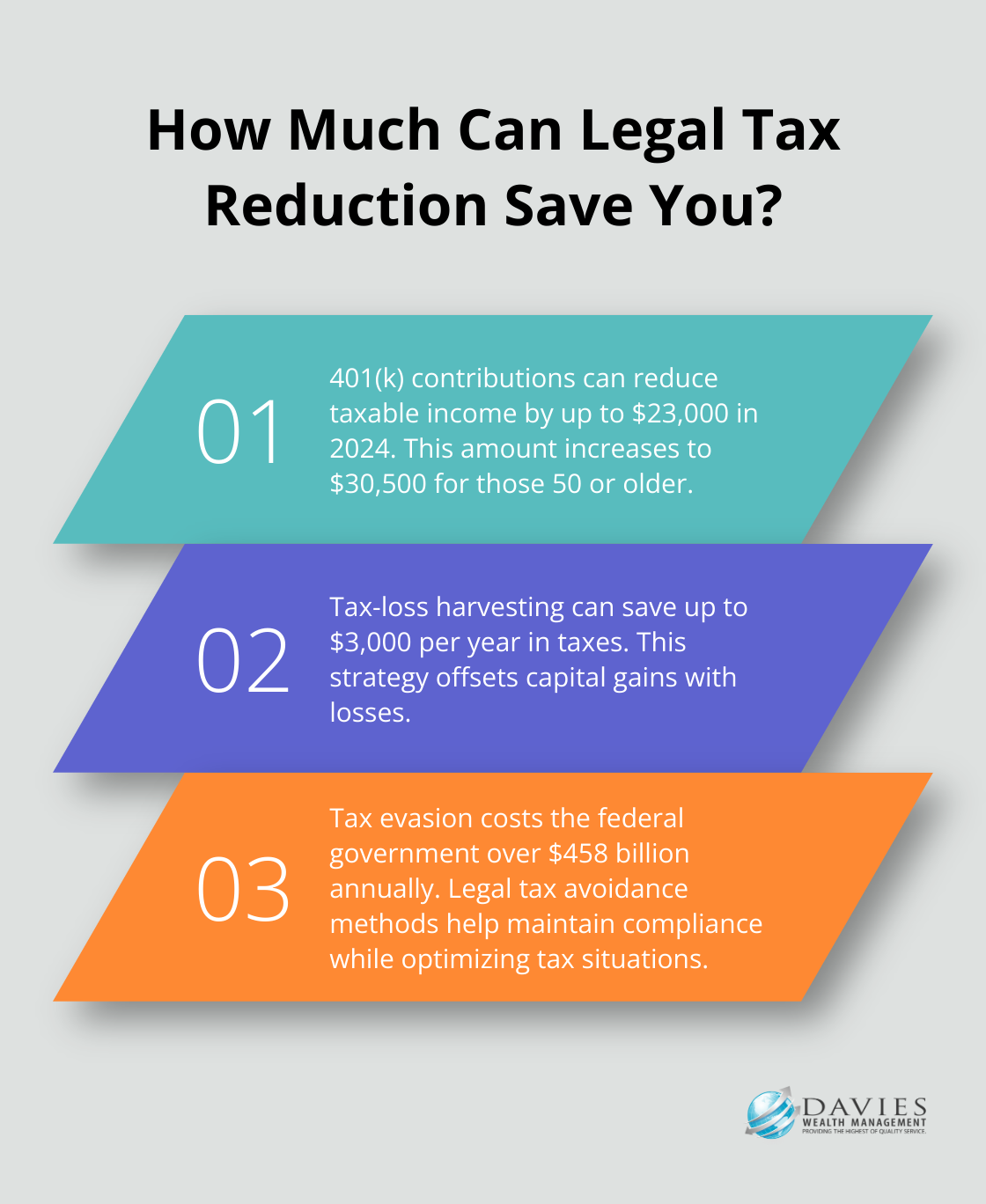

At Davies Wealth Management, we empower our clients with knowledge about effective and legal tax reduction strategies. These strategies serve as essential tools for wealth maximization and financial goal achievement. We must distinguish between tax avoidance and tax evasion. Tax avoidance involves legal methods to reduce tax liability by leveraging provisions in the tax code. This includes strategies such as maximizing deductions, contributing to retirement accounts, or structuring investments tax-efficiently. Tax evasion, however, is the illegal practice of not paying owed taxes. The IRS reports that tax evasion costs the federal government over $458 billion annually. We always advocate for legal tax reduction methods to ensure our clients maintain compliance while optimizing their tax situation.

The Power of Legal Tax Reduction

Legal tax reduction strategies prove powerful for wealth building and preservation. For example, contributing to a 401(k) can reduce taxable income by up to $23,000 in 2024 ($30,500 for those 50 or older). This strategy not only lowers the current tax bill but also allows investments to grow tax-deferred. Another effective approach is tax-loss harvesting, which can save up to $3,000 per year in taxes by offsetting capital gains with losses.

Proactive Tax Planning Benefits

Proactive tax planning should occur year-round and can yield significant benefits. Staying informed about tax law changes and regularly reviewing your financial situation allows you to identify opportunities to reduce your tax burden. For instance, the SECURE Act 2.0 introduced new provisions for retirement savings, including higher catch-up contribution limits for those aged 60-63 (starting in 2025).

Implementing Effective Strategies

Implementing these strategies effectively requires expertise in tax-efficient investing and financial planning. This ensures you don’t leave money on the table when it comes to your taxes. Whether you’re a professional athlete managing variable income or a business owner looking to optimize your tax situation, understanding and applying these strategies can significantly impact your financial well-being.

As we move forward, let’s explore specific tax reduction strategies for individuals that can help you keep more of your hard-earned money and work towards your financial goals.

Smart Tax Strategies for Individuals

Maximize Retirement Contributions

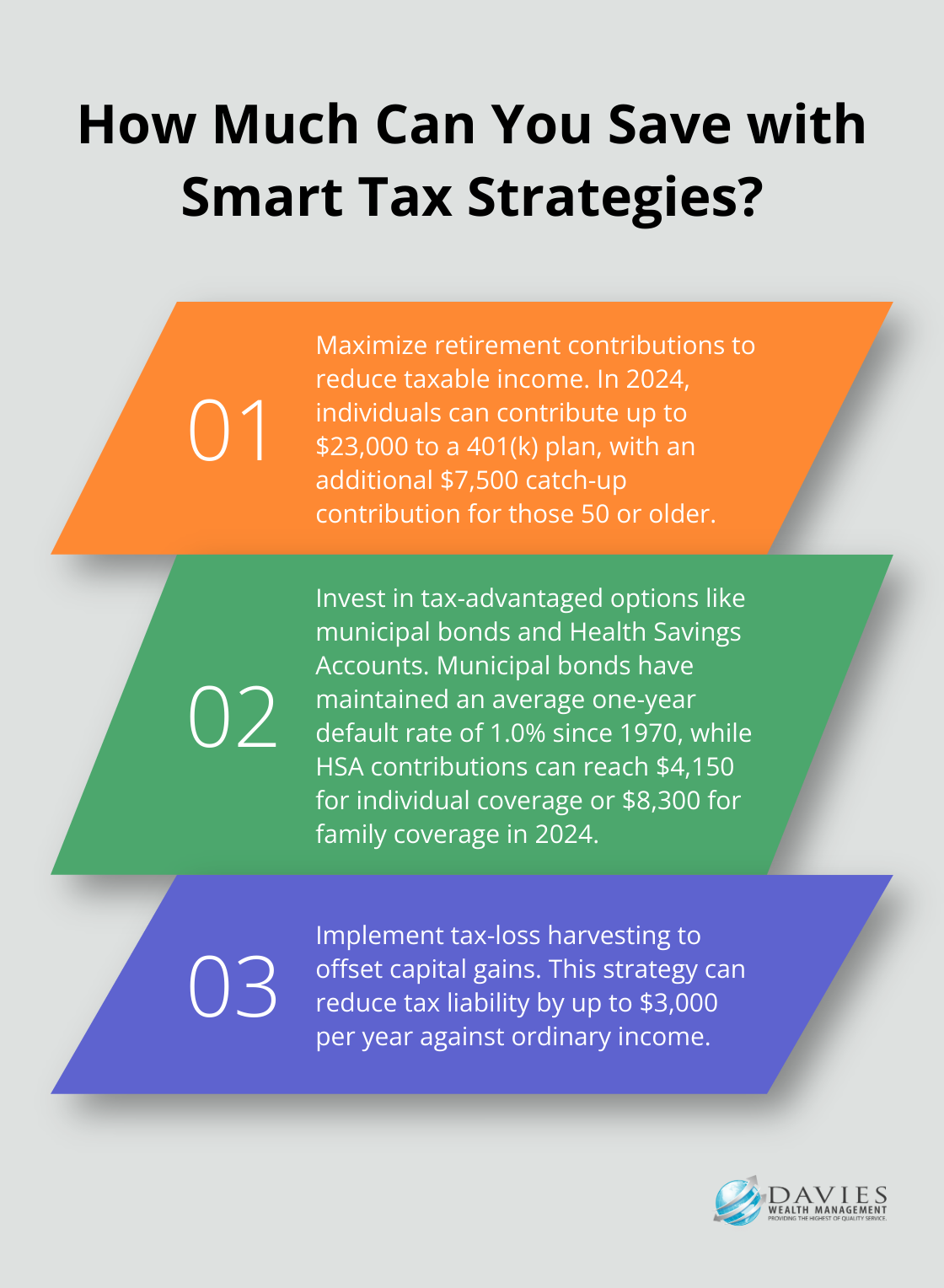

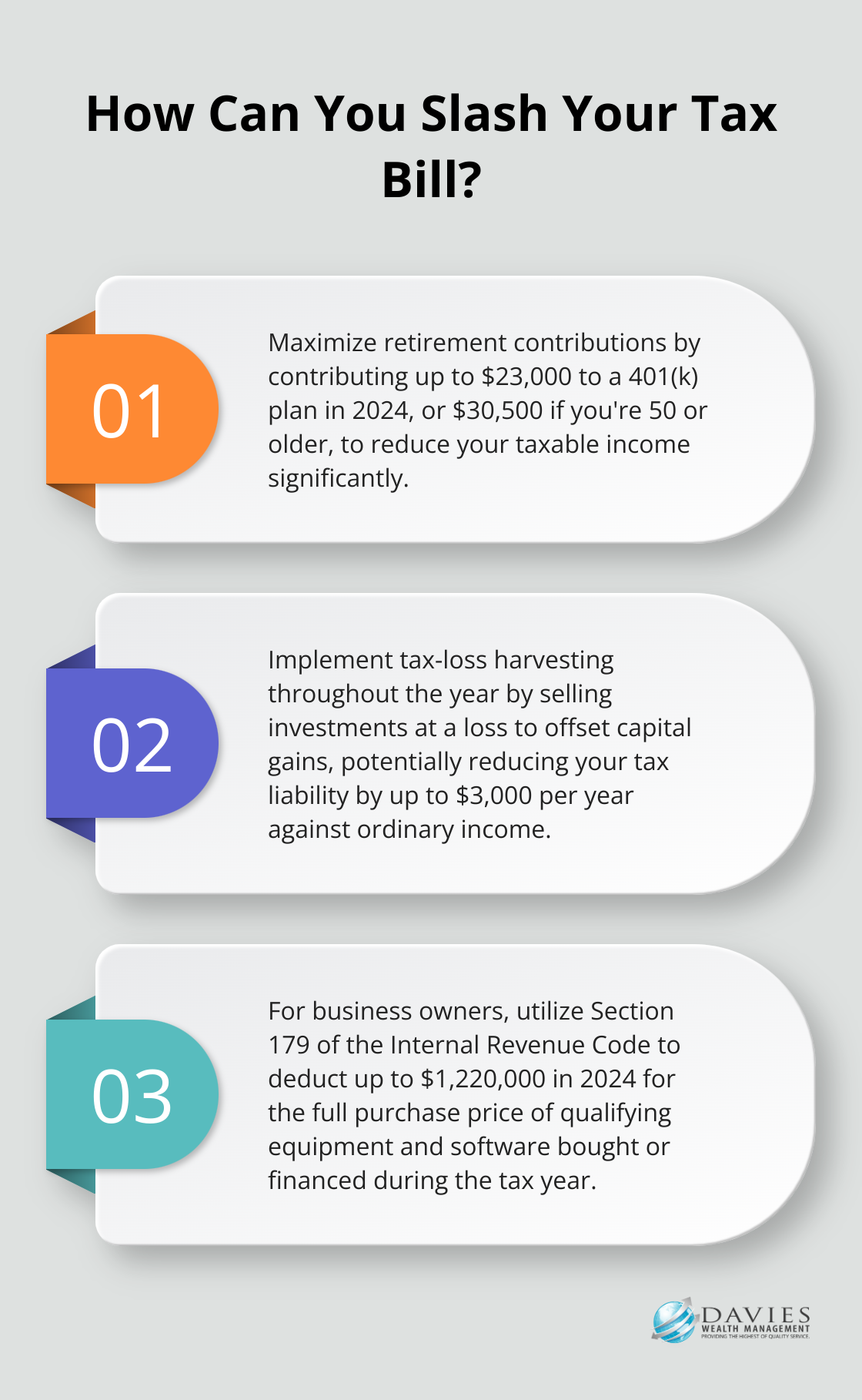

One of the most effective ways to reduce taxable income involves maximizing contributions to retirement accounts. In 2024, individuals can contribute up to $23,000 to a 401(k) plan. If you’re age 50 or older, you’re eligible for an additional $7,500 in catch-up contributions, raising your employee deferral limit to $30,500. For IRAs, the limit stands at $7,000 (with a $1,000 catch-up contribution). Maxing out these accounts could potentially reduce taxable income significantly.

Leverage Tax-Advantaged Investments

Investing in municipal bonds provides tax-free interest income at the federal level (and potentially at state and local levels). According to Moody’s Investors Service, municipal bonds have maintained an average one-year SG municipal default rate of 1.0% since 1970, making them a relatively safe investment option. Health Savings Accounts (HSAs) offer another tax-advantaged option for those with high-deductible health plans. In 2024, individuals can contribute up to $4,150 for individual coverage or $8,300 for family coverage, enjoying triple tax advantages.

Implement Strategic Tax-Loss Harvesting

Tax-loss harvesting involves selling investments at a loss to offset capital gains. This strategy can reduce tax liability by up to $3,000 per year against ordinary income. For optimal results, implement this strategy throughout the year rather than waiting until December. This approach proves particularly effective for individuals with variable income, such as professional athletes.

Utilize Charitable Giving for Tax Benefits

Strategic charitable giving supports causes while providing significant tax benefits. For those aged 70½ or older, Qualified Charitable Distributions (QCDs) allow donations of up to $100,000 annually from an IRA directly to charities, avoiding income tax on the distribution. Donating appreciated securities instead of cash allows individuals to avoid capital gains taxes while still claiming the full market value as a deduction.

Time Income and Deductions

For high-income earners, timing income and deductions plays a critical role in tax management. Consider deferring income to the following year if you expect to be in a lower tax bracket. Conversely, if you anticipate being in a higher bracket next year, accelerating income into the current year might prove beneficial. The same principle applies to deductions – bunching deductions into a single year can help surpass the standard deduction threshold and itemize for greater tax benefits.

These strategies require careful planning and expertise. While we’ve outlined powerful methods here, every individual’s financial situation remains unique. Professional guidance can help create personalized tax strategies that align with overall financial goals, whether you’re a professional athlete, business owner, or individual seeking to optimize your tax situation. As we move forward, let’s explore how businesses can implement effective tax reduction strategies to enhance their financial performance.

Optimizing Business Tax Strategies

Selecting the Optimal Business Structure

The choice of business structure affects tax obligations significantly. S corporations provide tax advantages by allowing business income to pass through to the owner’s personal tax return, potentially reducing self-employment taxes. The IRS reported 5.1 million S corporation tax returns filed in 2018, highlighting its popularity among small businesses.

Limited Liability Companies (LLCs) offer flexibility in taxation. They can be taxed as sole proprietorships, partnerships, or corporations, allowing businesses to choose the most advantageous option. This flexibility can lead to substantial tax savings when aligned with the company’s financial goals.

Strategic Timing of Income and Expenses

Timing plays a critical role in tax planning. Businesses can defer income to the following tax year by delaying billings or accelerate expenses by making purchases before year-end. This strategy works particularly well for cash-basis taxpayers.

A business expecting a lower tax bracket next year might benefit from deferring income. Conversely, if higher taxes are anticipated, accelerating income into the current year could prove advantageous. The key is to align these decisions with the company’s overall financial strategy and cash flow needs.

Maximizing Depreciation Benefits

Section 179 of the Internal Revenue Code allows businesses to deduct the full purchase price of qualifying equipment and software purchased or financed during the tax year. For 2024, the deduction limit stands at $1,220,000. This can result in significant tax savings, especially for businesses making substantial equipment investments.

Bonus depreciation serves as another powerful tool. The 100% write-off of eligible property expired December 31, 2022. Unless the law changes, the bonus percentage will decrease by 20 points in subsequent years, making it important for businesses to understand the current benefits available.

Implementing Strategic Employee Benefits

Offering comprehensive employee benefits not only attracts and retains talent but also provides tax advantages. Employer contributions to health insurance premiums, retirement plans, and certain other benefits are tax-deductible for the business and often tax-free for employees.

Implementing a 401(k) plan allows businesses to deduct contributions made on behalf of employees. In 2024, employers can contribute up to $69,000 per employee (including employee deferrals), potentially leading to substantial tax savings.

Leveraging Research and Development Credits

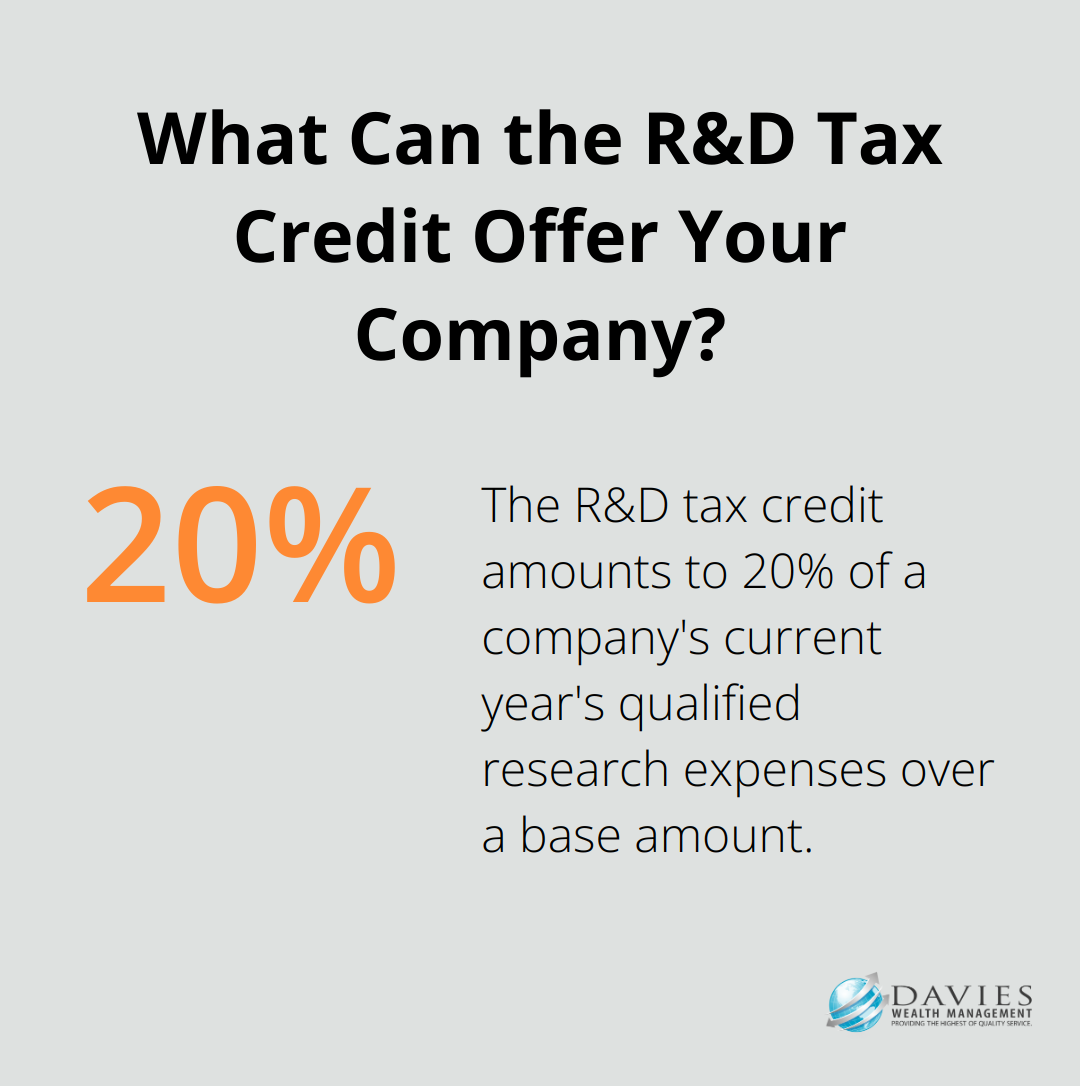

The R&D tax credit can transform innovative businesses. This credit amounts to 20% of your company’s current year’s qualified research expenses over a base amount.

Even small businesses and startups can benefit from this credit. Eligible startups can use the credit to offset up to $250,000 in payroll taxes annually. This can boost cash-strapped new businesses investing in innovation significantly.

Final Thoughts

Effective tax reduction strategies can significantly impact your financial well-being. These approaches offer powerful ways to minimize your tax burden legally, from maximizing retirement contributions to selecting the right business structure. However, the complex landscape of tax laws and regulations requires expertise and careful planning.

Working with a qualified tax professional ensures you make informed decisions that align with your overall financial goals. At Davies Wealth Management, we develop personalized tax strategies that cater to your unique situation (whether you’re a professional athlete managing variable income or a business owner looking to optimize your tax position).

Tax reduction strategies are not one-size-fits-all solutions. What works for one individual or business may not be the best approach for another. Take the first step towards optimizing your tax situation and securing your financial future by partnering with Davies Wealth Management. Our team of experts will help you navigate the complexities of tax planning and wealth management.

Leave a Reply