Retirement planning can be overwhelming, but it’s essential for securing your financial future. At Davies Wealth Management, we understand the importance of a well-structured retirement planning process.

This guide will walk you through the key steps to create a solid foundation for your retirement years, helping you navigate the complexities of financial planning with confidence.

Where Do You Stand Financially?

Taking Stock of Your Assets and Liabilities

The first step to build a solid retirement plan is to calculate your net worth. List all your assets (what you own) and subtract your liabilities (what you owe). Include everything from your home and vehicles to savings accounts and investments. Don’t forget to account for any outstanding debts, including mortgages, car loans, and credit card balances. This exercise provides a snapshot of your financial health and helps identify areas for improvement.

Understanding Your Cash Flow

Next, evaluate your income sources and review your expenses. Track your monthly income, including salary, bonuses, and any passive income streams. Then, analyze your spending habits over the past few months. This helps you understand where your money goes and identify potential areas to cut back or redirect funds towards retirement savings.

Assessing Your Current Savings and Investments

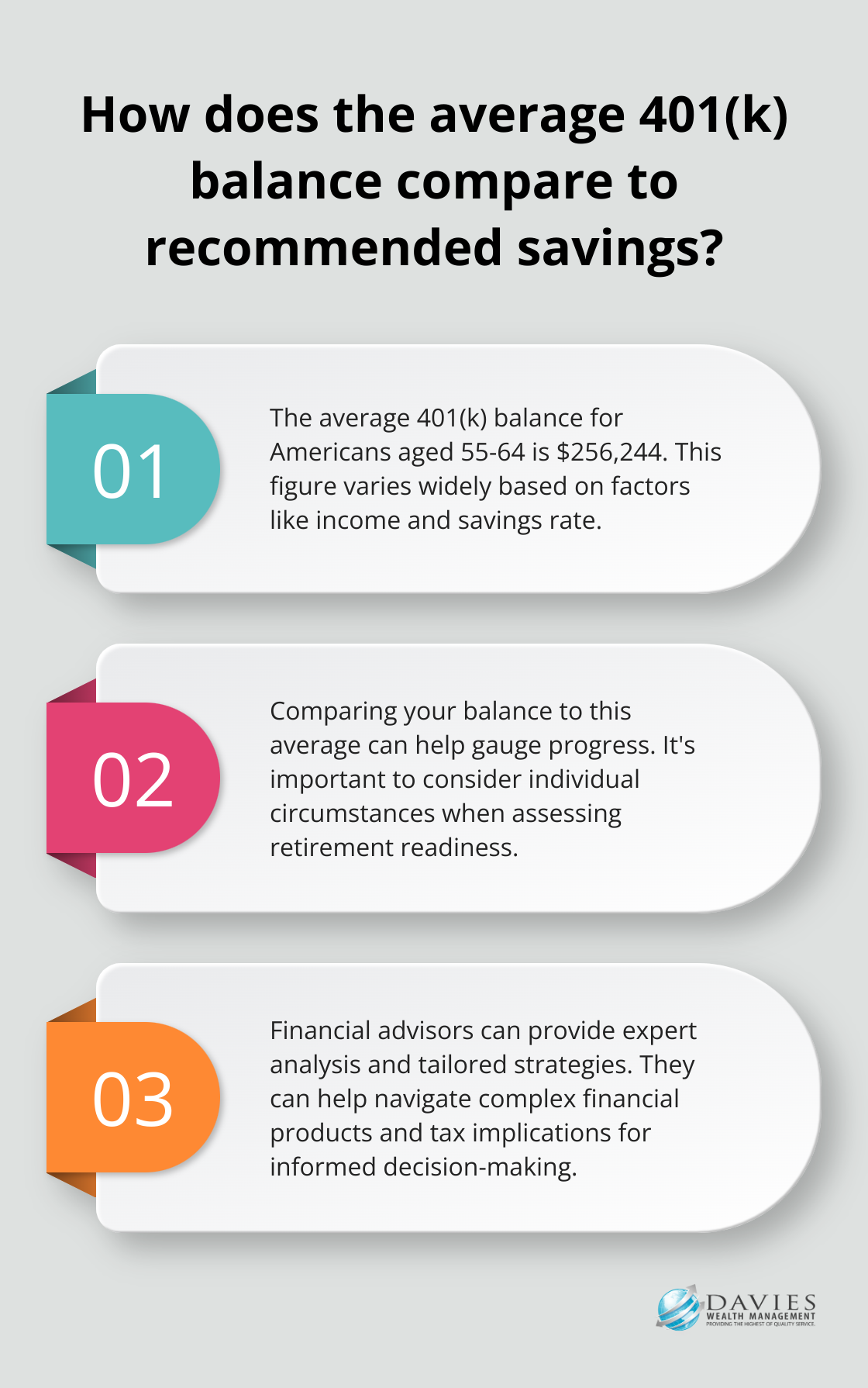

Take a close look at your existing savings and investment accounts. This includes retirement accounts like 401(k)s and IRAs, as well as any taxable investment accounts. A recent study revealed that the average 401(k) balance for Americans aged 55-64 was $256,244. However, this figure varies widely based on factors like income and savings rate. Understanding where you stand compared to these benchmarks can help you gauge your progress and adjust your savings strategy if needed.

Identifying Gaps and Opportunities

After you gather all this information, start to identify gaps in your financial plan and opportunities for improvement. You might discover that you’re not maximizing your employer’s 401(k) match (essentially leaving free money on the table). Or you might find that your investment portfolio isn’t properly diversified, exposing you to unnecessary risk.

Seeking Professional Guidance

While self-assessment is valuable, professional guidance can provide deeper insights. Financial advisors can offer expert analysis of your financial situation and help create a tailored retirement strategy. They can also help you navigate complex financial products and tax implications, ensuring you make informed decisions about your retirement planning.

As you move forward in your retirement planning journey, the next step is to set clear goals for your future. This involves envisioning your ideal retirement lifestyle and estimating the associated costs.

What’s Your Retirement Vision?

Paint Your Retirement Picture

To create an effective retirement plan, you must first envision your ideal retirement lifestyle. Ask yourself key questions: Where do you want to live? How will you spend your time? Do you plan to travel extensively or pursue new hobbies? Your answers will shape your retirement budget and savings targets. For example, if you dream of retiring in a coastal town, research the cost of living in your desired location. The Bureau of Labor Statistics reports that housing costs can vary significantly by region, with median home prices ranging from $230,000 in the Midwest to over $500,000 in the West.

Crunch the Numbers

After you have a clear vision, estimate your retirement expenses. The income replacement ratio is a measure of retirement income adequacy that analysts use to determine how much of your pre-retirement income you’ll need to maintain your standard of living. However, this figure can vary widely based on your specific plans. Break down your anticipated expenses into categories such as housing, food, healthcare, transportation, and leisure activities. Don’t forget to factor in potential one-time expenses (like home renovations or a dream vacation).

Account for the Future

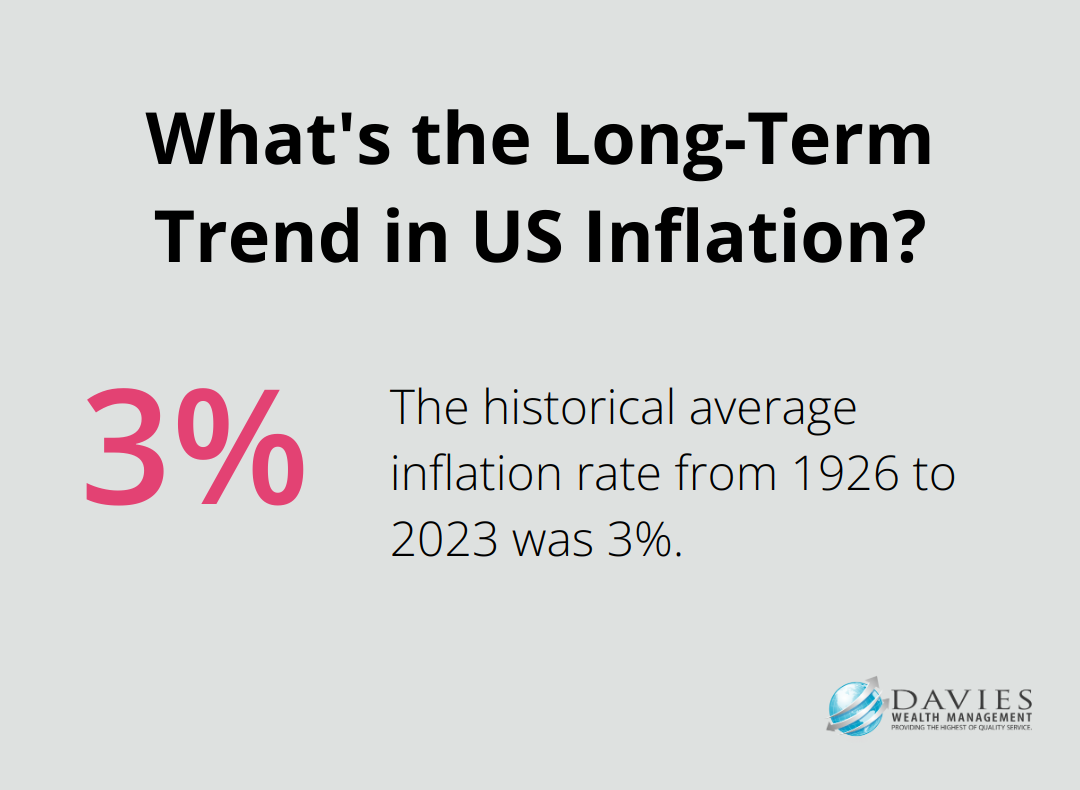

When you project your retirement expenses, consider the impact of inflation. The historical average inflation rate from 1926 to 2023 was 3%. This means that the purchasing power of your money will decrease over time. Use online inflation calculators to adjust your estimated expenses accordingly.

Address Healthcare: The Wild Card

Healthcare costs often represent a significant portion of retirement expenses and tend to increase with age. According to Fidelity research, the average American estimates healthcare costs in retirement will be about $75,000, which is less than half of Fidelity’s actual calculation. Consider purchasing long-term care insurance or set aside additional savings to cover these potential expenses.

Seek Professional Guidance

Creating a comprehensive retirement vision involves many complex considerations. Professional financial advisors specialize in helping clients navigate these intricacies. They can provide personalized projections and strategies to ensure your retirement vision becomes a reality, whether you’re a professional athlete with unique financial circumstances or an individual seeking a comfortable retirement.

With a clear retirement vision in place, the next step is to develop a comprehensive strategy to achieve your goals. This involves creating a diversified portfolio, maximizing retirement account contributions, and exploring tax-efficient strategies.

Building Your Retirement Fortress

Diversification: Your Financial Shield

Diversification protects your investments against market volatility. These strategies specifically use options to trade some equity portfolio volatility and upside for steady, volatility-reducing income. Spread your investments across various asset classes, including stocks, bonds, real estate, and potentially alternative investments.

Many financial advisors recommend a mix of low-cost index funds and carefully selected individual securities. This approach provides broad market exposure while allowing for strategic positioning in promising sectors or companies.

Maximizing Contributions: Fueling Your Retirement Engine

Take full advantage of tax-advantaged retirement accounts. In 2024, you can contribute up to $23,000 to a 401(k) if you’re under 50, and $30,500 if you’re 50 or older. For IRAs, the limits are $7,000 and $8,000, respectively. Self-employed individuals or small business owners should consider a SEP IRA or Solo 401(k), which often have higher contribution limits.

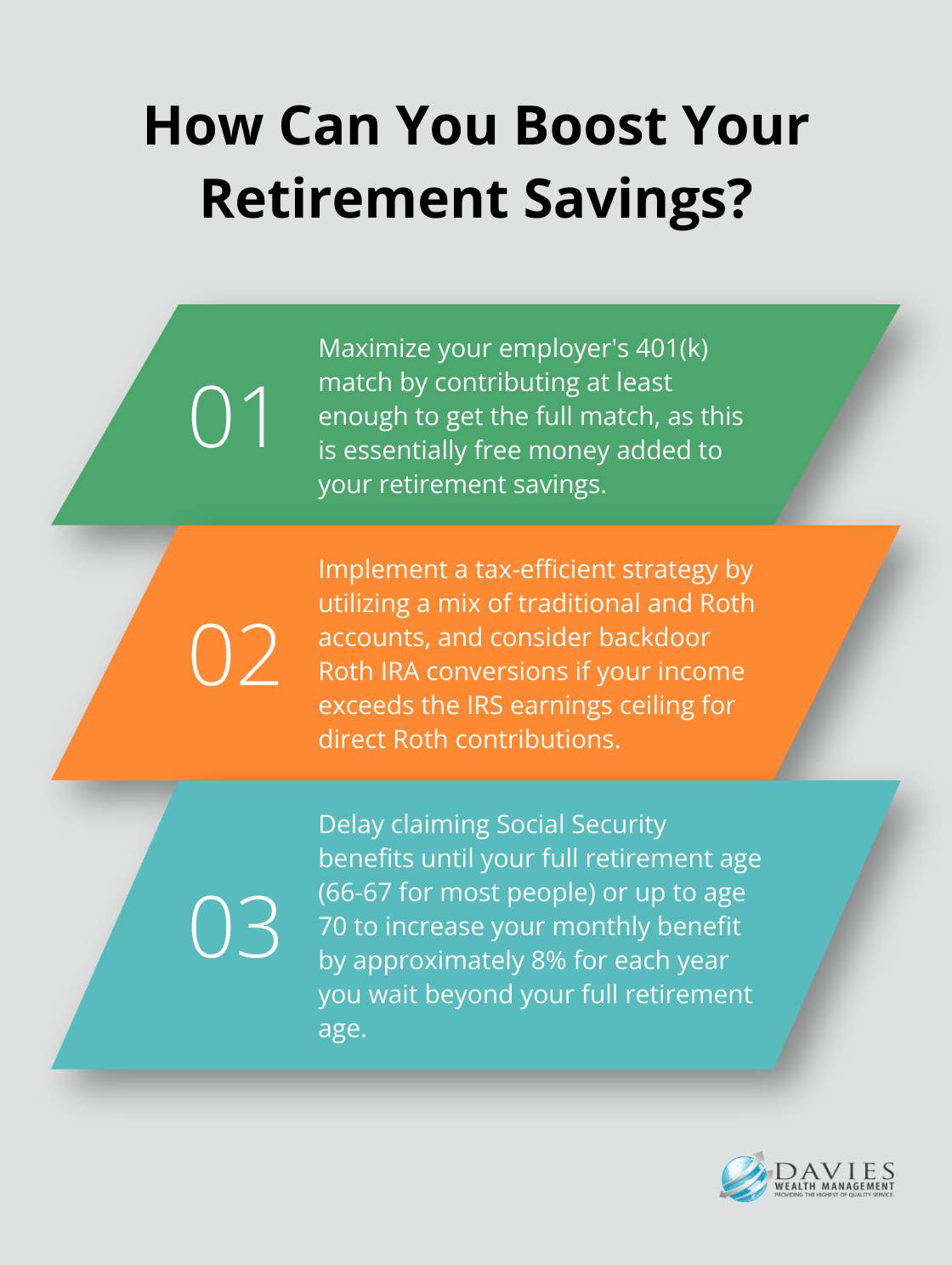

Don’t miss out on employer matching. If your employer offers a 401(k) match, contribute at least enough to get the full match. This essentially adds free money to your retirement savings.

Tax Efficiency: Keeping More of What You Earn

Tax planning maximizes your retirement savings. Consider a mix of traditional and Roth accounts to give yourself tax flexibility in retirement. High-income earners often benefit from backdoor Roth IRA conversions or mega backdoor Roth strategies, when appropriate. The backdoor Roth IRA strategy allows taxpayers to set up a Roth IRA retirement fund even if their income exceeds the IRS earnings ceiling for Roth contributions.

Tax-loss harvesting can also boost your returns. Strategically selling investments at a loss offsets capital gains and potentially reduces your tax bill.

Risk Management: Protecting Your Nest Egg

As retirement approaches, reassess your risk tolerance. While you don’t want to be too conservative and miss out on potential growth, you also can’t afford significant losses close to retirement.

Incorporate lower-risk investments like bonds or CDs into your portfolio. The traditional rule of thumb suggests subtracting your age from 100 to determine your stock allocation percentage. However, with increasing life expectancies, many financial advisors now recommend using 110 or even 120 as the starting point.

Insurance plays a vital role in risk management. Long-term care insurance can protect your assets from being depleted by healthcare costs. For a couple where both are age 55, the average combined annual premium is $2,080.

Navigating Social Security and Pensions

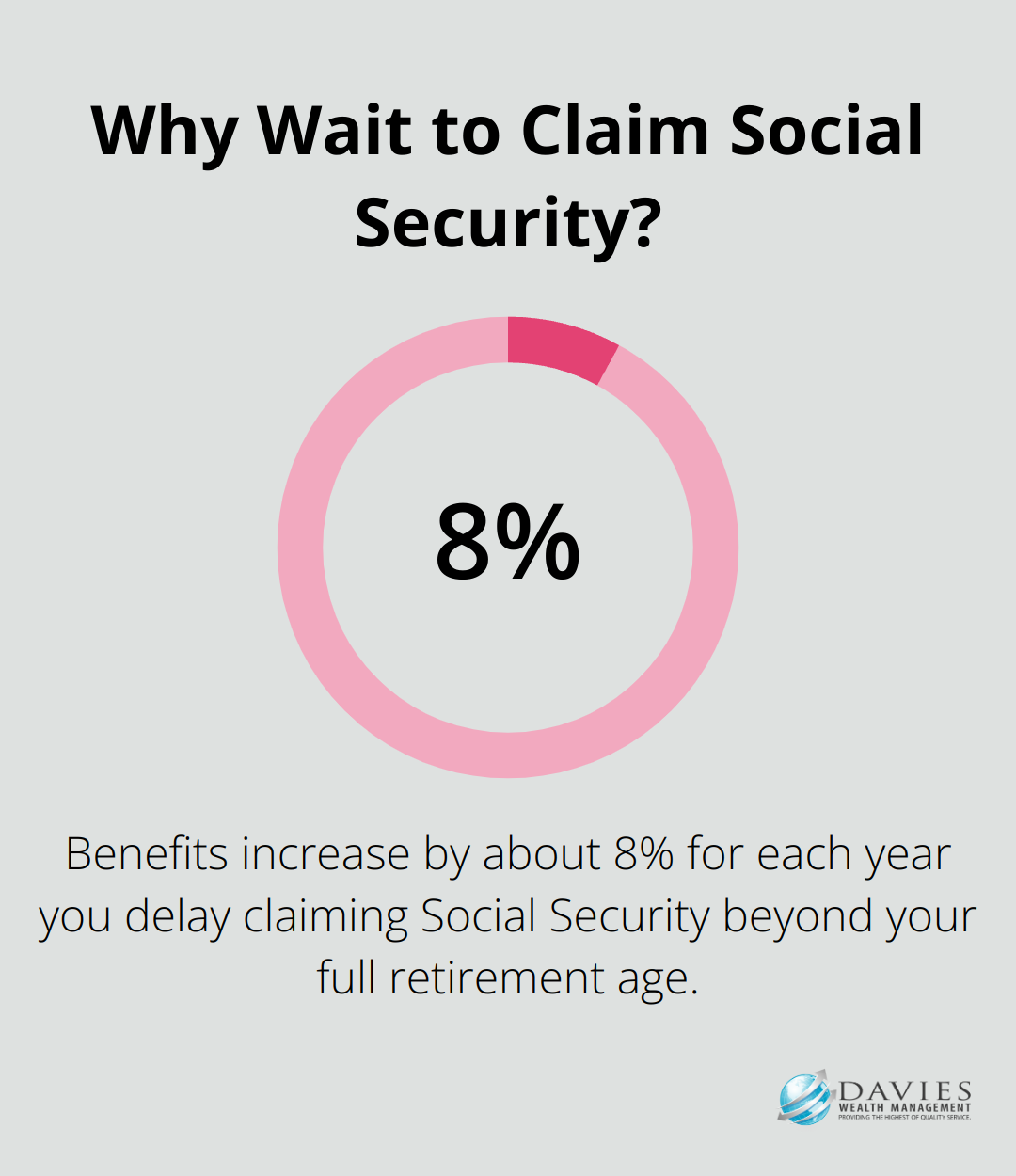

Timing impacts your Social Security benefits significantly. While you can start claiming benefits at 62, waiting until your full retirement age (66-67 for most people) or even up to age 70 can increase your monthly benefit. The Social Security Administration reports that benefits increase by about 8% for each year you delay claiming beyond your full retirement age.

For those with pensions, carefully consider your payout options. A single life annuity provides the highest monthly payment but ends when you die. A joint and survivor annuity provides a lower monthly payment but continues paying your spouse after your death.

Final Thoughts

A solid retirement planning process forms the foundation of a secure financial future. You must assess your current situation, set clear goals, and develop a comprehensive strategy to achieve a comfortable retirement. The earlier you start, the more time your money has to grow through compound interest, which can lead to a larger nest egg.

Commitment to your retirement plan will yield the best results. You should review and adjust your strategy as your life circumstances change (this might involve rebalancing your portfolio or increasing contributions as your income grows). Each individual’s situation is unique, and personalized strategies often produce the best outcomes.

At Davies Wealth Management, we create tailored retirement plans that address your specific needs and goals. Our team of experts can help you navigate the intricacies of retirement planning. Take control of your financial future today by implementing a robust retirement planning process.

Leave a Reply