Here is the full HTML with up to 3 internal links added at the first natural occurrence of each keyword:

🎧 Prefer to listen to the podcast or watch the video? Jump to listen to the podcast & watch the video.

A roth conversion ladder is one of the most consequential tax strategies available to high-net-worth retirees — and one of the most misunderstood. If you have $1 million or more sitting in a traditional IRA, 401(k), or other tax-deferred accounts, every dollar that eventually comes out will be taxed as ordinary income. The question is not whether you’ll pay tax on that money. The question is when — and at what rate.

Done correctly, a multi-year roth conversion ladder can shift hundreds of thousands of dollars from a fully taxable account into a permanently tax-free Roth IRA. The result: lower lifetime taxes, reduced required minimum distributions, better Medicare premium control, and a cleaner wealth transfer to your heirs.

This guide walks through exactly how it works — and why the strategy looks very different at the $2M–$10M level than it does for the average retiree.

Why Tax-Deferred Accounts Become a Problem at High Net Worth

The RMD Time Bomb Inside Your IRA

Most high-net-worth individuals spent decades maximizing contributions to 401(k)s, deferred compensation plans, and traditional IRAs. That was smart at the time — every dollar deferred was a dollar that compounded without the drag of annual taxation.

But here is the problem: the IRS eventually demands its share. Required minimum distributions (RMDs) begin at age 73 under current law (SECURE 2.0). If your tax-deferred balance has grown to $3M, $5M, or more, those mandatory withdrawals can easily push you into the 32% or 37% federal tax bracket — whether you need the income or not.

For context, a $5M IRA at age 73 generates an RMD of roughly $188,000 in year one using the IRS Uniform Lifetime Table. That is taxable income before you spend a single dollar of it.

How the Mass-Market Investor Gets Different Advice

This is where HNW planning diverges sharply from what most people read in general personal finance articles. A typical article on Roth conversions might suggest converting $50,000–$100,000 to “fill up the 22% bracket.” That is appropriate advice for someone with a $400,000 IRA and a modest pension.

It is not the right framework for someone with $4M in a rollover IRA, a deferred compensation payout starting at 65, Social Security at 70, and a commercial real estate portfolio generating passive income.

For that person — and for many Davies Wealth Management clients — the roth conversion ladder requires a coordinated, multi-year blueprint that accounts for bracket management, IRMAA thresholds, state tax implications, and estate planning objectives simultaneously. Consult a qualified tax and financial planning professional for your specific situation before acting on any strategy discussed here.

What Is a Roth Conversion Ladder?

The Core Mechanics Explained Simply

A roth conversion ladder is the practice of systematically converting portions of a traditional IRA (or other pre-tax retirement account) into a Roth IRA over multiple years — rather than all at once. Each annual conversion is calibrated to keep your taxable income below a specific threshold.

The “ladder” metaphor refers to the sequential, year-by-year nature of the conversions. Like rungs on a ladder, each year’s conversion is a deliberate step — not a single leap. The goal is to convert as much as possible at the lowest possible marginal rate before higher-income events force you into a higher bracket.

Why Timing Matters More Than the Conversion Amount

The window for a roth conversion ladder is typically the period between retirement and age 73 (when RMDs begin). For many high-net-worth retirees, this window is 5–15 years of relatively lower income — the “gap years.” This is the optimal time to convert.

After RMDs begin, your taxable income floor rises significantly. Converting on top of large RMDs often means paying 32%–37% on those dollars, which frequently negates the long-term benefit. Acting during the gap years is the strategic imperative.

The 5-Step Roth Conversion Ladder for HNW Retirees

Step 1 — Map Your Income Floor and Identify the Conversion Window

Before converting a single dollar, you need a precise picture of your baseline income in each year of the conversion window. This includes:

- Pension or deferred compensation distributions (and their start dates)

- Social Security benefits (and your planned claiming age)

- Rental income or business distributions

- Required minimum distributions once they begin

- Capital gains from any planned asset sales

Once you know your income floor, you can identify how much “room” exists in each tax bracket before your next marginal rate kicks in.

Step 2 — Set Annual Conversion Targets Around Key Thresholds

For 2026, the federal income tax brackets for married filing jointly are:

- 10%: $0 – $23,850

- 12%: $23,851 – $96,950

- 22%: $96,951 – $206,700

- 24%: $206,701 – $394,600

- 32%: $394,601 – $501,050

- 35%: $501,051 – $751,600

- 37%: Over $751,600

Many HNW clients can convert $150,000–$250,000 per year and remain in the 22%–24% bracket during their gap years. Converting at 22%–24% now — rather than being forced to take RMDs at 32%–37% later — produces significant lifetime tax savings. Consult a qualified tax professional to confirm applicable brackets for your filing status and situation.

Step 3 — Monitor IRMAA Thresholds with Precision

Here is where the roth conversion ladder becomes genuinely complex for high-net-worth retirees: Medicare IRMAA surcharges.

IRMAA (Income-Related Monthly Adjustment Amount) increases your Medicare Part B and Part D premiums based on income from two years prior. In 2026, a married couple filing jointly with modified adjusted gross income (MAGI) above approximately $212,000 begins paying IRMAA surcharges. At higher income levels, the surcharges escalate significantly.

A large Roth conversion that pushes MAGI over an IRMAA cliff — even by $1 — can trigger thousands of dollars in additional Medicare premiums two years later. For a $300,000 conversion, crossing an IRMAA threshold might add $5,000–$15,000 in Medicare costs, meaningfully reducing the net benefit of the conversion.

Precision matters. Your roth conversion ladder must be modeled against IRMAA tiers, not just income tax brackets. Learn more about IRMAA thresholds directly from the Social Security Administration’s Medicare premium information.

Step 4 — Account for State Taxes and Domicile Strategy

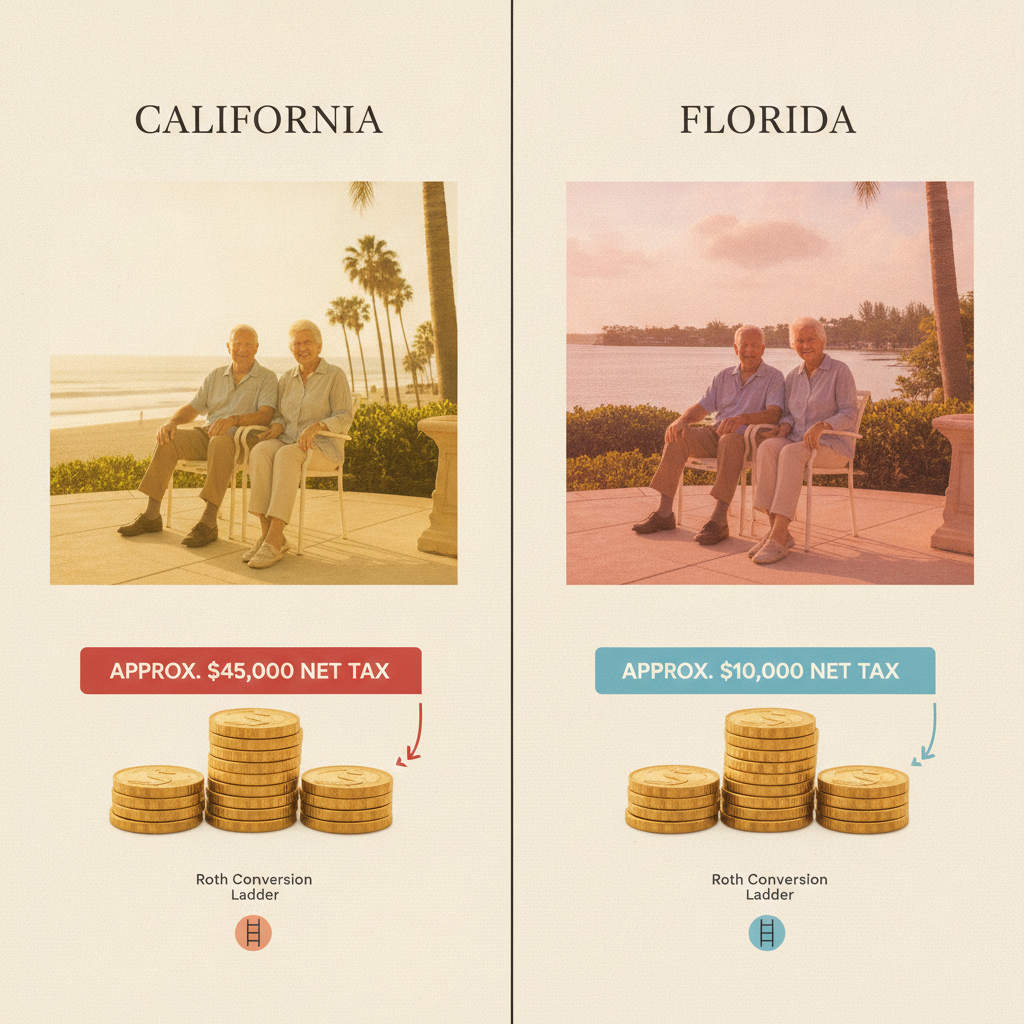

If you live in a high-income-tax state — California (13.3%), New York (10.9%), or New Jersey (10.75%) — every dollar converted is also taxed at the state level. This can dramatically change the math of your roth conversion ladder.

For retirees considering a move to a tax-friendly state like Florida (no state income tax), coordinating your relocation with your conversion schedule can be extraordinarily valuable. Converting after establishing Florida domicile means those same dollars are taxed at zero percent at the state level. On a $500,000 cumulative conversion, the state tax savings alone could exceed $50,000 for a California domiciliary.

This is one of the specific reasons many of our clients in Stuart, Florida chose to relocate before accelerating their roth conversion ladder — not just for the weather, but for the math.

Step 5 — Integrate with Estate Planning and Charitable Strategies

For estates approaching or exceeding the federal estate tax exemption — which in 2026 is $13.99 million per individual ($27.98 million for married couples) — Roth IRAs provide an additional estate planning advantage: they pass to heirs income-tax-free.

Heirs who inherit a traditional IRA must deplete it within 10 years (under SECURE 2.0 rules) and pay ordinary income tax on every distribution. A Roth IRA inherited under the same rules generates no income tax on qualified distributions. For a $2M inherited IRA, that difference can represent $500,000 or more in additional wealth retained by your family.

Pair your roth conversion ladder with charitable strategies — Qualified Charitable Distributions (QCDs) from IRAs after age 70½, Charitable Remainder Trusts (CRTs), or Donor-Advised Funds — to further manage taxable income in the conversion window. You can review IRS guidance on QCDs at IRS.gov.

Roth Conversion Ladder: Head-to-Head Comparison

The table below illustrates how different strategies compare for a married HNW retiree with a $3M traditional IRA, age 62, with a 10-year gap before RMDs. Consult a qualified tax and financial planning professional before drawing conclusions for your own situation.

| Strategy | Projected RMD at 73 | Est. Lifetime Tax Cost | Heir Tax Burden | IRMAA Risk |

|---|---|---|---|---|

| No conversions (status quo) | $180,000+/yr | Very High (32%–37%) | High (10-year depletion rule) | High |

| Roth conversion ladder (22%–24% bracket) | Significantly reduced | Moderate (22%–24%) | Low to None | Managed with precision |

| Lump-sum conversion (all at once) | Eliminated | Extreme (37%+ in conversion year) | None | Severe in conversion year |

| QCD strategy (age 70½+) combined with partial conversions | Moderately reduced | Low to Moderate | Low | Low if well-structured |

| No action + charitable bequest of IRA | Full RMDs during life | High (during lifetime) | None (charity is tax-exempt) | High |

Common Roth Conversion Ladder Mistakes HNW Retirees Make

Converting Too Much in a Single Year

The single most common mistake is over-converting in a given year — either by ignoring IRMAA cliffs or by triggering the 3.8% Net Investment Income Tax (NIIT) surtax on top of regular income tax. A $400,000 conversion sounds aggressive and productive. But if it pushes MAGI over the NIIT threshold ($250,000 for MFJ in 2026) on top of existing investment income, the effective marginal rate can exceed 40% on the top dollars converted.

Bigger is not always better with a roth conversion ladder. Disciplined, bracket-aware conversions consistently outperform large one-time conversions. You can review NIIT rules at IRS Topic 559.

Ignoring the 5-Year Rule

Each Roth conversion starts its own 5-year clock for penalty-free access to converted principal (if you are under 59½). For retirees over 59½, this is less relevant — but for executives who retire early at 55–58, the sequencing of conversions and withdrawals matters. A roth conversion ladder built for an early retiree must account for which conversion “rungs” will be accessible without penalty in which years.

Failing to Pay Conversion Taxes from Non-IRA Funds

If you withhold taxes from the conversion itself — rather than paying from taxable accounts — you effectively reduce the amount that enters the Roth IRA. On a $200,000 conversion, withholding 24% means only $152,000 lands in the Roth. Paying the $48,000 in taxes from a separate taxable account keeps the full $200,000 compounding tax-free. Paying conversion taxes from outside the IRA is a critical execution detail that significantly affects long-term outcomes.

Not Revisiting the Plan Annually

A roth conversion ladder is not a set-it-and-forget-it plan. Tax law changes, income surprises, investment gains, and life events (business sale, inheritance, property sale) all affect the optimal conversion amount in any given year. Annual recalibration with a qualified advisor is essential.

How Davies Wealth Management Structures the Roth Conversion Ladder

A Coordinated, Fiduciary Approach

In my experience working with executives and retirees who come to us after outgrowing their national brokerage firm, the roth conversion ladder is almost always underutilized — or executed without the sophistication the situation demands. We see clients with $4M in IRAs who were told to convert $50,000 a year, with no modeling for IRMAA, no coordination with their estate plan, and no integration with their Social Security claiming strategy.

As a fee-based fiduciary RIA, Davies Wealth Management is compensated to give advice that serves your interests — not to sell products or generate transaction revenue. Our comprehensive wealth management services integrate tax planning, investment management, estate coordination, and retirement income design into a single cohesive plan.

Your roth conversion ladder is not a standalone tax trick. It is one component of a multi-decade wealth strategy. For more information on how to connect with our team, you can schedule a discovery conversation at any time.

We work with CPAs and estate attorneys as part of an integrated team — because the tax projections that drive conversion decisions require collaboration across disciplines. Research from Morningstar’s research on financial planning value consistently shows that coordinated tax planning is among the highest-value activities a financial advisor can deliver.

Frequently Asked Questions: Roth Conversion Ladder

What is a roth conversion ladder and how does it work for retirees?

A roth conversion ladder is a multi-year strategy of systematically converting pre-tax IRA or 401(k) funds into a Roth IRA in annual increments calibrated to your tax bracket. Retirees use the low-income gap years before RMDs begin to convert at lower rates, reducing lifetime taxes and creating a tax-free inheritance for heirs. Each year’s conversion is a deliberate step sized to maximize tax efficiency without triggering costly income thresholds.

How much should a high-net-worth retiree convert each year?

There is no universal answer — the right annual conversion amount depends on your total income picture, filing status, IRMAA thresholds, state taxes, and estate goals. For many HNW married couples in the 2026 gap-year window, conversions of $150,000–$300,000 per year can be optimal, but this must be modeled precisely. Consult a qualified tax and financial planning professional to determine the right amount for your situation.

Does a roth conversion ladder affect Medicare IRMAA premiums?

Yes — conversions increase your MAGI, which determines IRMAA surcharges two years later. Crossing an IRMAA income threshold can add thousands of dollars in Medicare Part B and Part D premiums annually. A well-structured roth conversion ladder accounts for these tiers explicitly and keeps conversions just below trigger points when the math warrants it.

What is the 5-year rule for roth conversions and when does it matter?

Each Roth conversion creates a separate 5-year holding period before converted principal can be withdrawn penalty-free (for those under age 59½). For retirees over 59½, this rule generally does not restrict access to converted funds. However, early retirees who execute a roth conversion ladder beginning in their mid-to-late 50s need to sequence conversions so that accessible funds align with their income needs each year.

Can a roth conversion ladder help with estate planning?

Absolutely. Roth IRAs inherited by non-spouse beneficiaries must be depleted within 10 years under current law, but qualified distributions are income-tax-free — a significant advantage over traditional IRAs. Converting during your lifetime reduces the income tax burden your heirs would otherwise face. Combined with strategies like dynasty trusts or charitable remainder trusts, a roth conversion ladder can dramatically improve multi-generational wealth outcomes.

Take the Next Step

The roth conversion ladder is not a strategy you stumble into. It requires careful year-by-year modeling, integration with your full tax picture, and consistent recalibration as income events change. For high-net-worth retirees with $1M or more in tax-deferred accounts, executing this strategy well — or failing to execute it at all — can be worth hundreds of thousands of dollars in lifetime and generational wealth.

If you are in or approaching the gap years between retirement and age 73, now is the time to act. The window is finite, and every year without a plan is a year of opportunity that cannot be recovered. To avoid making a costly error, learn about the one critical mistake to avoid when you retire before finalizing your strategy.

Ready to see how IRMAA thresholds and Roth conversion planning interact for your specific income levels? Download our comprehensive Medicare IRMAA Planning Guide — it walks through the exact income tiers, surcharge amounts, and planning strategies that sophisticated retirees need to know.

Download our Medicare IRMAA Planning Guide →

Ready for personalized guidance from a fee-based fiduciary? Book a complimentary phone call and let’s map out your roth conversion ladder strategy together.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

Listen & Watch

Prefer audio or video? We’ve got you covered.

Leave a Reply