Here is the full HTML content with the three links added at their first natural occurrences:

“`html

“`html

Mastering the financial planning process is essential for achieving your monetary goals and securing your financial future. At Davies Wealth Management, we understand the importance of a well-structured approach to managing your finances.

In this guide, we’ll walk you through the key steps of effective financial planning, from setting clear objectives to implementing a comprehensive strategy. By following these steps, you’ll be better equipped to take control of your financial life and work towards long-term success.

What Are Your Financial Goals?

Define Your Short-Term and Long-Term Goals

The first step in mastering the financial planning process is to set clear financial goals. At Davies Wealth Management, we believe that understanding your objectives forms the foundation of your financial success.

Start by listing your financial aspirations. Short-term goals might include saving for a vacation, paying off credit card debt, or building an emergency fund. Long-term goals often involve saving for retirement, buying a home, or funding your children’s education. Be specific about what you want to achieve and when you want to achieve it.

Prioritize Your Financial Objectives

After you identify your goals, prioritize them. Consider the urgency and importance of each objective. For instance, building an emergency fund might take precedence over saving for a luxury purchase. A recent study reveals that about half of Americans had enough savings to cover a $1,000 emergency expense in 2023, down from 59% in 2021 when people still had pandemic relief money. This statistic underscores the importance of prioritizing an emergency fund in your financial plan.

Create SMART Financial Objectives

To increase your chances of success, transform your goals into SMART objectives (Specific, Measurable, Achievable, Relevant, and Time-bound). Instead of saying “I want to save more,” a SMART goal would be “I will save $10,000 for a down payment on a house within 18 months by setting aside $555 per month.”

Research from the Dominican University of California shows that people who write down their goals are 42% more likely to achieve them. Take the time to document your SMART objectives and review them regularly.

Align Your Goals with Your Values

Ensure your financial goals align with your personal values and life aspirations. If you value experiences over material possessions, your goals should reflect that. For example, you might prioritize saving for travel or continuing education over purchasing luxury items.

Tailor Goals for Unique Situations

Different life circumstances require different financial goals. For instance, professional athletes face distinct financial challenges due to their short career spans and fluctuating income. The key to long-term financial security for athletes lies in careful planning from day one, requiring special tax planning and wealth management strategies.

As you move forward in the financial planning process, the next step involves assessing your current financial situation. This assessment will provide a clear picture of where you stand financially and help you identify the steps needed to reach your newly defined goals.

Where Do You Stand Financially?

Calculate Your Net Worth

The first step to assess your financial situation involves calculating your net worth. Net worth is a way to measure financial health by taking someone’s total assets and then subtracting all debts. List all your assets (what you own) and subtract your liabilities (what you owe). Assets include cash, investments, property, and valuable possessions. Liabilities encompass mortgages, loans, and credit card debts. The Federal Reserve’s 2019 Survey of Consumer Finances reported the median net worth of U.S. households at $121,700. This benchmark provides valuable context for your personal financial standing.

Analyze Your Cash Flow

Examine your cash flow by tracking your income sources and spending patterns over several months. This analysis will reveal whether you live within your means or overspend. The Bureau of Labor Statistics reports that average annual expenditures decreased 2.7 percent between 2019 and 2020 (from $63,036 to $61,334, respectively). Compare your spending to this figure and identify areas where you can potentially reduce expenses.

Evaluate Your Investments and Insurance

Review your investment portfolio and insurance coverage. Ensure your investments align with your risk tolerance and financial goals. The S&P 500 has historically returned about 9.381% annually over the last 150 years, as of the end of December 2024. Compare your portfolio’s performance to relevant benchmarks.

For insurance, ensure you have adequate coverage. A general rule suggests life insurance coverage equal to 10-15 times your annual income. However, your specific needs may vary based on your circumstances.

Identify Improvement Areas and Risks

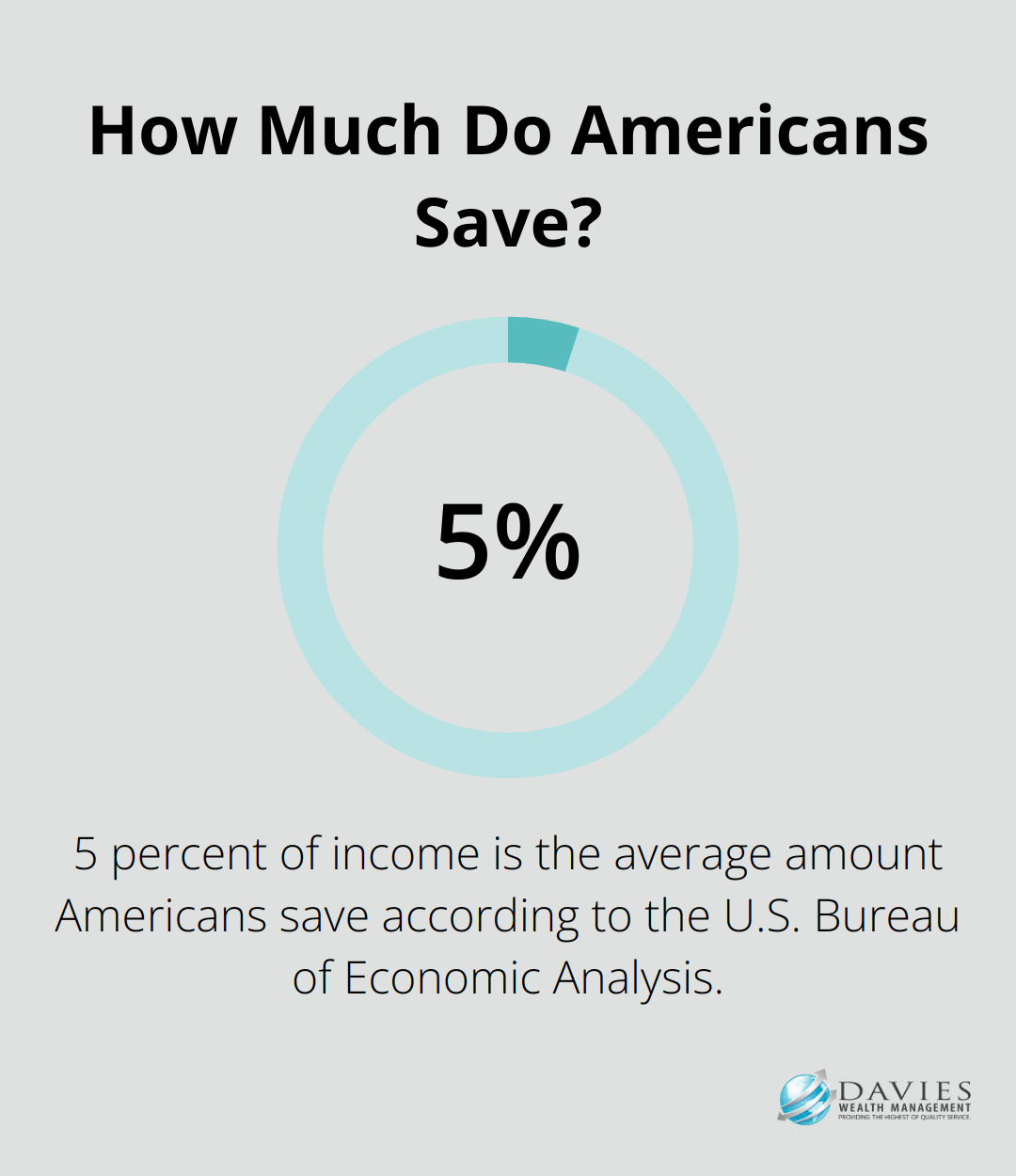

Look for areas to improve your financial situation. This might include increasing your savings rate, diversifying your investments, or reducing high-interest debt. The U.S. Bureau of Economic Analysis reports that the average American saves only about 5% of their income. Try to save at least 20% of your income for long-term financial security.

Consider potential risks to your financial health, such as job loss, health issues, or market downturns. An emergency fund covering 3-6 months of expenses can provide a crucial safety net.

Special Considerations for Athletes

Professional athletes face unique financial landscapes. They often have short career spans with high earnings potential, requiring specialized strategies for long-term financial security. These strategies may include tax planning, investment diversification, and post-career income planning.

A thorough assessment of your current financial situation equips you to develop a comprehensive financial plan that addresses your specific needs and goals. This assessment serves as the foundation for the next step in the financial planning process: developing and implementing your personalized financial strategy.

Building Your Financial Fortress

Create a Budget That Works

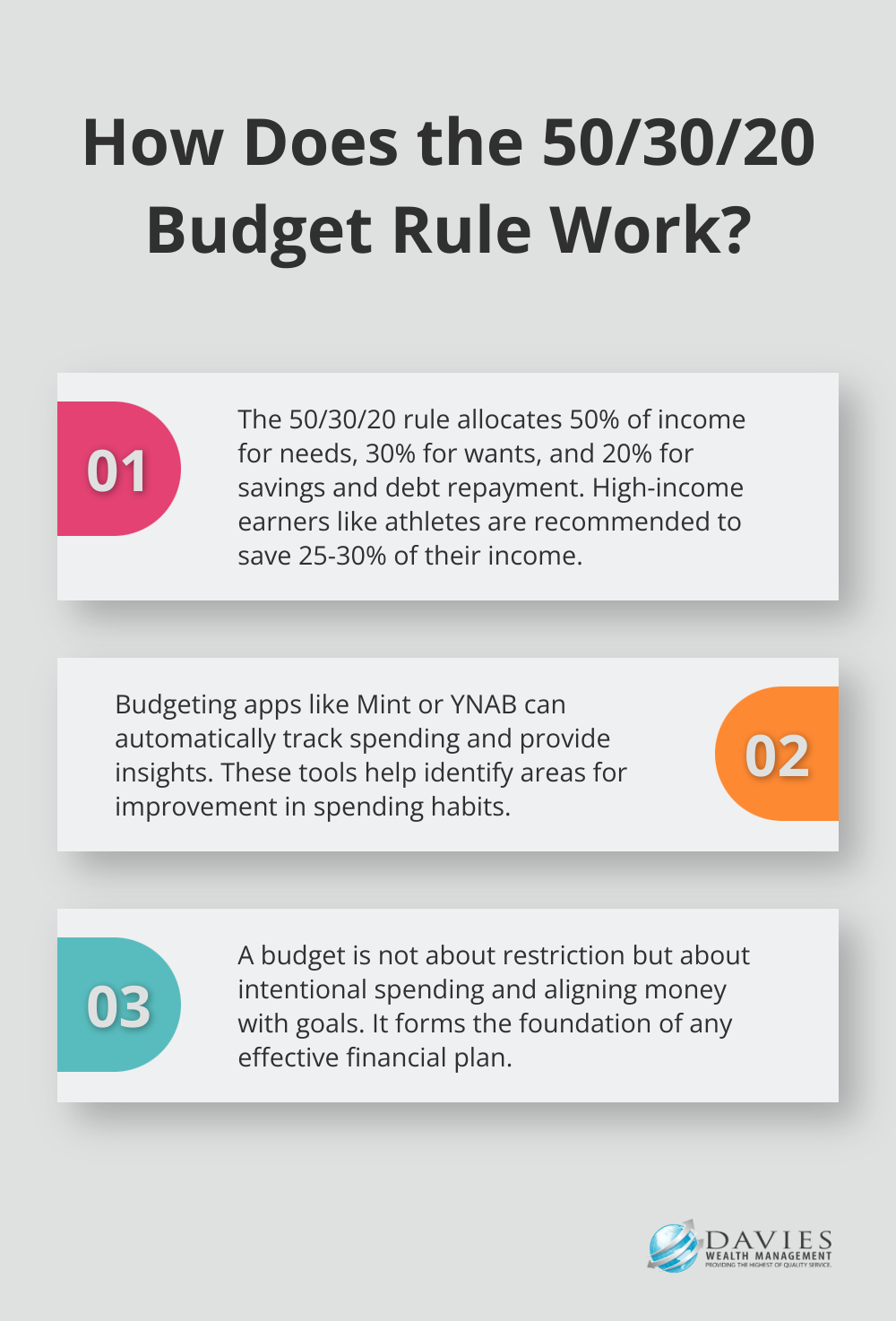

The foundation of any effective financial plan is a well-structured budget. Start by categorizing your expenses and allocating your income accordingly. A popular budgeting method is the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings and debt repayment. However, a more aggressive savings rate of 25-30% is often recommended for high-income earners like professional athletes.

Use budgeting apps like Mint or YNAB to track your spending automatically. These tools provide insights into your spending habits and help you identify areas for improvement. A budget is not about restriction; it’s about intentional spending and aligning your money with your goals.

Design Your Investment Strategy

Your investment strategy should reflect your financial goals, risk tolerance, and time horizon. While the traditional advice of subtracting your age from 100 to determine your stock allocation can be a starting point, a more nuanced approach is often beneficial.

For younger investors with a long time horizon, consider allocating up to 90% in stocks for maximum growth potential. As you near retirement, gradually shift towards a more conservative mix. The Vanguard Total Stock Market Index Fund (VTSAX) has delivered an average annual return of 14.5% over the past decade, making it an excellent core holding for many investors.

For professional athletes with shorter career spans, a more conservative approach initially is often recommended, with a focus on capital preservation and steady growth. As financial literacy improves and careers progress, the strategy can be adjusted to be more aggressive if appropriate.

Maximize Tax Efficiency

Implementing tax-efficient strategies can significantly impact your wealth accumulation over time. Utilize tax-advantaged accounts like 401(k)s, IRAs, and HSAs to their full potential. For high-income earners, consider backdoor Roth IRA contributions or mega backdoor Roth strategies if available through your employer plan.

Tax-loss harvesting can also be a powerful tool. A study by Vanguard found that tax-loss harvesting can add up to 0.35% of additional after-tax return annually. This strategy involves selling investments at a loss to offset capital gains, potentially reducing your tax liability.

Secure Your Future with Insurance

Insurance is a key component of a comprehensive financial plan. At a minimum, ensure you have adequate health, life, and disability insurance. For life insurance, consider a term policy with coverage of 10-15 times your annual income. Disability insurance should replace 60-70% of your income if you’re unable to work.

For high-net-worth individuals, an umbrella policy for additional liability protection is often recommended. These policies typically offer $1-5 million in coverage for a relatively low cost, providing an extra layer of security for your assets.

Plan for Retirement and Beyond

Retirement planning is not just about saving; it’s about creating a sustainable income stream for your post-work years. The 4% rule (which suggests withdrawing 4% of your portfolio annually in retirement) can be a good starting point. However, a more dynamic approach is often recommended, adjusting withdrawal rates based on market conditions and personal circumstances.

For estate planning, consider establishing a trust to protect your assets and ensure they’re distributed according to your wishes. A revocable living trust can help avoid probate and provide flexibility in managing your estate.

Final Thoughts

The financial planning process demands dedication, knowledge, and ongoing commitment. You must set clear goals, assess your current financial situation, and implement a comprehensive strategy to secure your financial future. Financial planning requires regular review and adjustment as life circumstances change and financial markets evolve.

Professional guidance often proves invaluable in navigating the complexities of financial planning. Davies Wealth Management specializes in providing tailored financial solutions for individuals, families, and professional athletes. Our expertise in wealth management positions us to help you achieve your financial objectives.

Working with a professional advisor provides expert insights, objective analysis, and personalized strategies that address your specific needs. Whether you plan for retirement, manage a high-income career, or build long-term wealth, a knowledgeable partner can make a significant difference in achieving your goals (especially when dealing with complex financial situations).

“`

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

“`

Leave a Reply