Tax deferral strategies are powerful tools for managing your financial future. By postponing tax payments, you can potentially grow your wealth faster and more efficiently.

At Davies Wealth Management, we’ve seen firsthand how effective tax deferral can transform our clients’ financial landscapes. This post will guide you through various methods to implement these strategies, from basic techniques to advanced approaches that can significantly impact your long-term financial health.

What Are Tax Deferral Strategies?

The Essence of Tax Deferral

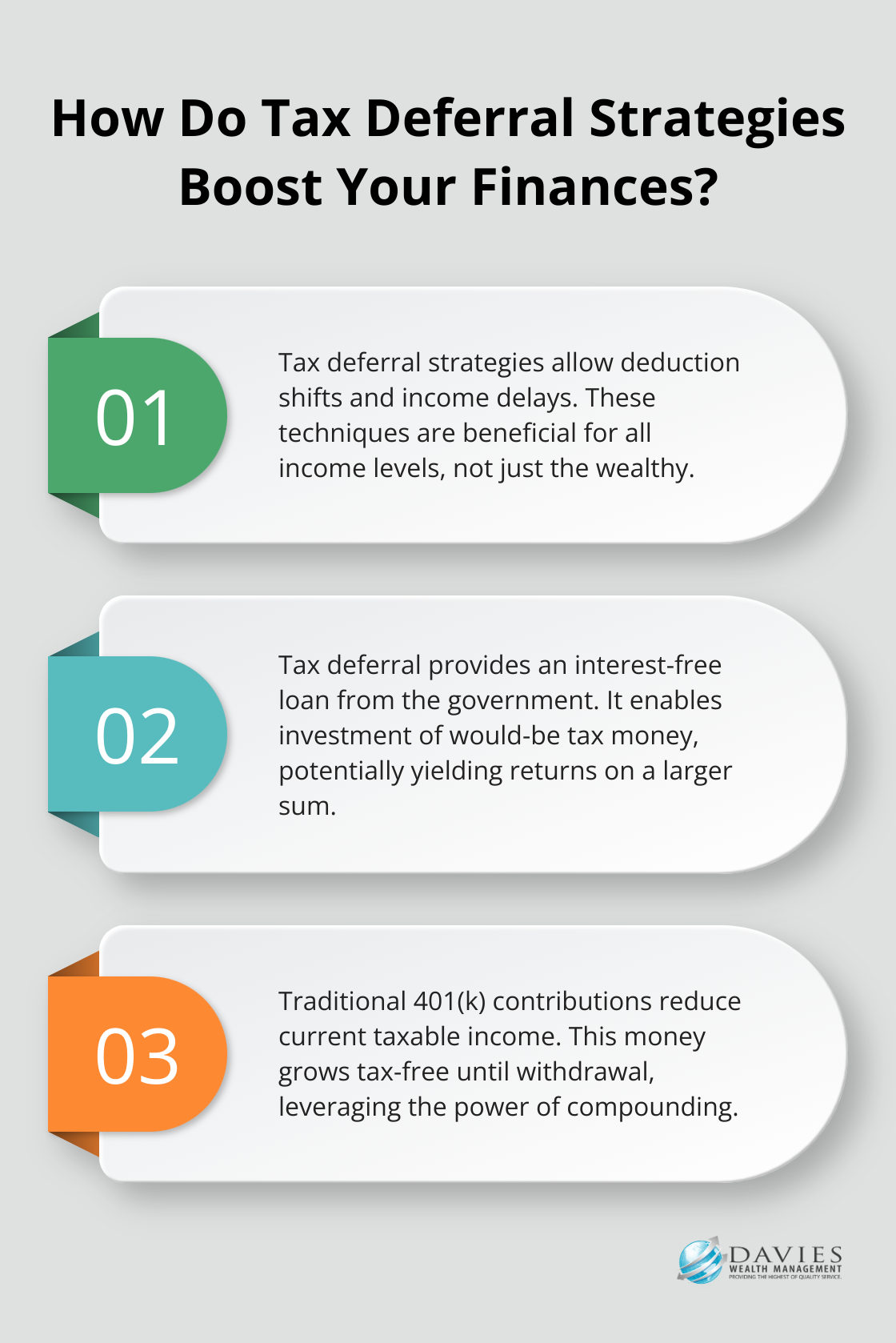

Tax deferral strategies are financial techniques that allow you to take a deduction and move it into an earlier year or defer some income to a later year. These strategies aren’t just for the wealthy – they’re valuable tools for anyone who wants to optimize their financial future.

The Mechanics of Tax Deferral

When you defer taxes, you give yourself an interest-free loan from the government. You keep and invest money that would otherwise go to taxes, potentially earning returns on a larger sum. For example, a contribution to a traditional 401(k) reduces your taxable income now, allowing that money to grow tax-free until withdrawal.

The Power of Compounding

The real advantage of tax deferral lies in the power of compounding in tax-deferred accounts. This investment growth can help compare fully taxable investments to tax-advantaged situations, potentially leading to significant differences in long-term wealth accumulation.

Dispelling Common Myths

Many people think tax deferral is just postponing the inevitable. While it’s true you’ll eventually pay taxes, you’re likely to be in a lower tax bracket in retirement. Plus, you’ve benefited from years of growth on money that would have gone to taxes.

Another misconception is that tax deferral only applies to retirement accounts. In reality, numerous strategies exist, from certain types of life insurance to real estate investments. Financial advisors (like those at Davies Wealth Management) can tailor these strategies to each client’s unique situation.

Beyond Retirement Accounts

Tax deferral isn’t limited to traditional retirement vehicles. Here are some other options:

- Deferred Annuities: These insurance products allow your money to grow tax-deferred until withdrawal.

- 1031 Exchanges: Real estate investors can defer capital gains tax on the sale of one investment property by reinvesting the proceeds into another like-kind property.

- Health Savings Accounts (HSAs): Contributions are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified medical expenses.

Tax deferral isn’t about avoiding taxes – it’s about controlling when you pay them. Understanding and implementing these strategies effectively can significantly enhance your long-term financial outlook. In the next section, we’ll explore some of the most popular methods to put these powerful concepts into action, including both basic and advanced techniques that can transform your financial landscape.

Maximizing Your Tax Deferral Options

Traditional IRAs and 401(k)s: Cornerstones of Tax-Deferred Savings

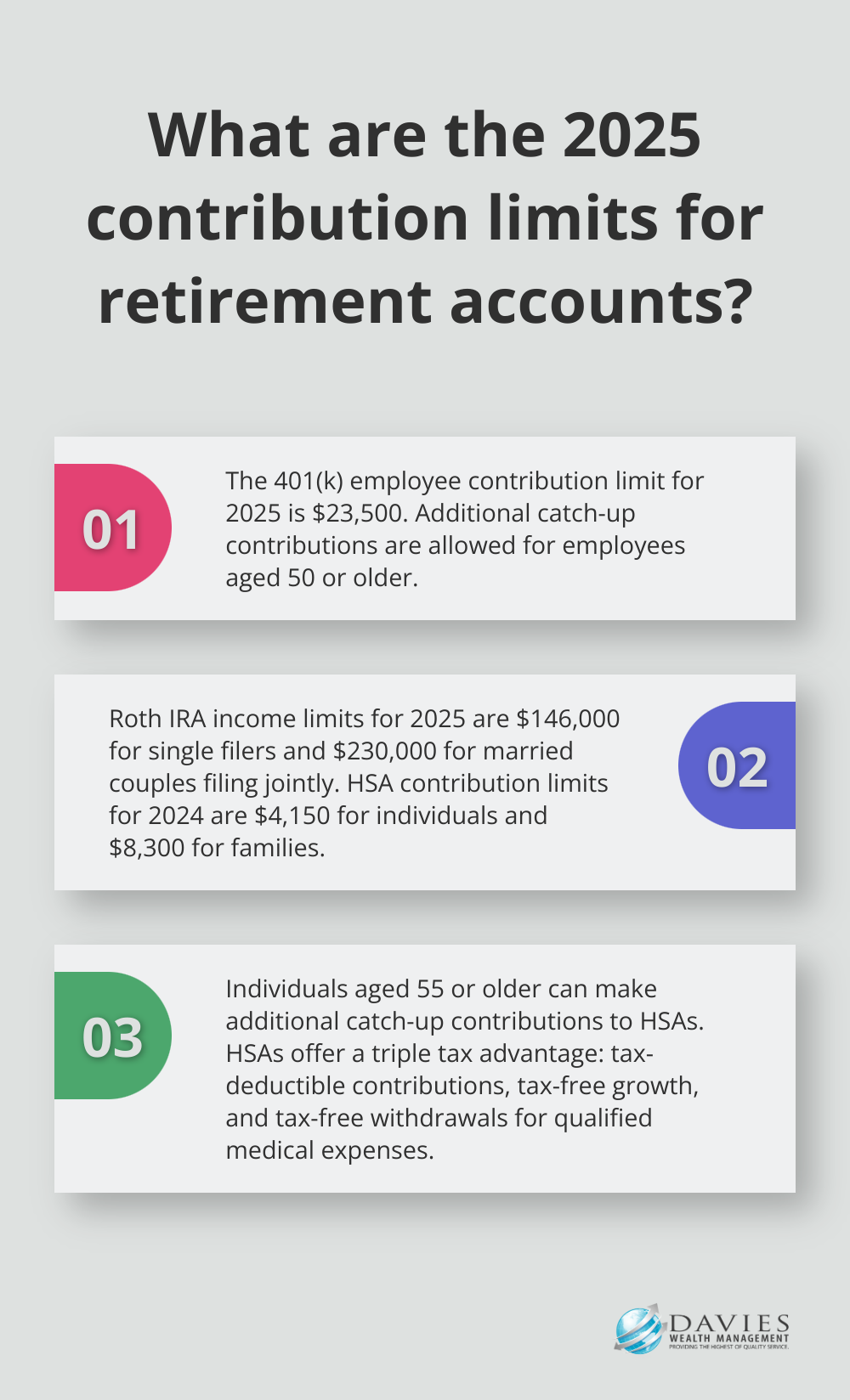

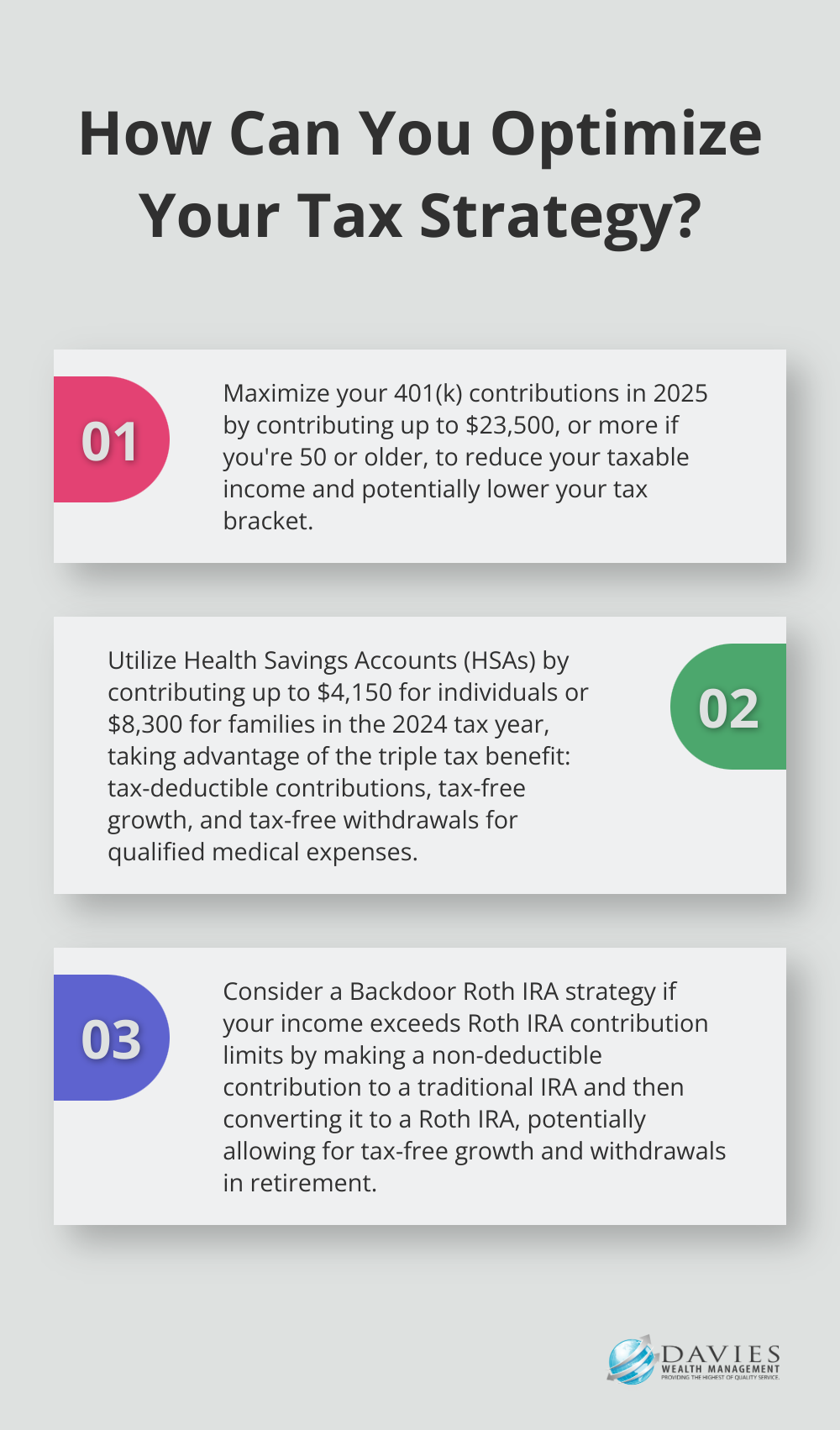

Traditional IRAs and 401(k)s remain popular choices for good reason. In 2025, the annual elective deferral limit for 401(k) plan employee contributions is increased to $23,500. Employees age 50 or older may contribute additional catch-up contributions. These contributions reduce your taxable income for the year, potentially lowering your tax bracket.

High earners, such as professional athletes, who max out these accounts can achieve substantial tax savings. An athlete in the 37% tax bracket who maximizes their 401(k) could save over $8,500 in taxes for the year.

Roth IRAs and Roth 401(k)s: Tax-Free Growth for the Future

Roth accounts don’t offer immediate tax benefits but provide tax-free growth and withdrawals in retirement. This can advantage individuals who expect to be in a higher tax bracket in the future.

For 2025, the income limits for Roth IRA contributions are $146,000 for single filers and $230,000 for married couples filing jointly. If your income exceeds these limits, consider a backdoor Roth IRA conversion (making a non-deductible contribution to a traditional IRA and then converting it to a Roth IRA).

Health Savings Accounts: Triple Tax Advantage

Health Savings Accounts offer a unique triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. For the 2024 tax year, you have until Tax Day 2025 to contribute up to $4,150 for individuals and $8,300 for families, while individuals age 55 or older can make an additional catch-up contribution.

HSAs can serve as powerful retirement savings tools. After age 65, you can withdraw funds for any purpose without penalty, paying only income tax on non-medical withdrawals.

Deferred Annuities: Guaranteed Income with Tax Benefits

Deferred annuities allow your money to grow tax-deferred until withdrawal. They can benefit those who’ve maxed out other tax-advantaged accounts. However, you must understand the fees and surrender charges associated with these products.

1031 Exchanges: Deferring Taxes on Real Estate Gains

For real estate investors, 1031 exchanges offer a way to defer capital gains taxes by reinvesting proceeds from the sale of one property into another “like-kind” property. This strategy can help build a real estate portfolio over time.

1031 exchanges come with strict rules. You must identify a replacement property within 45 days of selling the original property and complete the purchase within 180 days. Working with experienced professionals will help you navigate these complexities successfully.

While these strategies can significantly impact your long-term financial health, the best approach depends on your individual circumstances. Your current income, future expectations, and overall financial goals all play a role in determining the most effective tax deferral methods for you. In the next section, we’ll explore some advanced tax deferral techniques that can further enhance your financial strategy.

Advanced Tax Strategies for Savvy Investors

At Davies Wealth Management, we often encounter clients who seek more sophisticated tax deferral methods. These advanced strategies can significantly enhance wealth accumulation, but they require careful planning and execution. Let’s explore some powerful techniques that go beyond basic retirement accounts.

Backdoor Roth IRA: A Workaround for High Earners

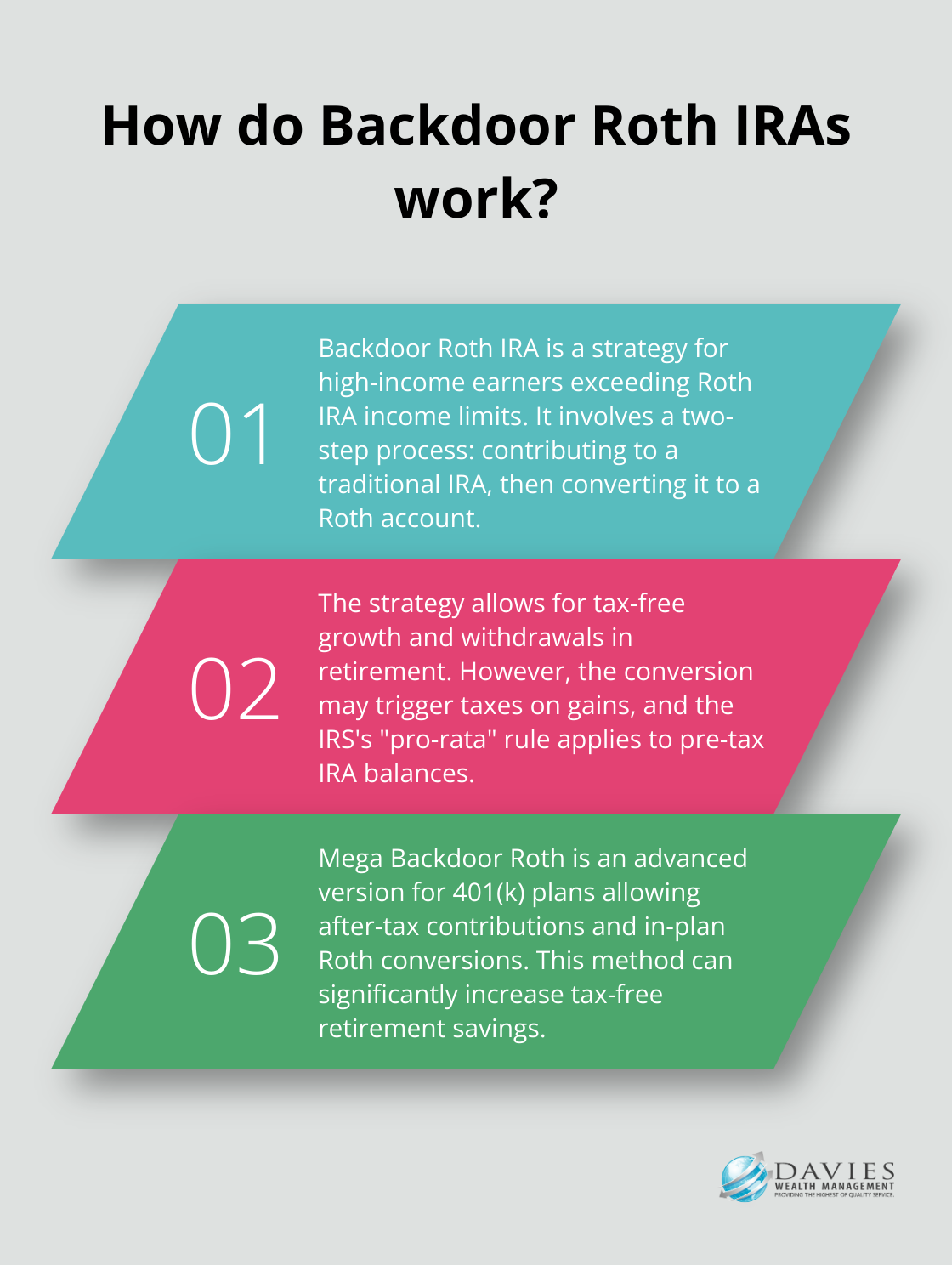

High-income earners who exceed Roth IRA income limits can use the Backdoor Roth IRA strategy to enjoy tax-free growth. This two-step strategy involves first making a contribution to a traditional IRA and then converting it to a Roth account. While the conversion may trigger taxes on any gains, the long-term benefits of tax-free withdrawals in retirement can prove substantial.

This strategy comes with potential pitfalls. The IRS’s “pro-rata” rule means you can’t simply convert only your non-deductible contributions if you have other pre-tax IRA balances. You must consult with a tax professional to navigate these complexities effectively.

Mega Backdoor Roth: Supercharging Your Retirement Savings

Those with access to a 401(k) plan that allows after-tax contributions and in-plan Roth conversions can use the Mega Backdoor Roth strategy. This method allows some people to save more in a Roth IRA and/or Roth 401(k) than they otherwise would be able to.

The key is to immediately convert these after-tax contributions to Roth, which minimizes taxable gains. This strategy can potentially add significantly to your tax-free retirement savings over time. However, it’s not available in all 401(k) plans, so check with your plan administrator first.

Cash Value Life Insurance: Tax-Deferred Growth with Added Benefits

Certain types of permanent life insurance policies (such as whole life or indexed universal life) offer a cash value component that grows tax-deferred. These policies can serve as a tax-efficient savings vehicle, especially for high-income earners who’ve maxed out other tax-advantaged accounts.

You can access the cash value tax-free through policy loans, which provides a source of tax-free income in retirement. However, these policies come with higher premiums and complexity. You must thoroughly understand the costs and benefits before implementing this strategy.

Charitable Remainder Trusts: Philanthropy with Tax Benefits

Philanthropically inclined individuals with appreciated assets can use Charitable Remainder Trusts (CRTs) to defer capital gains taxes while generating income. These irrevocable trusts allow you to donate assets to charity and draw annual income for life or for a specific time period. At the end of the term, the remaining assets go to your chosen charity.

This strategy can provide immediate tax deductions, ongoing income, and the satisfaction of supporting a cause you care about. However, CRTs are irrevocable, so you must consider them carefully before implementation.

Opportunity Zone Investments: Tax Breaks for Patient Investors

Investing in Qualified Opportunity Zones can defer and potentially reduce capital gains taxes. This program allows investors to defer taxes on capital gains by reinvesting them into designated economically distressed communities.

If you hold the investment for at least 10 years, any appreciation on the Opportunity Zone investment becomes tax-free. While this can offer significant tax benefits, these investments often carry higher risk and require a long-term commitment. You must conduct thorough due diligence before investing.

Final Thoughts

Tax deferral strategies offer powerful tools to optimize your financial future. These methods can significantly impact your long-term wealth accumulation, from traditional retirement accounts to advanced techniques like Backdoor Roth conversions. Each strategy has its own set of benefits and considerations, making it essential to approach tax planning with a personalized perspective.

Professional guidance becomes invaluable when implementing tax deferral strategies effectively. At Davies Wealth Management, we specialize in crafting tailored financial solutions that align with your specific needs and objectives. Our expertise includes tax-efficient strategies for both individuals and professional athletes, helping you navigate the complexities of tax planning.

Effective tax planning requires regular review and adjustment as your financial situation evolves and tax laws change. You can potentially reduce your current tax burden, maximize investment growth, and create a more secure financial future through a proactive approach to tax deferral. Tax deferral strategies play a vital role in achieving your financial aspirations, whether you save for retirement, plan for major life events, or build a legacy.

Leave a Reply