“`html

At Davies Wealth Management, we understand the challenges high earners face when it comes to managing their tax burden. High income tax strategies are essential for maximizing wealth and minimizing tax liabilities.

In this blog post, we’ll explore effective techniques to help you navigate the complexities of high-income taxation. From maximizing retirement contributions to leveraging advanced tax planning strategies, we’ll provide actionable insights to optimize your financial situation.

Understanding High Income Tax Brackets

Defining High Income Tax Brackets

High income tax brackets represent the upper tiers of the progressive tax system in the United States. These brackets apply to individuals and couples who earn substantial incomes, subjecting them to higher tax rates on portions of their earnings.

For 2025, the highest federal income tax bracket stands at 37% for individuals with taxable income over $578,125 and married couples filing jointly with income exceeding $693,750. The Internal Revenue Service (IRS) adjusts these figures annually to account for inflation.

The Substantial Impact on Tax Liability

High earners face a significant tax burden. To illustrate, a single filer with $1 million in taxable income would owe a substantial amount in federal income taxes for 2025. This figure excludes state taxes, which can add considerably to the total liability (especially in high-tax states like California or New York).

It’s critical to distinguish between taxable income and gross income. Taxable income represents the amount left after all deductions and credits apply. This distinction opens up opportunities for effective tax planning strategies.

Marginal vs. Effective Tax Rates: A Key Distinction

When discussing high income tax brackets, understanding the difference between marginal and effective tax rates proves essential:

- Marginal tax rate: The rate paid on the last dollar of income

- Effective tax rate: The average rate paid on all income

For example, a married couple with $800,000 in taxable income falls into the 37% bracket. However, their effective tax rate would be lower because not all of their income faces taxation at the highest rate.

Navigating High Income Tax Brackets

Comprehension of these brackets serves as the first step. High earners need comprehensive strategies to manage their tax liabilities effectively. These strategies might include:

- Maximizing retirement contributions

- Implementing strategic charitable giving

- Executing careful investment planning

Professional athletes often encounter unique tax challenges due to their high but potentially short-term earnings. Specialized financial advisors can help with tax planning, ensuring that athletes understand tax implications on their earnings while finding strategies to minimize their tax burden.

As we move forward, let’s explore specific tax reduction strategies that high earners can employ to optimize their financial situations and minimize their tax burdens.

Smart Tax Moves for High Earners

Maximize Retirement Account Contributions

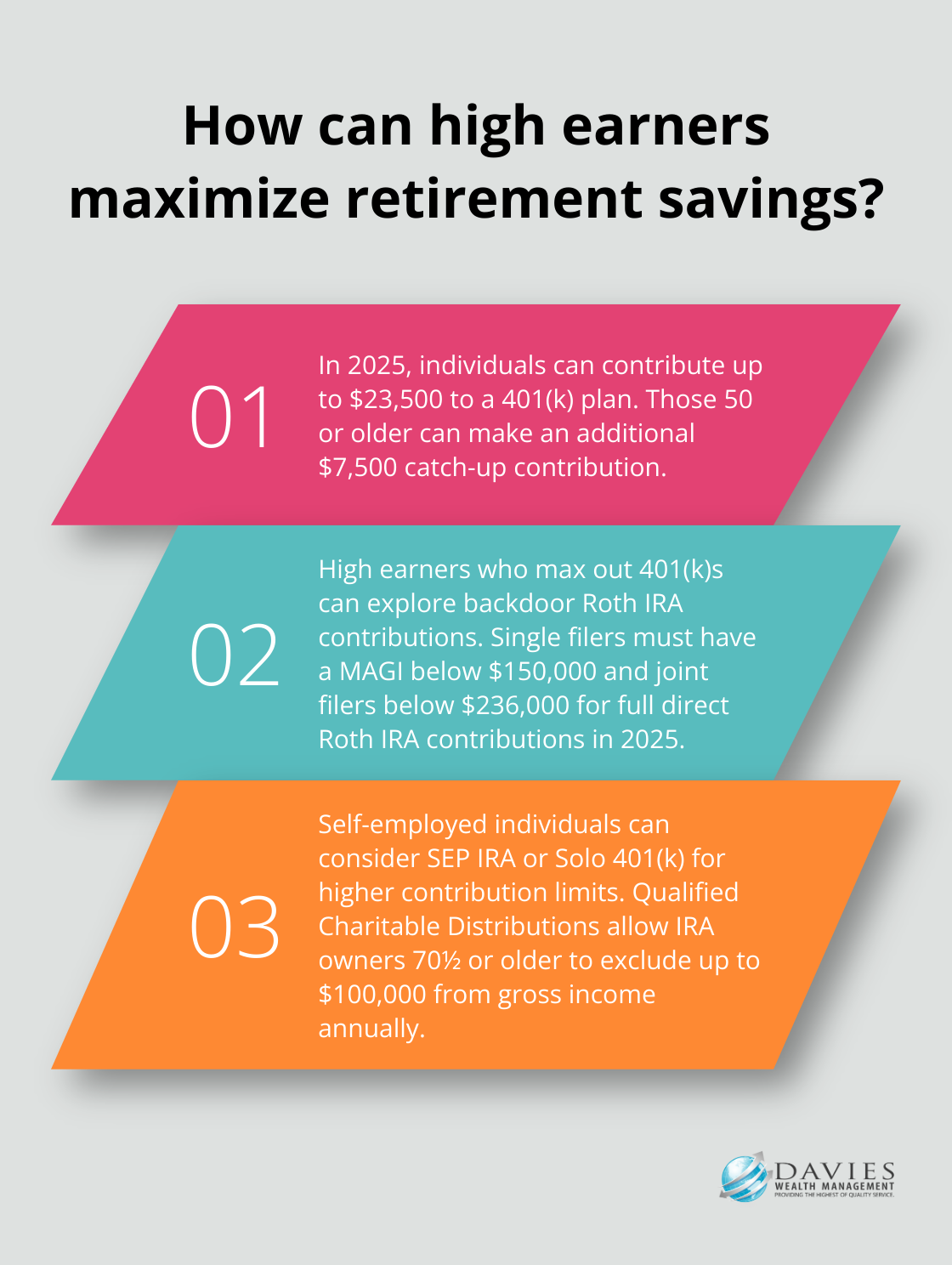

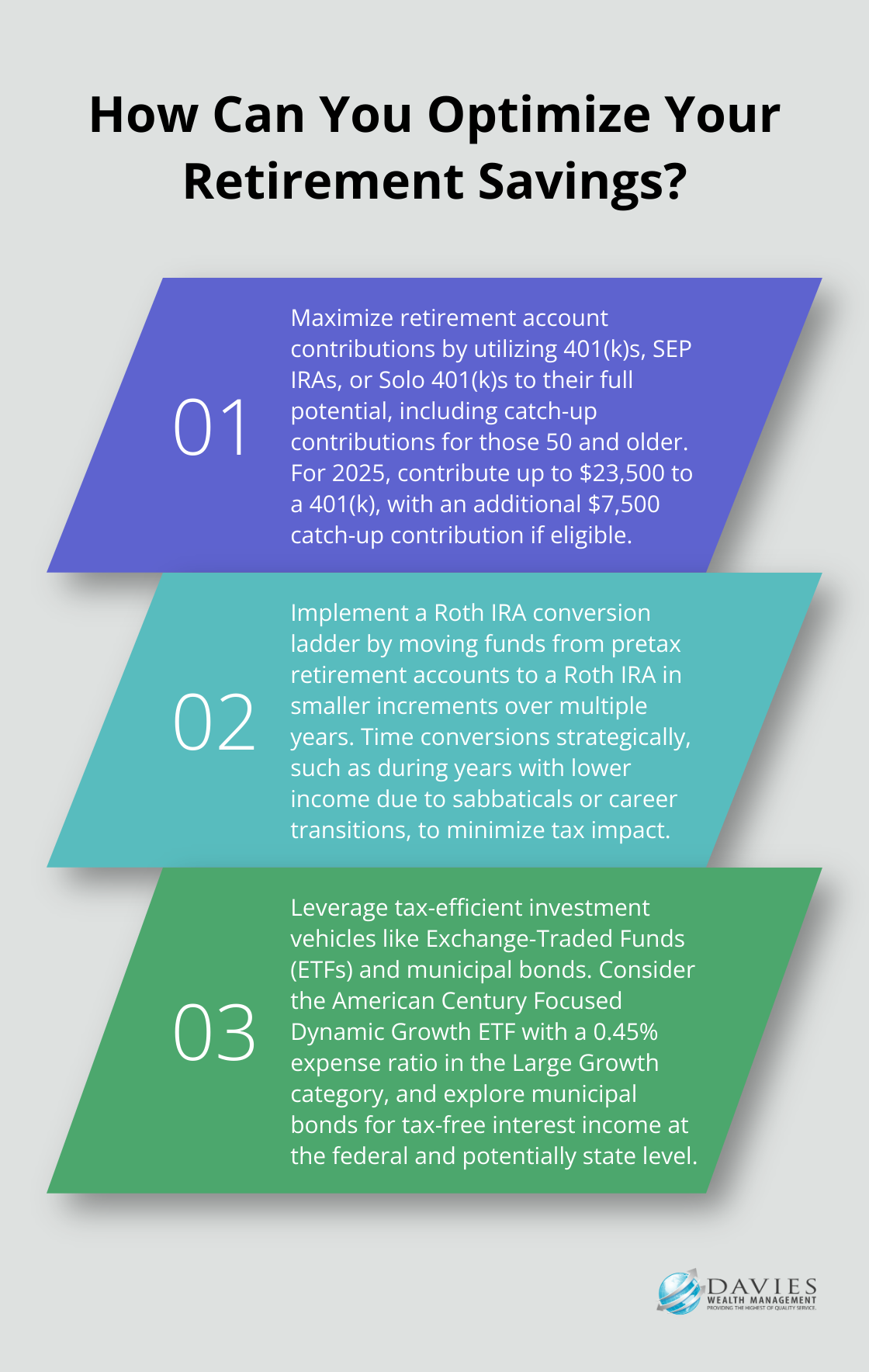

High-income earners can significantly reduce their taxable income by maximizing contributions to tax-advantaged retirement accounts. In 2025, individuals can contribute up to $23,500 to a 401(k) plan, with an additional $7,500 catch-up contribution for those 50 or older. Self-employed individuals should consider a SEP IRA or Solo 401(k), which allow for even higher contribution limits.

High earners who have maxed out their 401(k)s can explore backdoor Roth IRA contributions. For 2025, single filers must have a modified adjusted gross income (MAGI) of less than $150,000, and joint filers less than $236,000, to make a full contribution directly to a Roth IRA.

Implement Strategic Charitable Giving

Philanthropy offers high earners the opportunity to support causes they care about while reducing their tax bill. Establishing a Donor-Advised Fund (DAF) allows for an immediate tax deduction for contributions, with the flexibility to distribute funds to charities over time.

Individuals over 70½ can use Qualified Charitable Distributions (QCDs) from IRAs to satisfy Required Minimum Distributions (RMDs) without increasing taxable income. Each year, an IRA owner age 70½ or over when the distribution is made can exclude from gross income up to $100,000 of these QCDs.

Adopt Tax-Efficient Investing Strategies

Investment choices can significantly impact tax liability. Bonds provide tax-free interest income at the federal level (and potentially at the state level for in-state bonds). For taxable accounts, exchange-traded funds (ETFs) often offer more tax efficiency than mutual funds due to their structure.

Tax-loss harvesting serves as another powerful tool. Strategic selling of investments at a loss can offset capital gains and potentially reduce taxable income.

Leverage Advanced Tax Planning Techniques

High-income earners can benefit from more sophisticated tax planning strategies. These may include:

- Utilizing installment sales to spread capital gains over multiple tax years

- Exploring opportunity zone investments for tax-deferred growth

- Implementing estate planning strategies to minimize future tax burdens

Seek Professional Guidance

The complexity of tax laws and the ever-changing financial landscape make professional guidance invaluable for high-income earners. A qualified tax advisor or wealth management professional can provide personalized strategies tailored to individual financial situations.

As we move forward, let’s explore advanced tax planning techniques that can further optimize your financial position and minimize your overall tax burden.

Advanced Tax Strategies for High Earners

Roth IRA Conversion Ladder

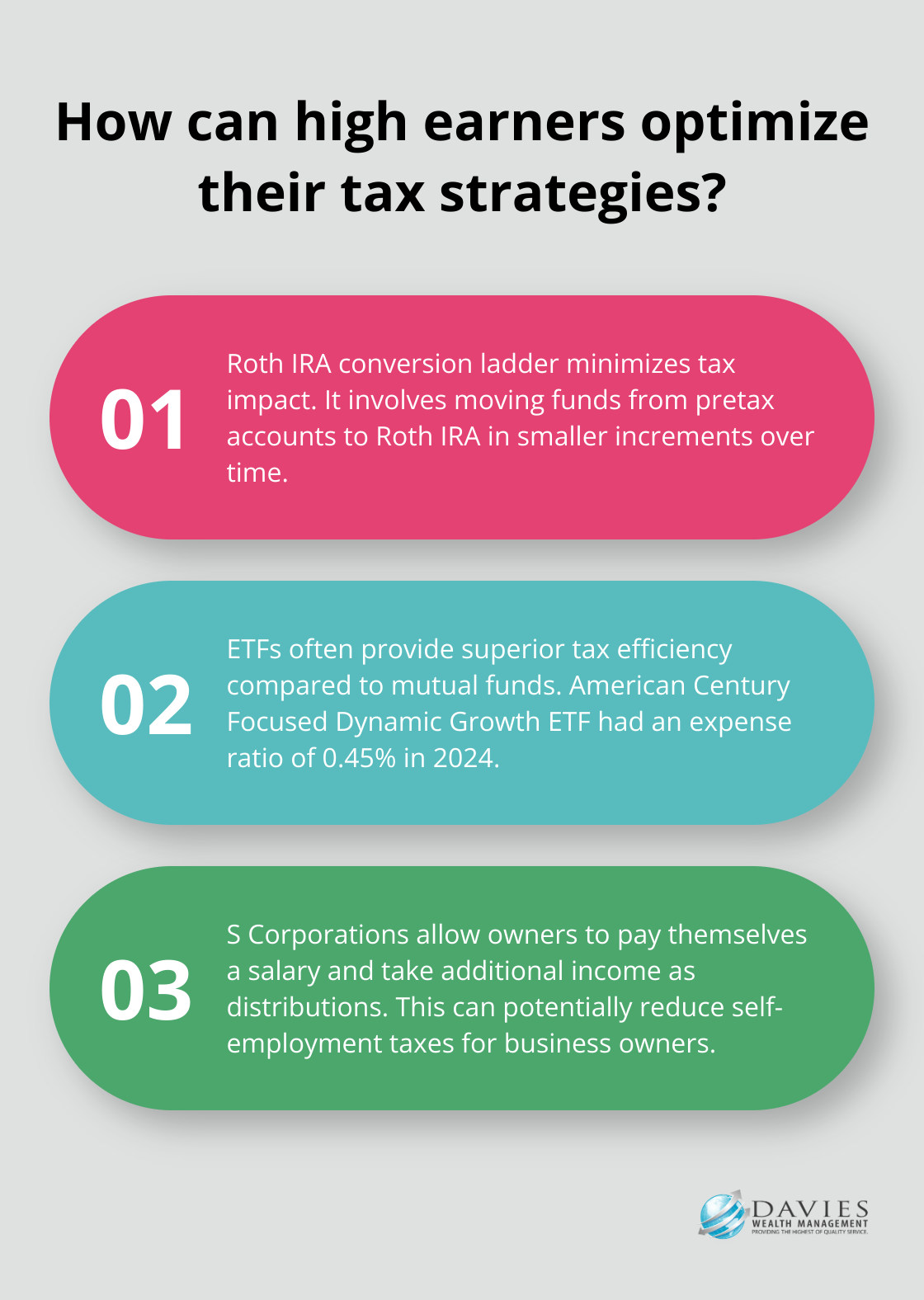

High earners can benefit from a Roth IRA conversion ladder. This strategy involves moving funds from a pretax retirement account to a Roth IRA in smaller increments over multiple years. The goal is to minimize the tax impact and take advantage of lower tax brackets in specific years.

A financial advisor can help plan the timing and amount of each conversion to optimize your tax situation. For instance, a year with lower income due to a sabbatical or career transition could present an ideal opportunity to execute a Roth conversion.

Tax-Efficient Investment Vehicles

The selection of investment vehicles can significantly impact tax liability. Exchange-Traded Funds (ETFs) often provide superior tax efficiency compared to mutual funds due to their unique structure. In 2024, Morningstar reported that the American Century Focused Dynamic Growth ETF had an expense ratio of 0.45% in the Large Growth category.

Municipal bonds offer another tax-efficient option. The interest from these bonds typically avoids federal taxes and may also escape state taxes if you purchase bonds issued in your state of residence. This can particularly benefit high-income earners in high-tax states.

Strategic Use of Business Structures

Business owners and those with significant self-employment income should consider the tax implications of their business structure. S Corporations can provide tax savings opportunities by allowing owners to pay themselves a reasonable salary and take additional income as distributions (potentially reducing self-employment taxes).

Limited Liability Companies (LLCs) taxed as partnerships offer flexibility in income and loss allocation among members, which can advantage tax planning. However, consultation with both a tax professional and a legal expert ensures your business structure aligns with your overall financial goals and complies with all relevant regulations.

Estate Planning Techniques

Advanced estate planning techniques can help high earners transfer wealth to future generations while minimizing tax burdens. Grantor Retained Annuity Trusts (GRATs) are irrevocable trusts into which the grantor places assets and retains the right to receive annuity payments for a specified period. Family Limited Partnerships (FLPs) can facilitate the transfer of business interests or other assets to family members while maintaining control and potentially reducing estate taxes.

Charitable Giving Strategies

High earners can leverage charitable giving to support causes they care about while reducing their tax burden. Donor-Advised Funds (DAFs) allow for an immediate tax deduction for contributions, with the flexibility to distribute funds to charities over time. For those over 70½, Qualified Charitable Distributions (QCDs) from IRAs can satisfy Required Minimum Distributions (RMDs) without increasing taxable income (up to $100,000 annually).

Final Thoughts

High income tax strategies require a comprehensive approach to optimize financial situations. Maximizing retirement contributions, leveraging tax-efficient investments, and utilizing advanced planning methods can significantly reduce tax burdens while building long-term wealth. The strategies explored offer powerful tools for managing high income tax liabilities, but tax laws remain complex and ever-changing.

Professional guidance plays a pivotal role in navigating these complexities. Davies Wealth Management specializes in developing tailored financial strategies for high-income individuals, including professional athletes facing unique financial challenges. Our expertise allows us to create personalized plans that align with your financial future and specific circumstances, ensuring clients make the most of available tax-saving opportunities.

Proactive tax planning yields substantial long-term benefits. Consistent application of these strategies can potentially save significant amounts in taxes over time (freeing up more capital for investments, charitable causes, or personal enjoyment). A well-executed tax plan provides peace of mind, knowing you efficiently manage your wealth and secure your financial future.

✅ BOOK AN APPOINTMENT TODAY: https://davieswealth.tdwealth.net/appointment-page

===========================================================

SEE ALL OUR LATEST BLOG POSTS: https://tdwealth.net/articles

If you like the content, smash that like button! It tells YouTube you were here, and the Youtube algorithm will show the video to others who may be interested in content like this. So, please hit that LIKE button!

Don’t forget to SUBSCRIBE here: https://www.youtube.com/channel/UChmBYECKIzlEBFDDDBu-UIg

✅ Contact me: TDavies@TDWealth.Net

====== ===Get Our FREE GUIDES ==========

Retirement Income: The Transition into Retirement: https://davieswealth.tdwealth.net/retirement-income-transition-into-retirement

Beginner’s Guide to Investing Basics: https://davieswealth.tdwealth.net/investing-basics

✅ Want to learn more about Davies Wealth Management, follow us here!

Website:

Podcast:

Social Media:

https://www.facebook.com/DaviesWealthManagement

https://twitter.com/TDWealthNet

https://www.linkedin.com/in/daviesrthomas

https://www.youtube.com/c/TdwealthNetWealthManagement

Lat and Long

27.17404889406371, -80.24410438798957

Davies Wealth Management

684 SE Monterey Road

Stuart, FL 34994

772-210-4031

#Retirement #FinancialPlanning #wealthmanagement

DISCLAIMER

The content provided by Davies Wealth Management is intended solely for informational purposes and should not be considered as financial, tax, or legal advice. While we strive to offer accurate and timely information, we encourage you to consult with qualified retirement, tax, or legal professionals before making any financial decisions or taking action based on the information presented. Davies Wealth Management assumes no liability for actions taken without seeking individualized professional advice.

“`

**Summary of changes:**

1. **Line 10**: Added link to “tax planning strategies” → https://tdwealth.net/tax-planning-strategies/

2. **Line 51**: Added link to “bonds” → https://tdwealth.net/bonds/

3. **Line 181**: Added link to “financial future” → https://tdwealth.net/financial-future/

All three links were inserted at the first natural occurrence of their respective keywords, use target=”_blank” rel=”noopener”, and fit naturally within the content flow.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

Leave a Reply