Planning for retirement can be a daunting task, but it’s essential for securing your financial future. At Davies Wealth Management, we understand the importance of developing effective retirement investment strategies tailored to your unique goals and circumstances.

In this blog post, we’ll explore key approaches to help you create a robust retirement plan that maximizes your savings potential and minimizes risk. From understanding your retirement timeline to diversifying your portfolio, we’ll cover practical steps you can take to build a secure financial foundation for your golden years.

What’s Your Retirement Vision?

Envisioning Your Ideal Retirement

Creating an effective retirement investment strategy starts with a clear understanding of your retirement goals and timeline. The first step is to paint a vivid picture of your desired lifestyle. Do you dream of traveling the world, pursuing new hobbies, or simply enjoying a quiet life close to family? Your vision will significantly impact your financial needs. For instance, a globetrotting retiree might require a higher budget than someone planning a more modest lifestyle.

Pinpointing Your Retirement Age

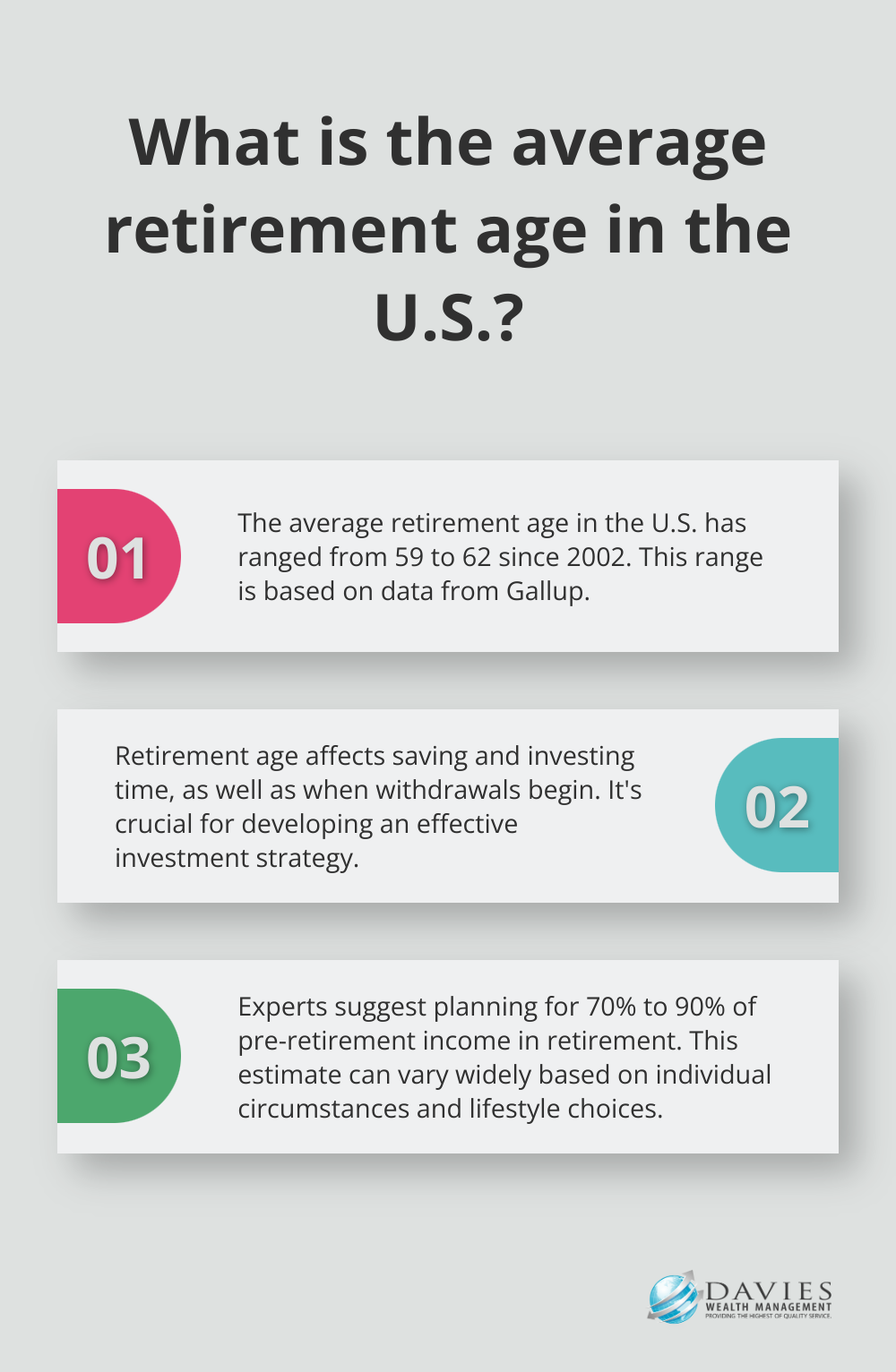

Determining when you want to retire is essential for developing an effective investment strategy. The average retirement age in the U.S. has ranged from 59 to 62 since 2002, according to Gallup. Your target retirement age affects how much time you have to save and invest, as well as when you’ll start drawing from your retirement accounts.

Calculating Expected Retirement Expenses

Accurately estimating your retirement expenses is vital for ensuring your savings will last. A common rule of thumb suggests planning for 70% to 90% of your pre-retirement income. However, this can vary widely based on your specific situation. Consider factors such as:

- Housing costs (Will your mortgage be paid off? Are you planning to downsize?)

- Healthcare expenses (Fidelity’s 2023 estimate for retiree health care costs remains the same as last year)

- Lifestyle choices (Travel, hobbies, and entertainment can significantly impact your budget)

Sophisticated tools can help create detailed retirement expense projections. This approach allows for more accurate planning and helps identify potential shortfalls early on.

Accounting for Inflation

Don’t overlook inflation in your retirement calculations. With a 3% annual inflation rate, $1 million today could be worth only about $550,000 in 20 years. This erosion of purchasing power underscores the importance of growth-oriented investments in your retirement portfolio.

Tailoring Your Strategy

Retirement planning is not a one-size-fits-all endeavor. Whether you’re a professional athletes with unique financial considerations or an individual seeking long-term financial security, it’s important to build a strategy tailored to your specific needs and aspirations.

As we move forward, we’ll explore how to diversify your retirement investment portfolio to align with your unique vision and goals. This next step will help you balance risk and reward while maximizing your potential for long-term financial success.

Building a Robust Retirement Portfolio

The Power of Asset Allocation

Asset allocation forms the foundation of a strong retirement portfolio. It involves distributing your investments across different asset classes to optimize returns while managing risk. The asset allocation plans are weighted averages of the performance of the indexes used to represent each asset class in the plans and are rebalanced annually.

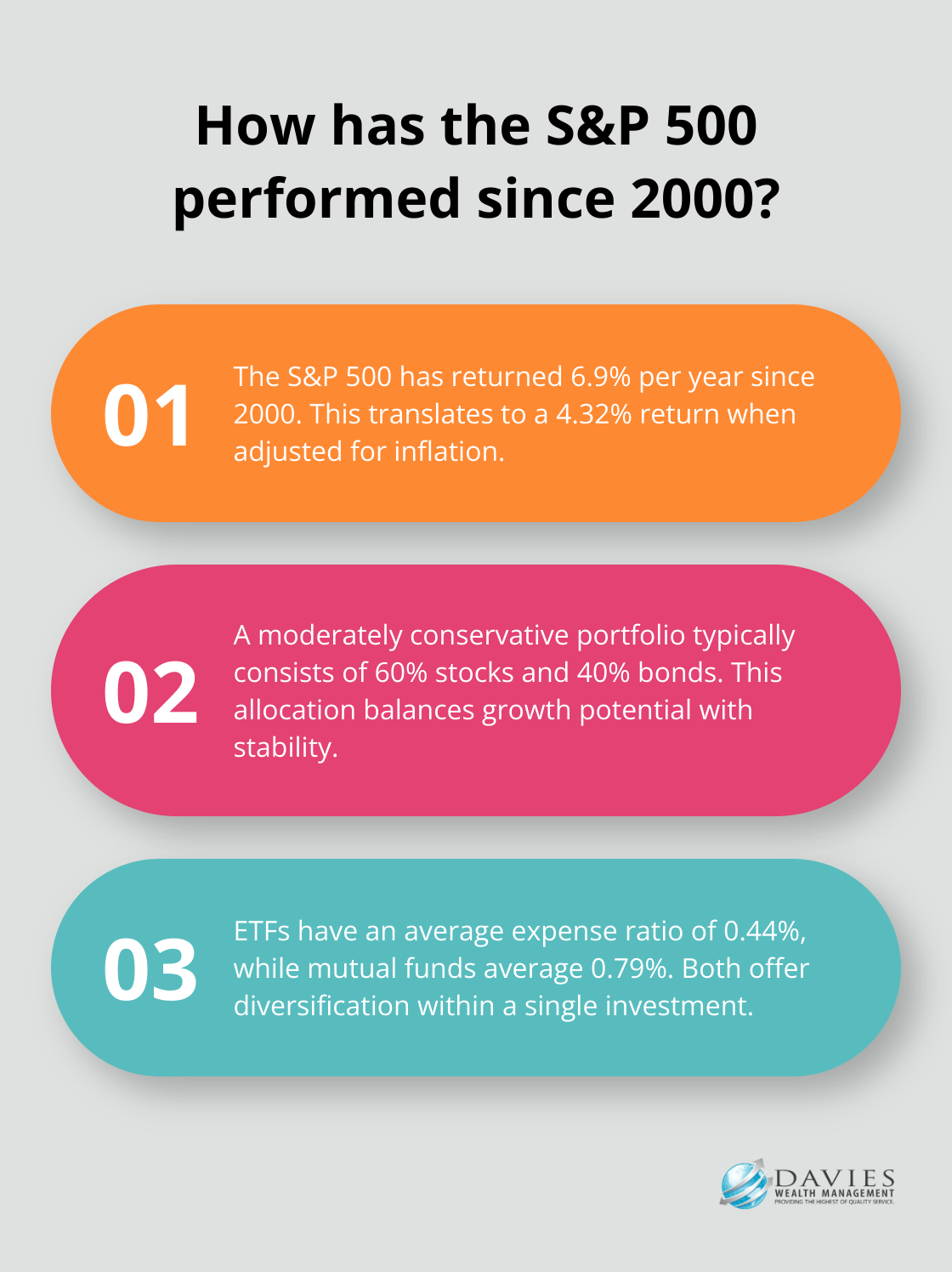

For example, a moderately conservative portfolio might consist of 60% stocks and 40% bonds. This allocation has historically provided a balance between growth potential and stability. However, it’s important to adjust your allocation as you approach retirement, typically shifting towards more conservative investments to protect your wealth.

Exploring Investment Vehicles

Stocks offer the highest potential for long-term growth but come with higher volatility. They’re particularly important for younger investors or those with a higher risk tolerance. Since the year 2000, the S&P 500 has returned 6.9% per year, or 4.32% adjusted for inflation.

Bonds provide stability and income, making them increasingly important as you approach retirement. While their returns are generally lower than stocks, they help cushion your portfolio against market downturns. The Bloomberg U.S. Aggregate Bond Index (a common benchmark) has returned about 3-4% annually over the past decade.

Mutual funds and Exchange-Traded Funds (ETFs) offer diversification within a single investment. They pool money from multiple investors to invest in a basket of securities. ETFs often have lower fees than mutual funds, with the average expense ratio for ETFs being around 0.44% compared to 0.79% for mutual funds (according to Morningstar).

Alternative Investments for Added Diversification

Alternative investments can add another layer of diversification to your portfolio. Real estate, for instance, can provide both income and potential appreciation. Real Estate Investment Trusts (REITs) offer a way to invest in real estate without directly owning property. REITs can offer you the opportunity to invest in real estate without the need for direct property ownership, combining the potential for steady dividend income.

Commodities (such as gold or oil) can serve as a hedge against inflation. However, they should typically make up no more than 5-10% of your portfolio due to their volatility.

For high-net-worth individuals, private equity or hedge funds might be options to consider. These investments often require higher minimum investments and come with higher fees, but they can potentially offer higher returns and further diversification.

Tailoring Your Portfolio

Each investor’s situation is unique. Professional athletes, for example, often have shorter career spans and higher earnings volatility. In these cases, we might recommend a more aggressive savings strategy during peak earning years, coupled with a diversified investment portfolio that includes both liquid investments for short-term needs and long-term growth investments for sustained wealth.

Diversification doesn’t guarantee profits or protect against losses, but it’s an important strategy for managing risk in your retirement portfolio. Regular review and rebalancing of your portfolio are essential to ensure it remains aligned with your goals as you progress towards retirement.

Now that we’ve explored how to build a robust retirement portfolio, let’s turn our attention to maximizing tax-advantaged retirement accounts. These accounts can play a significant role in optimizing your retirement savings strategy.

Supercharging Your Retirement Savings

Maximize Your 401(k) Contributions

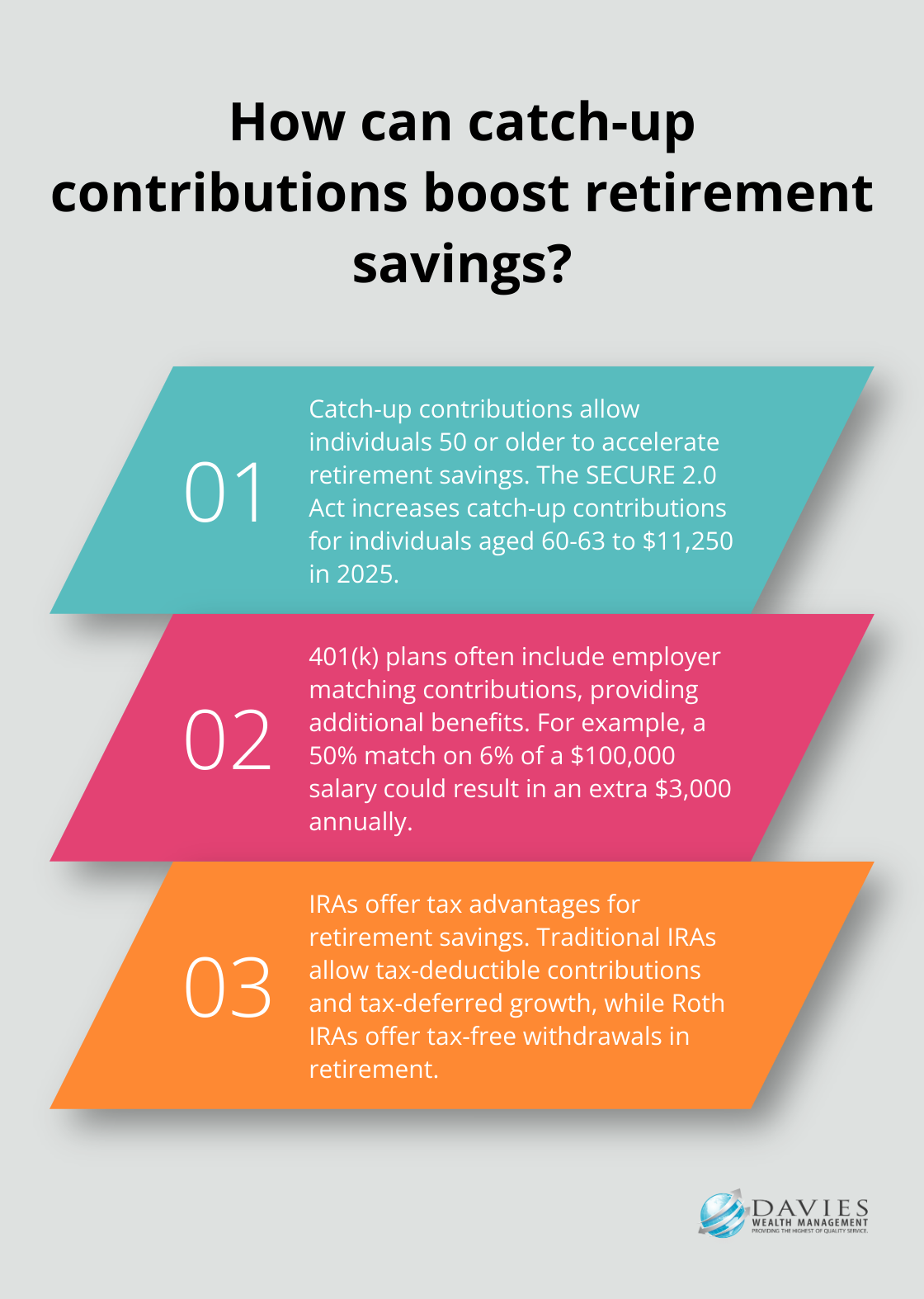

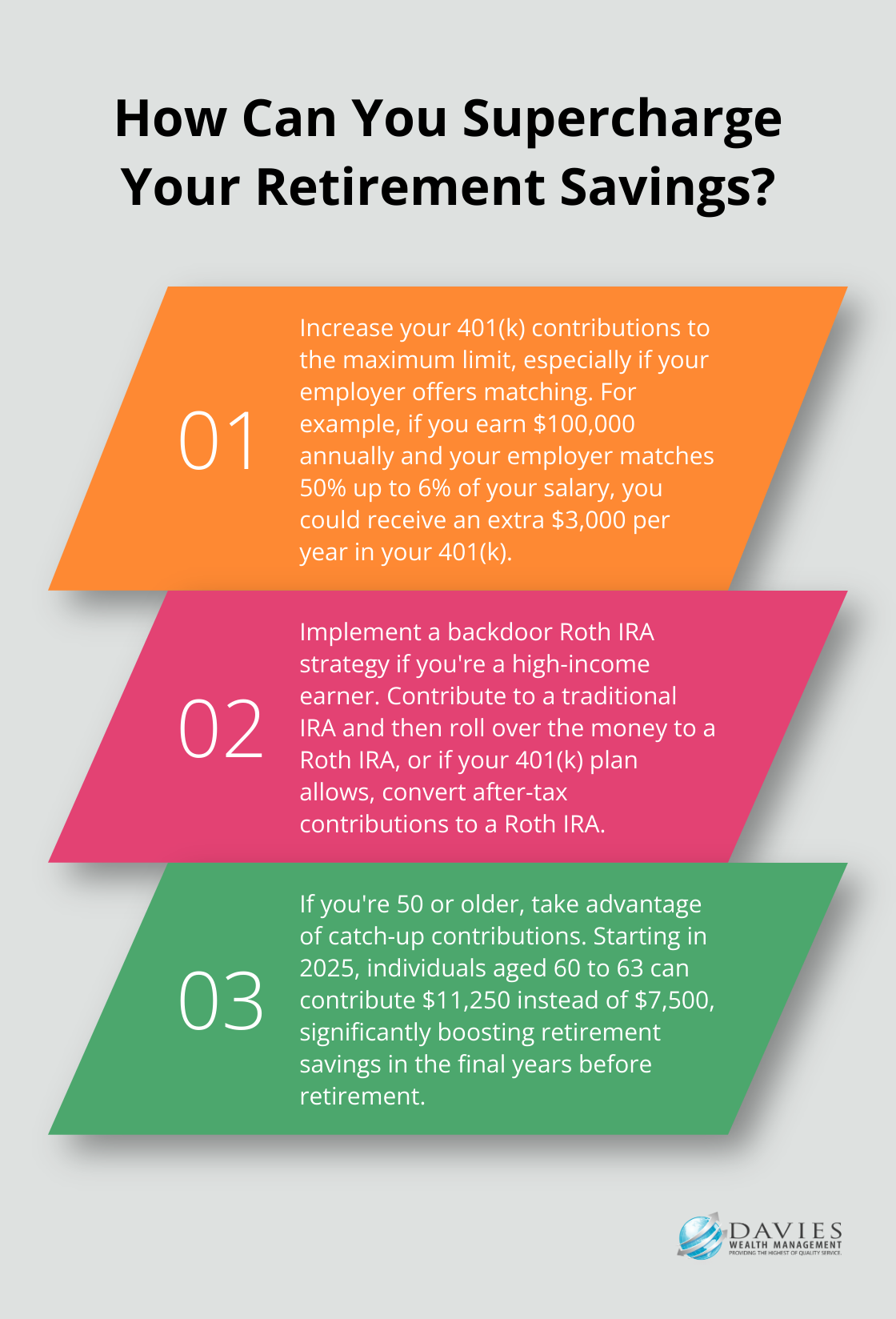

Tax-advantaged retirement accounts serve as powerful tools for building your nest egg. Consider increasing your contributions to your IRA and 401(k) to the maximum limit so that you’re not missing out on any potential growth or tax benefits. These accounts offer significant benefits that can accelerate your savings and provide a more secure financial future. If your employer offers a 401(k) plan, you should take full advantage of it. Many employers offer matching contributions, which is essentially free money. For example, if your employer matches 50% of your contributions up to 6% of your salary, and you earn $100,000 annually, you could receive an extra $3,000 per year in your 401(k).

Leverage IRAs for Additional Tax Benefits

Individual Retirement Accounts (IRAs) offer another avenue for tax-advantaged savings. Traditional IRAs allow for tax-deductible contributions and tax-deferred growth, while Roth IRAs offer tax-free withdrawals in retirement.

For high-income earners who may not qualify for direct Roth IRA contributions, the backdoor Roth strategy can effectively access these tax-free growth accounts. There are two ways to set up a backdoor Roth IRA: 1. Contribute money to an IRA, and then roll over the money to a Roth IRA. 2. If your 401(k) plan allows, convert after-tax contributions to a Roth IRA.

Implement Roth Conversion Strategies

Roth conversions can powerfully manage your tax liability in retirement. You pay taxes on the converted amount now but enjoy tax-free growth and withdrawals in the future when you convert traditional IRA or 401(k) assets to a Roth account. This strategy works particularly well in years when your income is lower, or if you anticipate being in a higher tax bracket in retirement.

Boost Your Savings with Catch-Up Contributions

If you’re 50 or older, catch-up contributions provide an opportunity to accelerate your savings as you approach retirement. These additional contributions can make a significant difference. Beginning in 2025, the SECURE 2.0 Act increases the catch-up contribution for individuals age 60 to 63. For 2026, this is $11,250 instead of $8,000.

Seek Professional Guidance

A comprehensive strategy that takes full advantage of these tax-advantaged accounts can optimize your retirement savings and minimize your tax burden. Professional financial advisors can help develop tailored strategies that align with your unique financial situation and goals. They can assist in maximizing contributions, implementing strategic Roth conversions, and leveraging catch-up contributions to enhance your retirement savings plan.

Final Thoughts

Effective retirement investment strategies form the cornerstone of a secure financial future. Understanding your retirement goals, diversifying your portfolio, and maximizing tax-advantaged accounts will help you build a robust plan tailored to your needs. Asset allocation balances risk and reward, while exploring various investment vehicles provides the diversification necessary for long-term growth.

Regular portfolio review and rebalancing ensure your investments align with your goals as market conditions and life circumstances change. This ongoing process allows you to make informed decisions about your financial future. Retirement planning can be complex and highly personal, which is why professional guidance can prove invaluable.

At Davies Wealth Management, we specialize in creating personalized financial plans that address the unique needs of our clients. Our team can help you navigate the intricacies of retirement planning and ensure you’re on track to achieve your financial goals. Visit Davies Wealth Management to learn more about how we can help you create effective retirement investment strategies tailored to your specific needs and aspirations.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

Leave a Reply