At Davies Wealth Management, we understand the unique challenges federal employees face when planning for retirement. The federal retirement system offers a range of benefits and options that can significantly impact your financial future.

Retirement planning for federal employees requires a thorough understanding of FERS, TSP, and other crucial components. In this guide, we’ll break down these elements and provide practical strategies to help you maximize your retirement benefits.

Understanding Federal Retirement Benefits

Federal employees have access to a comprehensive retirement package that sets them apart from many private sector workers. This package includes several key components that work together to provide a secure financial future.

The Federal Employees Retirement System (FERS)

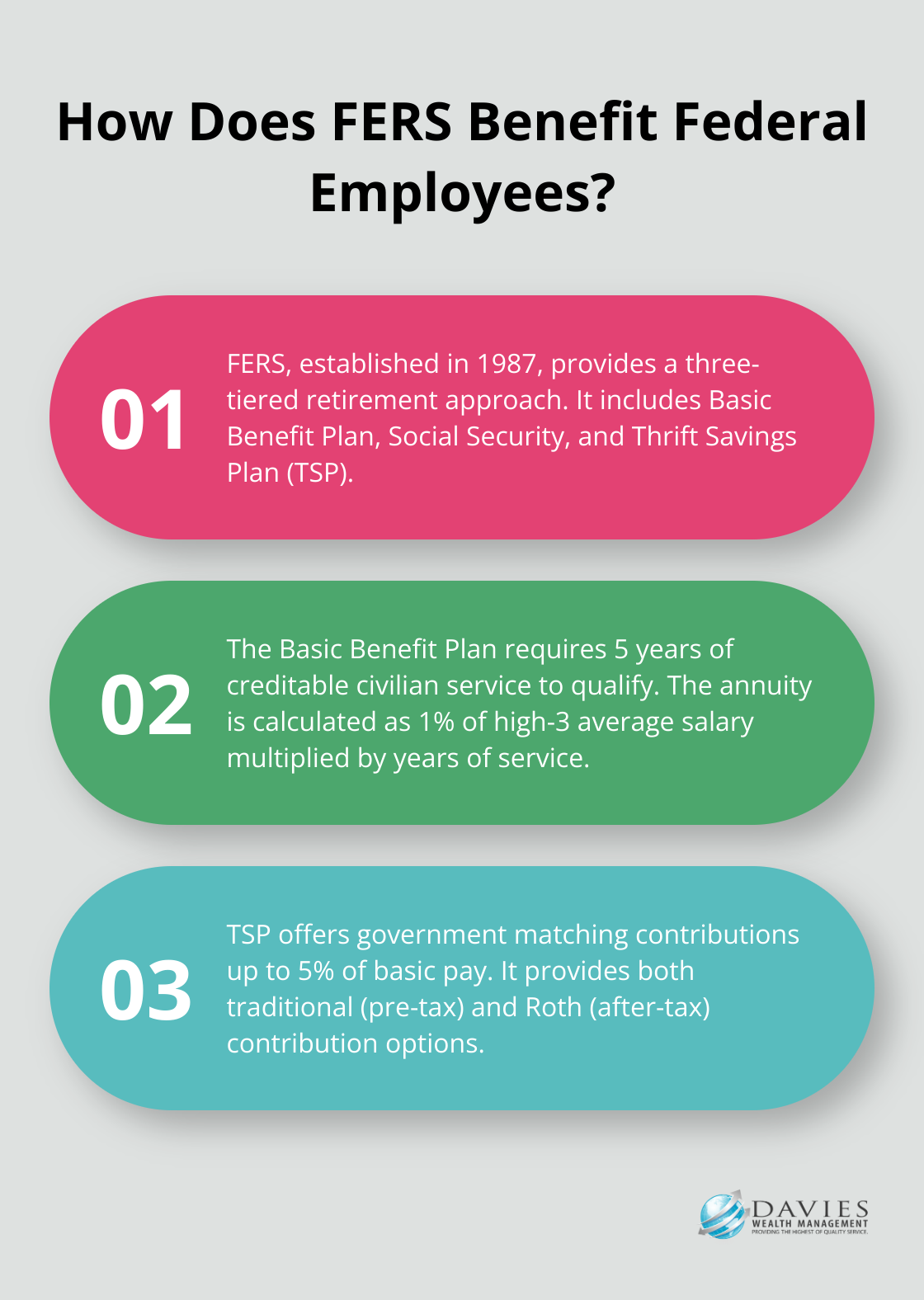

FERS, established in 1987, serves as the cornerstone of federal retirement benefits. It provides a three-tiered approach to retirement income:

- Basic Benefit Plan

- Social Security

- Thrift Savings Plan (TSP)

Each component plays a vital role in securing a comfortable retirement for federal workers.

Basic Benefit Plan Explained

The Basic Benefit Plan is a defined benefit pension plan. Your annuity calculation depends on your length of service and your highest three years of salary (known as the “high-3” average). For most employees, the formula is 1% of your high-3 average salary multiplied by your years of service.

To qualify for the Basic Benefit Plan, you must have at least 5 years of creditable civilian service. This vesting period ensures you’ll receive a pension even if you leave federal service before retirement age.

Social Security Benefits for Federal Employees

FERS fully integrates with Social Security, unlike its predecessor, the Civil Service Retirement System (CSRS). As a federal employee under FERS, you pay Social Security taxes and earn credits toward Social Security benefits, which can significantly supplement your retirement income.

However, it’s important to understand the potential impact of the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO). These provisions can affect your Social Security benefits if you get a pension from an employer who wasn’t required to withhold Social Security taxes. Factor these potential reductions into your retirement planning to avoid surprises later.

Thrift Savings Plan (TSP) Basics

The TSP is a defined contribution plan similar to a 401(k) in the private sector. It offers both traditional (pre-tax) and Roth (after-tax) contribution options, making it a powerful tool for building retirement savings.

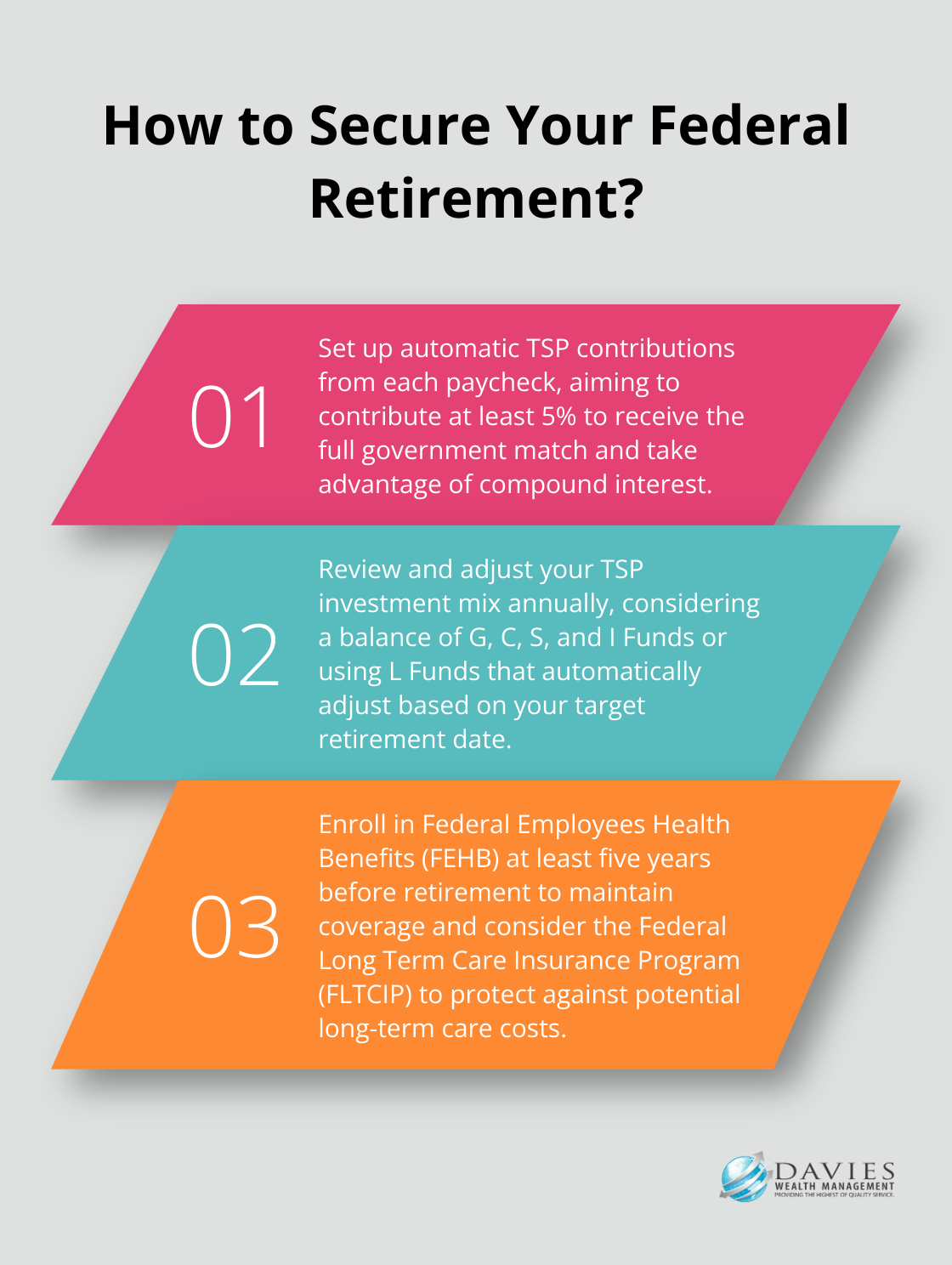

One of the most attractive features of the TSP is the government matching contributions. Your agency automatically contributes 1% of your basic pay and will match up to an additional 4% of your contributions. This means you can receive up to 5% in free money from your employer – a benefit you should maximize.

The TSP offers various investment options, including lifecycle funds that automatically adjust your asset allocation as you approach retirement. Understanding these options and aligning your investments with your risk tolerance and retirement timeline is essential for optimal results.

Proper utilization of these federal retirement benefits can lead to a secure and comfortable retirement. However, navigating these benefits can be complex. Professional guidance can help ensure you make the most of your federal retirement package and align it with your overall financial goals. As you consider your options, remember that Davies Wealth Management specializes in helping federal employees optimize their retirement strategies.

How to Maximize Your TSP Contributions

The Thrift Savings Plan (TSP) serves as a cornerstone for federal employees to build substantial retirement savings. Strategic use of the TSP can significantly impact retirement outcomes.

Early and Consistent Contributions

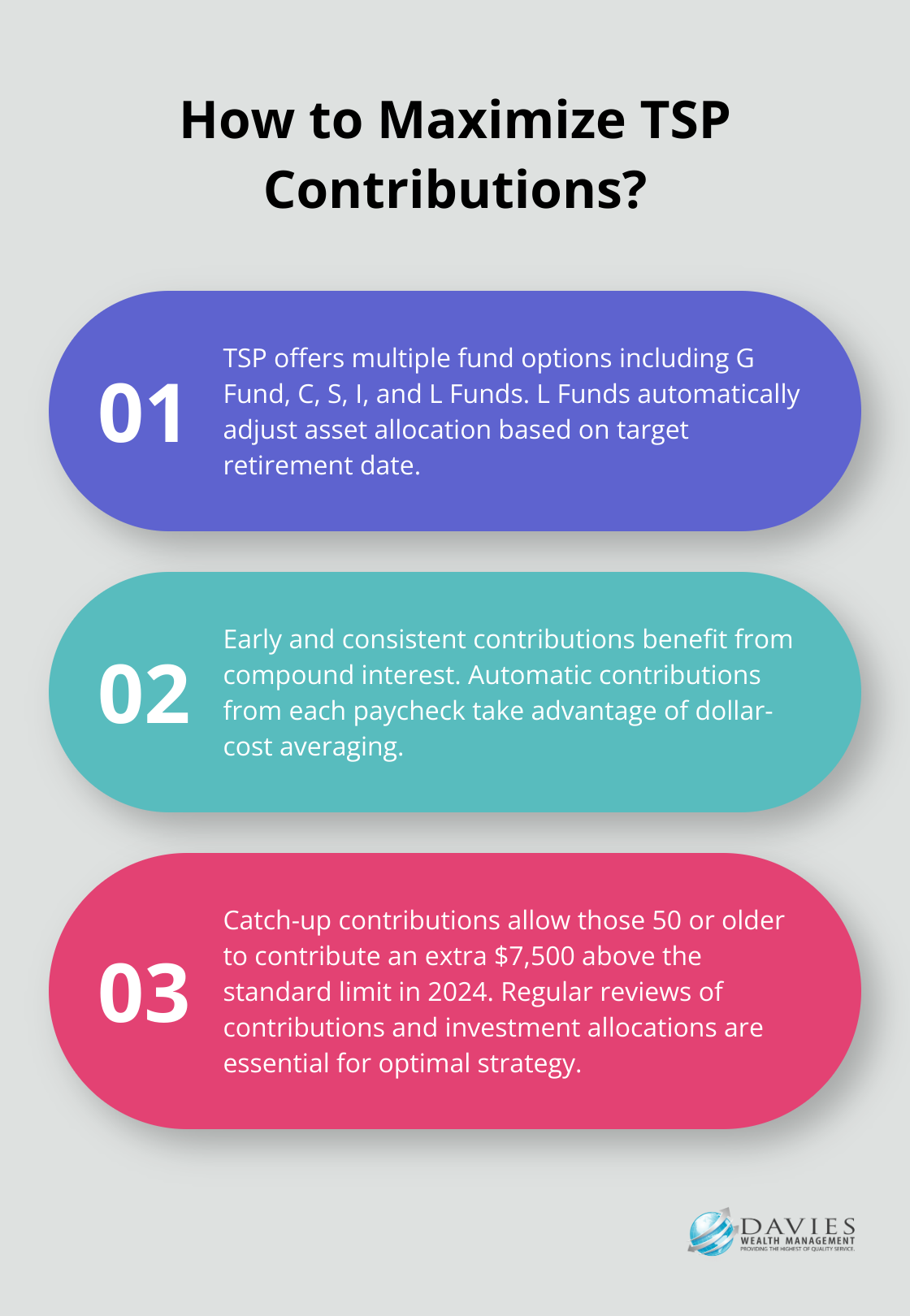

Time is your greatest ally for TSP contributions. The earlier you start, the more you benefit from compound interest. Set up automatic contributions from each paycheck. This approach ensures consistent saving and takes advantage of dollar-cost averaging, which reduces the impact of market volatility on your investments.

Optimal Investment Mix

The TSP offers several fund options, each with different risk and return profiles:

- G Fund: Provides stability but lower returns

- C, S, and I Funds: Offer higher potential returns with increased volatility

- L Funds: Automatically adjust asset allocation based on your target retirement date

For many federal employees, a mix of these funds can provide a balanced approach. The L Funds can be an excellent option for those who prefer a hands-off approach.

Catch-Up Contributions

If you’re 50 or older, you can make additional catch-up contributions to your TSP. In 2024, this allows you to contribute an extra $7,500 above the standard limit. This opportunity can boost your retirement savings in the years leading up to retirement.

Regular Review and Adjustment

Your TSP strategy should evolve with your changing financial situation and goals. Conduct regular reviews of your contributions and investment allocations. As you near retirement, you might want to shift to a more conservative mix to protect your accumulated wealth.

Understand Withdrawal Options

While retirement might seem distant, it’s essential to understand your TSP withdrawal options. The TSP offers various withdrawal methods, including lump-sum payments, monthly payments, and life annuities. Each option has different tax implications and flexibility. Familiarize yourself with these options to make informed decisions when the time comes.

As you navigate the complexities of TSP optimization, consider seeking professional guidance. A financial advisor can help you determine the right contribution level, investment mix, and overall strategy to align with your retirement goals and risk tolerance. The next chapter will explore additional retirement planning strategies that complement your TSP efforts and create a comprehensive retirement plan.

Beyond TSP: Comprehensive Retirement Strategies for Federal Employees

Securing Health Coverage in Retirement

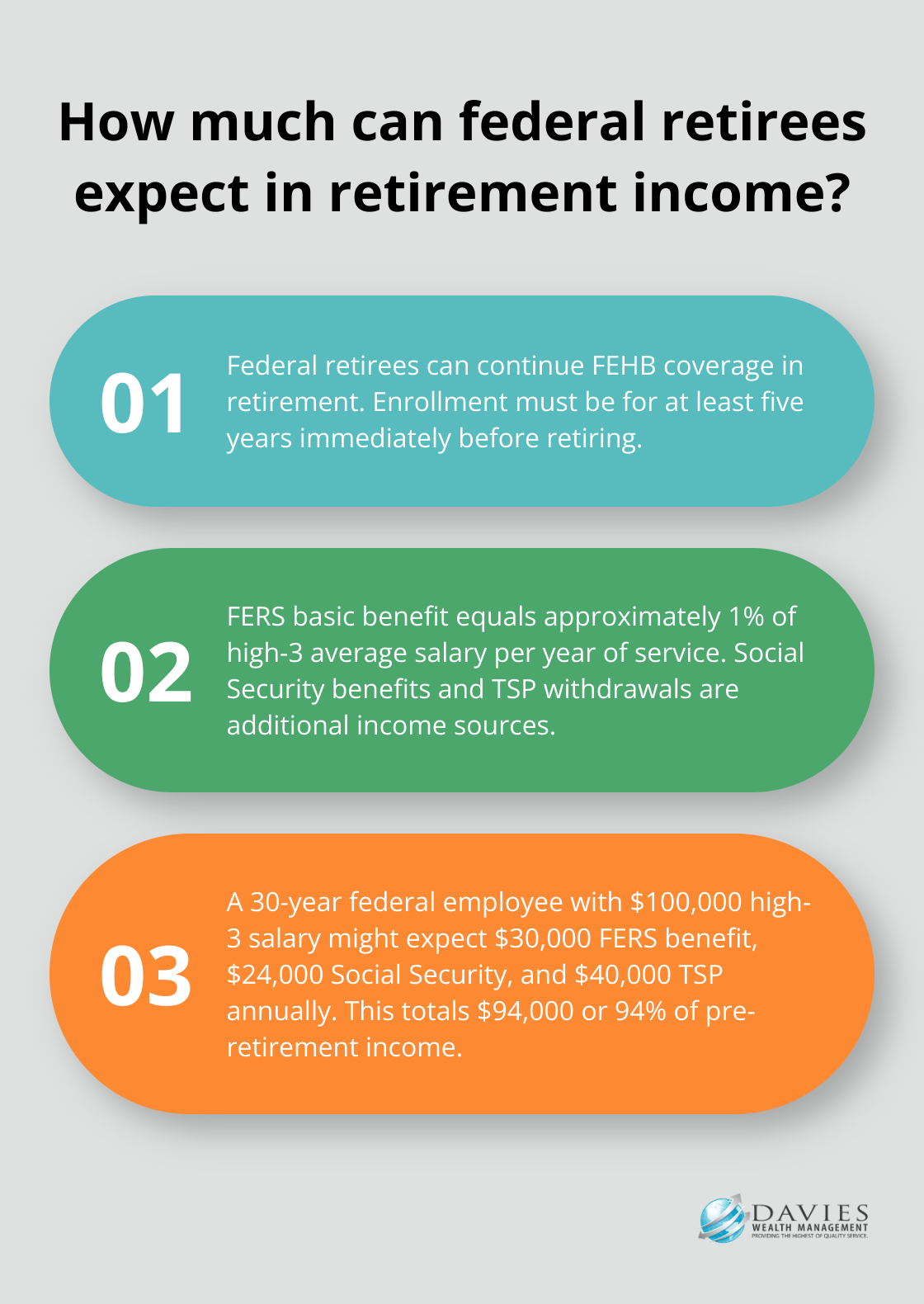

Federal employees can continue their Federal Employees Health Benefits (FEHB) coverage into retirement. To qualify, you must enroll in FEHB for at least five years immediately before retiring. This coverage provides substantial savings and peace of mind, as many private sector retirees struggle with high healthcare costs.

The Office of Personnel Management provides information on biweekly and monthly premiums, including the total premiums, the amount the government pays, and the change in the premiums for FEHB coverage.

Addressing Long-Term Care Needs

Long-term care is a critical consideration in retirement planning. The Federal Long Term Care Insurance Program (FLTCIP) provides long term care insurance to help pay for costs of care when enrollees need help with activities they perform every day. While premiums can be substantial, the potential costs of long-term care without insurance can devastate your finances.

According to Genworth’s 2021 Cost of Care Survey, the median annual cost for a private room in a nursing home was $108,405. This stark difference underscores the potential value of long-term care insurance.

Estate Planning for Federal Employees

Estate planning ensures your assets are distributed according to your wishes and minimizes tax burdens on your beneficiaries. As a federal employee, you have unique considerations, such as designating beneficiaries for your TSP account and federal life insurance.

The Federal Employees’ Group Life Insurance (FEGLI) program provides an important starting point for estate planning. Basic coverage equals your annual salary, rounded up to the next $1,000, plus $2,000. You can also elect additional coverage up to five times your salary. You should update your beneficiary designations and align them with your overall estate plan.

Calculating Your Retirement Income Needs

You must accurately estimate your retirement income needs for effective planning. A common rule suggests you try to reach 70-80% of your pre-retirement income. However, your specific needs may vary based on factors such as health, lifestyle, and retirement goals.

To calculate your federal retirement income, consider:

- Your FERS basic benefit (approximately 1% of your high-3 average salary per year of service)

- Social Security benefits (use the SSA’s online calculator for estimates)

- TSP withdrawals (consider the 4% rule as a starting point)

- Any additional savings or income sources

For example, a federal employee retiring with 30 years of service and a high-3 average salary of $100,000 might expect:

- FERS basic benefit: $30,000 per year

- Social Security: Approximately $24,000 per year (varies based on earnings history)

- TSP withdrawals: $40,000 per year (assuming a $1 million balance and 4% withdrawal rate)

This totals $94,000 per year, or 94% of pre-retirement income. However, individual circumstances can significantly impact these figures, making personalized planning essential.

Final Thoughts

The federal retirement system provides a comprehensive set of benefits for employees. FERS offers a three-tiered approach, while the TSP presents powerful savings potential. Federal employees can build a secure financial future through proactive planning and strategic decisions.

Retirement planning for federal employees extends beyond core benefits. Health insurance coverage, long-term care needs, and estate planning play vital roles in ensuring financial security throughout retirement years. Professional guidance can prove invaluable in navigating the complex landscape of federal retirement benefits.

Davies Wealth Management specializes in helping federal employees optimize their retirement strategies. Our team’s experience can assist you in preparing for current and future financial challenges. We encourage you to take control of your financial future and start planning today for a secure retirement that aligns with your goals.

✅ BOOK AN APPOINTMENT TODAY: https://davieswealth.tdwealth.net/appointment-page

===========================================================

SEE ALL OUR LATEST BLOG POSTS: https://tdwealth.net/articles

If you like the content, smash that like button! It tells YouTube you were here, and the Youtube algorithm will show the video to others who may be interested in content like this. So, please hit that LIKE button!

Don’t forget to SUBSCRIBE here: https://www.youtube.com/channel/UChmBYECKIzlEBFDDDBu-UIg

✅ Contact me: TDavies@TDWealth.Net

====== ===Get Our FREE GUIDES ==========

Retirement Income: The Transition into Retirement: https://davieswealth.tdwealth.net/retirement-income-transition-into-retirement

Beginner’s Guide to Investing Basics: https://davieswealth.tdwealth.net/investing-basics

✅ Want to learn more about Davies Wealth Management, follow us here!

Website:

Podcast:

Social Media:

https://www.facebook.com/DaviesWealthManagement

https://twitter.com/TDWealthNet

https://www.linkedin.com/in/daviesrthomas

https://www.youtube.com/c/TdwealthNetWealthManagement

Lat and Long

27.17404889406371, -80.24410438798957

Davies Wealth Management

684 SE Monterey Road

Stuart, FL 34994

772-210-4031

#Retirement #FinancialPlanning #wealthmanagement

DISCLAIMER

Davies Wealth Management makes content available as a service to its clients and other visitors, to be used for informational purposes only. Davies Wealth Management provides accurate and timely information, however you should always consult with a retirement, tax, or legal professionals prior to taking any action.

Leave a Reply