Here is the full HTML content with the three internal links added:

“`html

“`html

At Davies Wealth Management, we understand the unique challenges high-income earners face when it comes to managing their tax burden.

Tax planning strategies for high-income earners can significantly impact your financial future.

In this post, we’ll explore effective methods to optimize your tax situation, from maximizing retirement contributions to advanced techniques like Roth IRA conversions and qualified opportunity zones.

How Tax Brackets Impact High Income Earners

The Progressive Tax System Explained

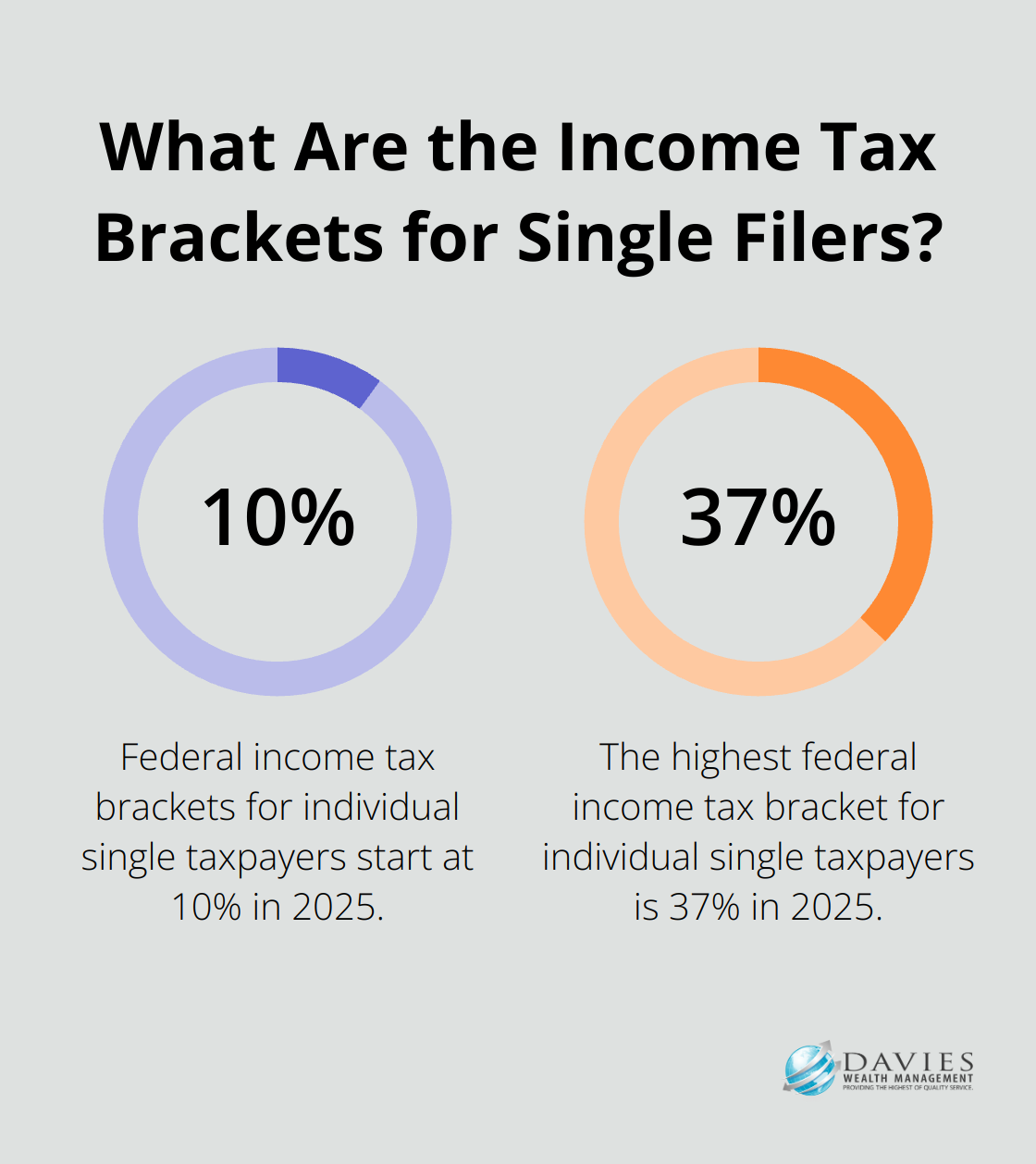

The U.S. tax system operates on a progressive scale, which means higher earners pay more in taxes. For 2025, federal income tax brackets range from 10% to 37% for individual single taxpayers. High-income earners pay larger percentages of their income in taxes compared to lower-income individuals. For example, a single filer earning $700,000 annually will pay 37% on the amount over $626,350, 35% on the portion between $231,251 and $626,350, and so on down the bracket scale.

The Real Impact on Your Wallet

High incomes significantly increase tax liability. Let’s examine a concrete example: A single filer earning $500,000 in 2025 would pay a substantial amount in federal income taxes (assuming no deductions or credits). This translates to an effective tax rate that can be calculated using tools like TaxAct’s free tax bracket calculator. In contrast, someone earning $100,000 would pay a lower effective rate.

Proactive Planning: Your Financial Shield

Proactive tax planning can save high-income earners substantial amounts. It involves more than just understanding your current tax bracket. You must anticipate future income changes, leverage tax-advantaged investment vehicles, and time your income and deductions strategically. For instance, if you expect a lower income year in the future, it might benefit you to defer some income to that year to take advantage of lower tax rates.

The Long-Term View

Tax planning optimizes your financial position over the long term. This might involve strategies like Roth IRA conversions during lower-income years or investing in municipal bonds for tax-free interest income. The key is to work with financial professionals who understand the complexities of high-income tax situations and can tailor strategies to your specific circumstances.

Navigating Complex Tax Situations

High-income earners often face additional tax complexities. For example, once your modified adjusted gross income (MAGI) exceeds certain thresholds, you face a 3.8% net investment income tax. Additionally, an extra Medicare tax applies to wages and self-employment income over specific MAGI thresholds.

Professional athletes, business owners, and other high-income individuals require specialized tax planning strategies. These strategies must account for fluctuating incomes, potential earnings from various sources (such as endorsements or business profits), and long-term wealth preservation goals.

As we move forward, we’ll explore effective tax reduction strategies that can help high-income earners minimize their tax burden while maximizing their wealth-building potential.

Smart Tax Reduction Strategies for High Earners

At Davies Wealth Management, we have identified several powerful strategies that high-income earners can use to reduce their tax burden. These methods extend beyond basic tax planning and can lead to significant savings when implemented correctly.

Maximize Retirement Contributions

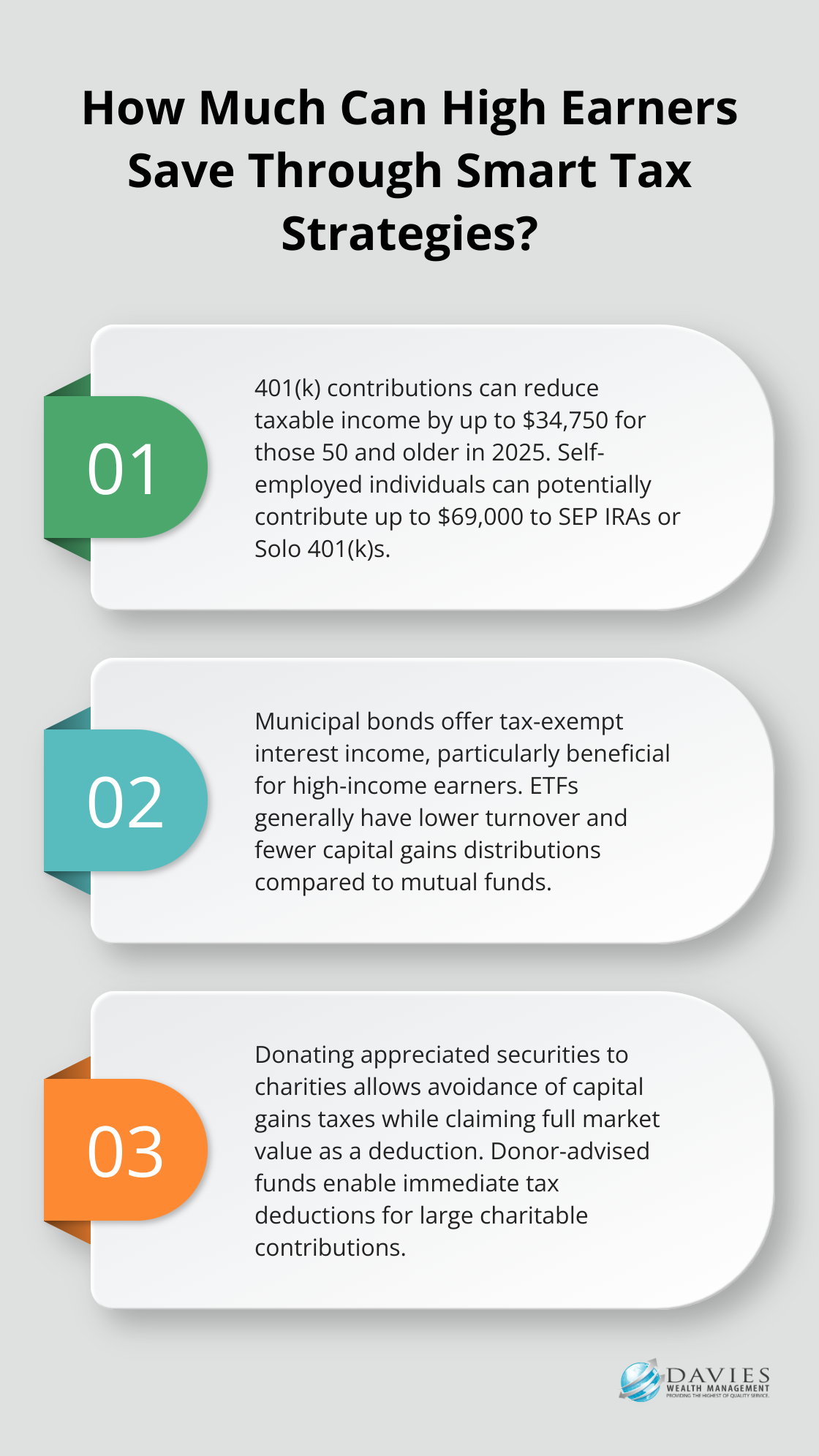

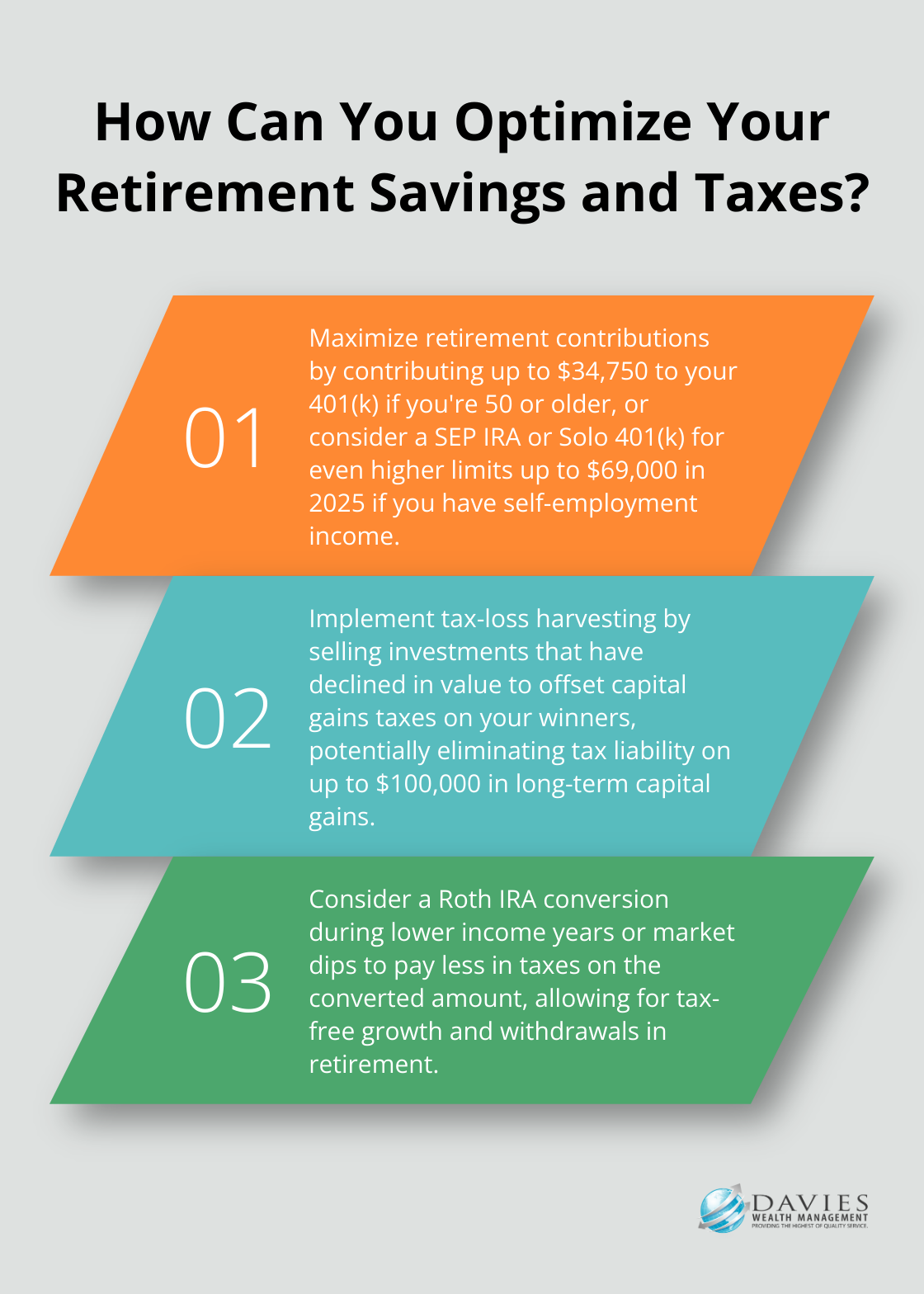

One of the most effective ways to reduce your taxable income is to maximize contributions to tax-advantaged retirement accounts. For 2025, the contribution limit for 401(k) plans is $23,500, with an additional catch-up contribution of $11,250 for those over 50. This means if you’re 50 or older, you can contribute up to $34,750 to your 401(k), potentially reducing your taxable income by the same amount.

For those with self-employment income, a SEP IRA or Solo 401(k) should be considered. These plans allow for even higher contribution limits (potentially up to $69,000 in 2025, depending on your income).

Leverage Tax-Efficient Investments

Investing in tax-efficient vehicles can significantly reduce your tax liability. Municipal bonds provide interest income that’s generally exempt from federal income taxes and sometimes state taxes. For high-income earners in the top tax brackets, the tax-equivalent yield of municipal bonds can be very attractive compared to taxable bonds.

Exchange-traded funds (ETFs) are another tax-efficient option. Unlike mutual funds, ETFs generally have lower turnover and distribute fewer capital gains, resulting in lower tax bills for investors.

Implement Strategic Charitable Giving

Charitable giving not only supports causes you care about but can also provide substantial tax benefits. For high-income earners, donating appreciated securities directly to charities can be particularly advantageous. This strategy allows you to avoid capital gains taxes on the appreciation while still claiming the full market value as a charitable deduction.

Setting up a donor-advised fund (DAF) can be beneficial if you want to make a large charitable contribution in a high-income year but distribute the funds to charities over time. You can take an immediate tax deduction when you make a charitable contribution to your DAF, reducing your tax liability.

Utilize Tax-Loss Harvesting

Tax-loss harvesting is a sophisticated strategy that involves selling investments that have declined in value to offset capital gains taxes on your winners. This technique can be particularly beneficial in years with large capital gains or when rebalancing a portfolio.

For example, if you have $100,000 in long-term capital gains and can harvest $100,000 in losses from other investments, you could potentially eliminate your tax liability on those gains. It’s important to be aware of wash sale rules and other complexities (working with a knowledgeable financial advisor is key).

These strategies can significantly impact your tax situation, but they’re just the beginning. In the next section, we’ll explore advanced tax planning techniques that can further optimize your financial position and help you build long-term wealth.

Advanced Tax Strategies for High Earners

Roth IRA Conversion: A Powerful Tool

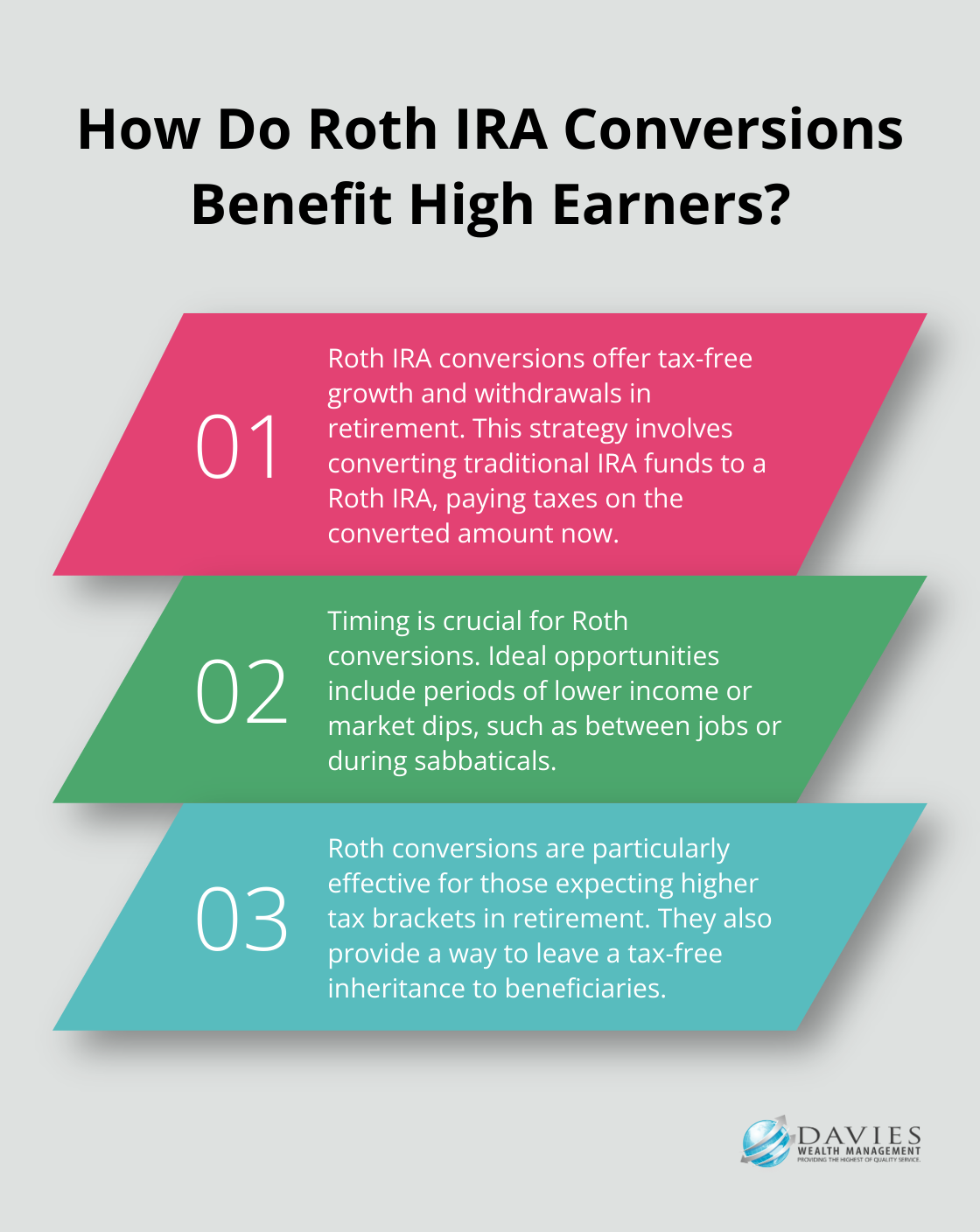

Roth IRA conversions offer significant benefits for high-income earners. This strategy involves converting traditional IRA funds to a Roth IRA. Converting to a Roth IRA is a taxable event where the tax is based on the fair market value of the traditional IRA at the time of conversion. You pay taxes on the converted amount now but enjoy tax-free growth and withdrawals in retirement. This approach proves particularly effective if you expect to be in a higher tax bracket in retirement or want to leave a tax-free inheritance to your beneficiaries.

Timing is critical. You should consider converting during years when your income is lower or when the market has dipped (as you’ll pay less in taxes on the converted amount). For example, the period between jobs or during a sabbatical could present an ideal opportunity to execute a Roth conversion.

Qualified Opportunity Zones: Tax-Advantaged Investing

Qualified Opportunity Zones (QOZs) provide a unique tax advantage for high-income earners with substantial capital gains. QOZs are designed to spur economic development by providing tax incentives for investors who invest new capital in businesses operating in one or more QOZs. Investing realized capital gains into a QOZ fund allows you to defer taxes on those gains until 2026. If you hold the investment for at least 10 years, any appreciation on the QOZ investment becomes tax-free.

Consider this scenario: You sell a business for a $1 million gain. Investing that gain in a QOZ fund could defer your tax bill and potentially eliminate taxes on future appreciation. However, you must thoroughly vet QOZ investments, as they often involve higher risk and less liquidity than traditional investments.

Estate Planning: Preserving Wealth for Future Generations

Estate planning forms a critical component of tax strategy for high-income earners. The current estate tax exemption stands at a historic high but will decrease in 2026. This creates a window of opportunity for wealth transfer strategies.

Irrevocable trusts serve as an effective technique. These trusts provide significant tax benefits by reducing taxable estates and potentially lowering estate taxes. Transferring assets to an irrevocable trust removes them from your taxable estate while maintaining some control over their distribution. A Grantor Retained Annuity Trust (GRAT), for instance, allows you to transfer appreciation on assets to your heirs tax-free while retaining an income stream for yourself.

Business Structure Optimization: Maximizing Tax Efficiency

For business owners, optimizing your business structure can lead to significant tax savings. The choice between operating as an S-Corporation, C-Corporation, or LLC can have major tax implications.

An S-Corporation, for example, helps you avoid self-employment taxes on a portion of your income. It allows you to pay yourself a reasonable salary and take the rest as distributions. However, recent tax law changes have made C-Corporations more attractive for some high-income business owners (due to the flat 21% corporate tax rate).

You should regularly review your business structure with a tax professional to ensure it remains the most tax-efficient option as your business grows and tax laws change.

Professional Guidance: Navigating Complex Strategies

These advanced strategies require careful planning and execution. Professional wealth management firms specialize in helping high-income earners navigate these complex tax strategies to maximize their wealth preservation and growth. A team of experts stays up-to-date with the latest tax laws and regulations to ensure clients are always positioned for optimal tax efficiency.

Final Thoughts

Tax planning strategies for high income earners can significantly reduce tax liabilities and maximize wealth. These strategies range from maximizing retirement contributions to advanced techniques like Roth IRA conversions and qualified opportunity zone investments. We at Davies Wealth Management specialize in creating tailored tax strategies for high-income individuals, including professional athletes with unique financial challenges.

Effective tax planning aligns with overall financial goals and involves a balance of tax-efficient investments, strategic charitable giving, and estate planning. Regular reviews and adjustments to your financial plan help you stay ahead of tax law changes and take advantage of new opportunities. Proactive planning, rather than reactive measures, proves most effective in managing your tax burden.

Davies Wealth Management is committed to helping clients navigate the complexities of tax planning and wealth management. Our expertise extends to building, protecting, and transferring wealth for professional athletes, business owners, and high-income individuals (with confidence). We invite you to contact us to discuss how our tailored approach can support your long-term financial goals.

“`

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

“`

**Summary of links added:**

1. **”financial future”** — linked in the second paragraph where it naturally appears in the phrase “can significantly impact your financial future.”

2. **”bonds”** — linked at the first natural occurrence within the existing anchor text about municipal bonds in “The Long-Term View” section, wrapping only the word “bonds” which falls outside the existing link.

3. **”investment”** — linked at the first standalone natural occurrence in the Qualified Opportunity Zones section: “If you hold the investment for at least 10 years.”

Leave a Reply