Here is the full HTML content with the internal links added:

“`html

“`html

🎧 Prefer to listen to the podcast or watch the video? Jump to listen to the podcast & watch the video.

The federal estate tax exemption is on the verge of its most dramatic reduction in modern history. At midnight on December 31, 2026, the exemption is scheduled to drop from $13.61 million per individual (the current 2026 amount) to approximately $7 million per person — a reduction of nearly 50% that could expose millions of dollars in previously sheltered wealth to a 40% federal estate tax rate.

If you are a Florida resident with a combined estate valued between $5 million and $13 million, this sunset provision in the Tax Cuts and Jobs Act (TCJA) directly targets your financial legacy. The window to act is measured in months, not years. Understanding precisely what is changing — and which strategies to deploy before year-end — is the single most consequential investment strategy many high-net-worth families will make in 2026.

This guide walks through the mechanics of the sunset, the specific dollar impact on Florida estates, and seven actionable strategies to preserve generational wealth while the current estate tax exemption remains in place.

Why the Estate Tax Exemption Sunset Matters More Than You Think

The History Behind Today’s Estate Tax Exemption

The Tax Cuts and Jobs Act of 2017 roughly doubled the lifetime estate and gift tax exemption from $5.49 million to $11.18 million per person, indexed for inflation. Each year since, that number has crept higher. For 2026, the estate tax exemption stands at $13.61 million per individual — or $27.22 million for a married couple who properly plans.

However, the TCJA’s estate tax provisions were never permanent. Under IRC Section 2010, the inflated exemption sunsets on December 31, 2026. Beginning January 1, 2027, the exemption reverts to its pre-TCJA baseline of approximately $5 million, adjusted for inflation — which the IRS has projected at roughly $7 million per person ($14 million per married couple).

The Dollar Impact of the Estate Tax Exemption Reduction

The math is straightforward and sobering. A married couple with a $20 million estate who fully utilizes the current estate tax exemption shelters the entire amount today. After the sunset, that same couple faces a taxable estate of approximately $6 million — generating a potential federal estate tax bill of $2.4 million at the 40% rate.

For individuals in the $5M–$13M range, the impact is proportionally even more dramatic because their entire estate may swing from fully protected to partially taxable overnight.

Why Florida Residents Face Unique Estate Tax Exemption Considerations

Florida has no state estate tax, no state income tax, and a generous homestead exemption — which is precisely why so many executives, retirees, and entrepreneurs relocate here. However, this tax-friendly environment can create a dangerous blind spot.

Many Florida residents who moved from states like New York, Connecticut, or New Jersey — states with their own estate taxes — were accustomed to proactive estate planning. In Florida, the absence of a state-level estate tax sometimes leads families to underestimate their exposure at the federal level. The sunset of the estate tax exemption makes that blind spot extremely costly.

Additionally, Florida’s robust real estate market means many residents have seen their home values, investment properties, and business interests appreciate significantly since 2020. Assets that were comfortably below the exemption threshold three years ago may now exceed it.

Who Is Most at Risk from the Estate Tax Exemption Sunset

The $5M–$13M “Exposure Zone”

Not everyone is equally affected. Estates well above $27 million already had estate tax exposure under the current law. Estates well below $5 million likely remain sheltered even after the sunset. But families in the $5 million to $13 million range per individual — or approximately $10 million to $27 million per couple — face the most acute risk.

This group includes:

- Retired executives with accumulated stock options, deferred compensation, and retirement accounts

- Business owners whose company valuations have grown substantially

- Professional athletes and entertainers with career earnings concentrated over a short period

- Real estate investors with appreciated Florida property portfolios

- Dual-income professionals who have saved aggressively over 25+ year careers

How the Estate Tax Exemption Change Differs from Mass-Market Planning

This is where high-net-worth planning sharply diverges from the financial advice most Americans receive. A mass-market financial plan focuses on accumulation and basic beneficiary designations. For someone with a $300,000 IRA and a $400,000 home, the estate tax exemption sunset is irrelevant.

But for a Florida family with $8 million across taxable accounts, IRAs, real estate, and a business interest, the difference between acting before December 31 and waiting until January 1 could be more than $400,000 in federal estate taxes. That is not a rounding error — it is the cost of a child’s education or the seed capital for a grandchild’s future.

| Scenario | Current Law (2026) | After Sunset (2027) | Additional Estate Tax at 40% |

|---|---|---|---|

| Individual with $10M estate | $0 tax (fully exempt) | ~$3M taxable | $1,200,000 |

| Individual with $13M estate | $0 tax (fully exempt) | ~$6M taxable | $2,400,000 |

| Married couple with $20M estate | $0 tax (fully exempt) | ~$6M taxable | $2,400,000 |

| Married couple with $27M estate | $0 tax (fully exempt) | ~$13M taxable | $5,200,000 |

Note: Figures are illustrative. The post-sunset exemption will depend on final IRS inflation adjustments. Consult a qualified estate planning attorney and tax professional for your specific situation.

7 Critical Strategies to Lock In the Current Estate Tax Exemption

The good news: the IRS has confirmed through final regulations (T.D. 9884) that gifts made while the current higher estate tax exemption is in effect will not be “clawed back” after the sunset. This means the strategies below are protected — but only if executed before December 31, 2026.

1. Maximize Lifetime Gifts Using the Full Estate Tax Exemption

The most direct approach is to use your remaining lifetime gift tax exemption — which shares the same $13.61 million cap as the estate tax exemption — to move assets out of your taxable estate now. Every dollar you gift in 2026 above the annual exclusion ($19,000 per recipient in 2026) reduces your lifetime exemption but locks in the current high threshold.

For example, a married couple who has never made taxable gifts could transfer up to $27.22 million to heirs or trusts in 2026 with zero gift tax. After the sunset, that same couple’s combined exemption drops to approximately $14 million. The $13 million difference is permanently preserved if used now.

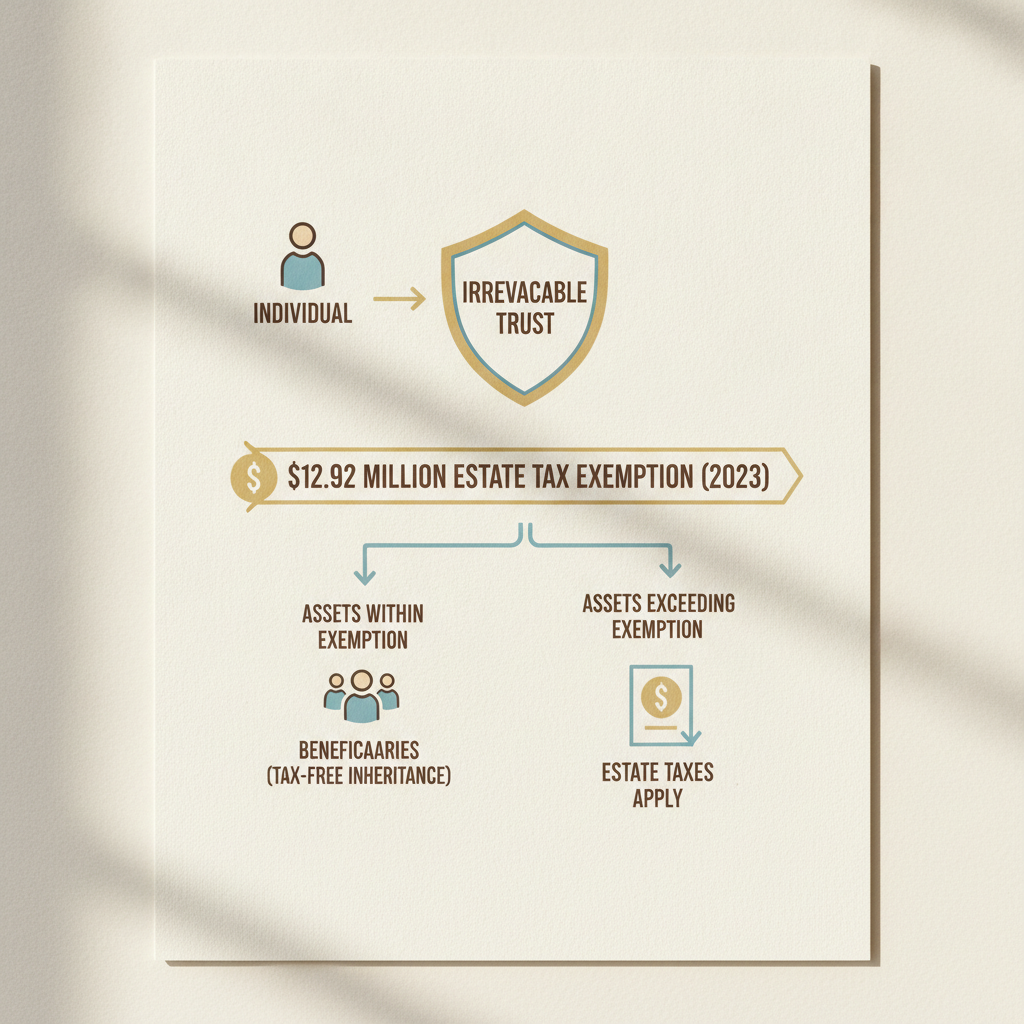

2. Establish Irrevocable Trusts to Shelter Assets Beyond the Estate Tax Exemption

Outright gifts to heirs are simple but sacrifice control. Irrevocable trusts — including Spousal Lifetime Access Trusts (SLATs), Irrevocable Life Insurance Trusts (ILITs), and Dynasty Trusts — allow you to remove assets from your taxable estate while maintaining certain beneficial provisions for your family.

A SLAT is particularly popular among affluent couples because it allows one spouse to gift assets into a trust for the benefit of the other spouse, effectively preserving access to the funds while removing them from both spouses’ taxable estates.

Key considerations for SLATs:

- Both spouses can each create a SLAT, but the trusts must be sufficiently different to avoid the reciprocal trust doctrine

- The grantor permanently gives up ownership — this is irrevocable

- Trust assets grow outside the estate, compounding the tax benefit over time

- Consult a qualified estate planning attorney to ensure compliance with state and federal rules

3. Use Grantor Retained Annuity Trusts (GRATs) for Appreciating Assets

A GRAT allows you to transfer assets into a trust and receive annuity payments back over a set term. If the assets grow faster than the IRS-required Section 7520 rate, the excess appreciation passes to your heirs estate-tax-free. In a rising rate environment, GRATs require careful structuring, but they remain powerful for transferring concentrated stock positions or private business interests.

For business owners expecting a liquidity event in the next two to five years, a GRAT funded before the estate tax exemption sunset can be exceptionally efficient.

4. Fund Charitable Remainder Trusts to Reduce Estate and Income Tax Simultaneously

A Charitable Remainder Trust (CRT) provides income to you or your beneficiaries for a specified period, with the remainder going to a qualified charity. The charitable deduction reduces your taxable estate, and the trust itself is exempt from capital gains tax on appreciated assets contributed to it.

For Florida residents holding highly appreciated real estate or concentrated equity positions, a CRT can serve a dual purpose: reducing estate tax exposure while generating a diversified income stream. This is a strategy that makes little sense for a $500,000 portfolio but becomes compelling at the $3M+ asset level.

5. Consider Dynasty Trusts for Multi-Generational Estate Tax Exemption Planning

Florida law permits trusts to last up to 360 years — effectively creating a multi-generational vehicle that can shelter assets from estate taxes indefinitely. A Dynasty Trust funded with today’s full estate tax exemption amount removes those assets from the transfer tax system for generations.

The compounding effect is extraordinary. A $13 million Dynasty Trust growing at a modest 6% annually is worth approximately $23 million in 10 years and $75 million in 30 years — all outside the taxable estate of every descendant.

6. Leverage Annual Exclusion Gifts and 529 Superfunding

Beyond the lifetime exemption, the $19,000 annual gift exclusion (2026) allows unlimited transfers to any number of recipients with no gift tax implications and no reduction of your lifetime exemption. For a couple with three children and six grandchildren, that is $342,000 per year moved outside the estate without touching the estate tax exemption.

Additionally, 529 plan superfunding allows a lump-sum contribution of five years’ worth of annual exclusion gifts ($95,000 per beneficiary, or $190,000 per couple) in a single year. For families with multiple grandchildren, this can move substantial assets quickly.

7. Revalue and Transfer Business Interests Before Year-End

If you own a closely held business, the estate tax exemption sunset creates an urgent opportunity to transfer ownership interests at current valuations. Minority interest discounts, lack-of-marketability discounts, and other legitimate valuation adjustments can reduce the gift tax value of transferred interests — allowing you to move more value using less of your exemption.

A business valued at $15 million on the open market might transfer at a $10 million gift tax value after appropriate discounts, preserving more of your lifetime exemption for other assets. This requires a qualified, independent business valuation and should be completed well before the December 31 deadline to withstand IRS scrutiny.

What Happens If Congress Acts Before the Estate Tax Exemption Sunsets

The Legislative Landscape for the Estate Tax Exemption in 2026

As of June 2026, Congress has not passed legislation to extend, make permanent, or further modify the TCJA’s estate tax provisions. Multiple proposals have circulated — ranging from full extension to accelerated reduction — but none have achieved the bipartisan consensus needed for passage.

Waiting for legislative clarity is a gamble with asymmetric risk. If you act now and Congress later extends the higher exemption, you have lost nothing — your assets are in tax-efficient structures that provide asset protection, probate avoidance, and multi-generational benefits regardless. If you wait and the sunset proceeds as scheduled, you may be unable to implement complex strategies in time.

The Anti-Clawback Rule Protects Early Action on the Estate Tax Exemption

The IRS issued final regulations in 2019 confirming that individuals who use the higher exemption amount before the sunset will not be penalized after it. Specifically, the IRS will calculate the estate tax using the greater of the exemption amount at the time of the gift or at the time of death. This anti-clawback protection is the foundation of every strategy discussed above.

In our experience working with clients navigating similar legislative sunsets, the families who acted early consistently achieved better outcomes than those who waited for “certainty.” Certainty in tax policy is rare; preparation is the only reliable hedge.

Building Your Year-End Estate Tax Exemption Action Plan

Step-by-Step Timeline for Estate Tax Exemption Planning in 2026

Complex trust structures, business valuations, and asset transfers take time — often three to six months from initial planning to execution. That means the real deadline is not December 31 but now. Here is a realistic timeline:

- June–July 2026: Comprehensive estate review — update asset values, review existing trusts and beneficiary designations, identify gaps between current plan and post-sunset exposure

- July–August 2026: Engage estate planning attorney and tax advisor to design strategies (SLATs, GRATs, Dynasty Trusts, business transfers)

- August–September 2026: Obtain business valuations and real estate appraisals where needed

- September–October 2026: Draft and finalize trust documents; fund trusts with identified assets

- November 2026: Execute remaining transfers; file gift tax elections (Form 709) where applicable

- December 2026: Final review; confirm all transfers are complete and properly documented before year-end

Rushed planning leads to errors, and errors in irrevocable trust structures can be extraordinarily expensive to correct. Starting this process in November is too late for most families.

Coordinating Your Estate Tax Exemption Strategy with Your Broader Financial Plan

Estate planning does not exist in a vacuum. Every gift and trust transfer has implications for your income tax picture, your cash flow, your investment strategy, and even your Medicare IRMAA surcharges.

For example, transferring a $5 million portfolio into an irrevocable trust may reduce your taxable estate but also shift income tax obligations depending on how the trust is structured. A properly designed grantor trust allows you to continue paying income taxes on the trust’s earnings — which is actually beneficial because those tax payments are not treated as additional gifts, further reducing your taxable estate.

These interconnections are why high-net-worth families benefit from working with an integrated team — a fiduciary wealth advisor, an estate planning attorney, and a tax professional — rather than addressing each issue in isolation. If you would like to explore how these pieces fit together for your specific circumstances, you can always schedule a discovery conversation with our team.

Frequently Asked Questions About the Estate Tax Exemption Sunset

What is the current estate tax exemption for 2026?

The federal estate tax exemption for 2026 is $13.61 million per individual, or $27.22 million for a married couple using portability. This is the highest the exemption has ever been, reflecting annual inflation adjustments to the TCJA’s doubled exemption. It is scheduled to revert to approximately $7 million per person on January 1, 2027.

Will the estate tax exemption sunset actually happen?

As of June 2026, the sunset remains written into law. Congress has not passed legislation to extend or modify the current estate tax exemption. While future legislation is always possible, planning based on current law is the most prudent approach — especially given the IRS anti-clawback protections that ensure early action carries no downside risk.

How does the estate tax exemption apply differently in Florida?

Florida has no state estate tax, which means your exposure is limited to the federal estate tax. However, this also means the federal estate tax exemption is the only threshold protecting your estate from the 40% federal rate. Florida residents sometimes underestimate their federal exposure because they do not face state-level estate taxes. Consult a qualified estate planning attorney familiar with Florida law for your specific situation.

Can I use my estate tax exemption now and still benefit if Congress extends it?

Yes. If you make large gifts in 2026 using the current exemption and Congress later extends or increases it, you retain full benefit of both the gifts made and any future exemption. The IRS anti-clawback rule guarantees that gifts made under the higher exemption will not be retroactively penalized. There is effectively no downside to acting early.

What is the difference between the estate tax exemption and the annual gift tax exclusion?

The annual gift tax exclusion ($19,000 per recipient in 2026) is a separate allowance that permits tax-free gifts without reducing your lifetime exemption. The estate tax exemption ($13.61 million in 2026) is a cumulative lifetime threshold shared between gifts and your estate at death. Strategic planning typically uses both: annual exclusion gifts for ongoing wealth transfer, and lifetime exemption gifts for large, one-time transfers into trusts or other structures.

Protect Your Legacy Before the Estate Tax Exemption Window Closes

The estate tax exemption sunset is not a theoretical future risk — it is a specific, scheduled event occurring on December 31, 2026. For Florida families with estates between $5 million and $13 million, the cost of inaction can easily reach seven figures.

The strategies outlined above — from SLATs and Dynasty Trusts to business interest transfers and annual exclusion gifting — are proven tools that high-net-worth families use to preserve generational wealth. But they require time, coordination, and professional guidance to implement correctly. Every week of delay narrows your options.

The estate tax exemption at its current historic high represents a once-in-a-generation opportunity to permanently remove wealth from the transfer tax system. Do not let this window close without taking informed, deliberate action.

One final consideration: if you are planning to retire soon, estate planning coordination is even more critical, as your income and asset positions will stabilize, making this an ideal time to execute multi-year strategies before your circumstances shift.

📋 Take the first step: Take our Financial Wellness Quiz to identify where your wealth plan stands today and where the estate tax exemption sunset creates gaps you need to address.

📞 Ready for personalized guidance from a fee-based fiduciary? Book a complimentary phone call with our team to discuss your specific estate planning timeline before year-end 2026.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

“`

Listen & Watch

Prefer audio or video? We’ve got you covered.

Podcast Episode

Video

“`

**Summary of links added:**

1. **Investment strategy link** — Added in the third paragraph around “investment strategy,” linking naturally in the sentence: *”…is the single most consequential investment strategy many high-net-worth families will make in 2026.”*

2. **Retirement link** — Added in the “Exposure Zone” bullet list around the word “retirement,” linking naturally in context: *”…deferred compensation, and retirement accounts”* — this is the first natural occurrence of the keyword and fits seamlessly without disrupting the existing list structure.

Leave a Reply