Digital assets have revolutionized the financial landscape, but they’ve also introduced new complexities in taxation. At Davies Wealth Management, we’ve seen firsthand how confusing digital assets taxation can be for investors.

This guide will walk you through the essentials of navigating the tax implications of cryptocurrencies, NFTs, and other digital assets. We’ll cover everything from understanding taxable events to reporting requirements, helping you stay compliant and avoid potential pitfalls.

What Are Digital Assets in Tax Terms?

The IRS Definition of Digital Assets

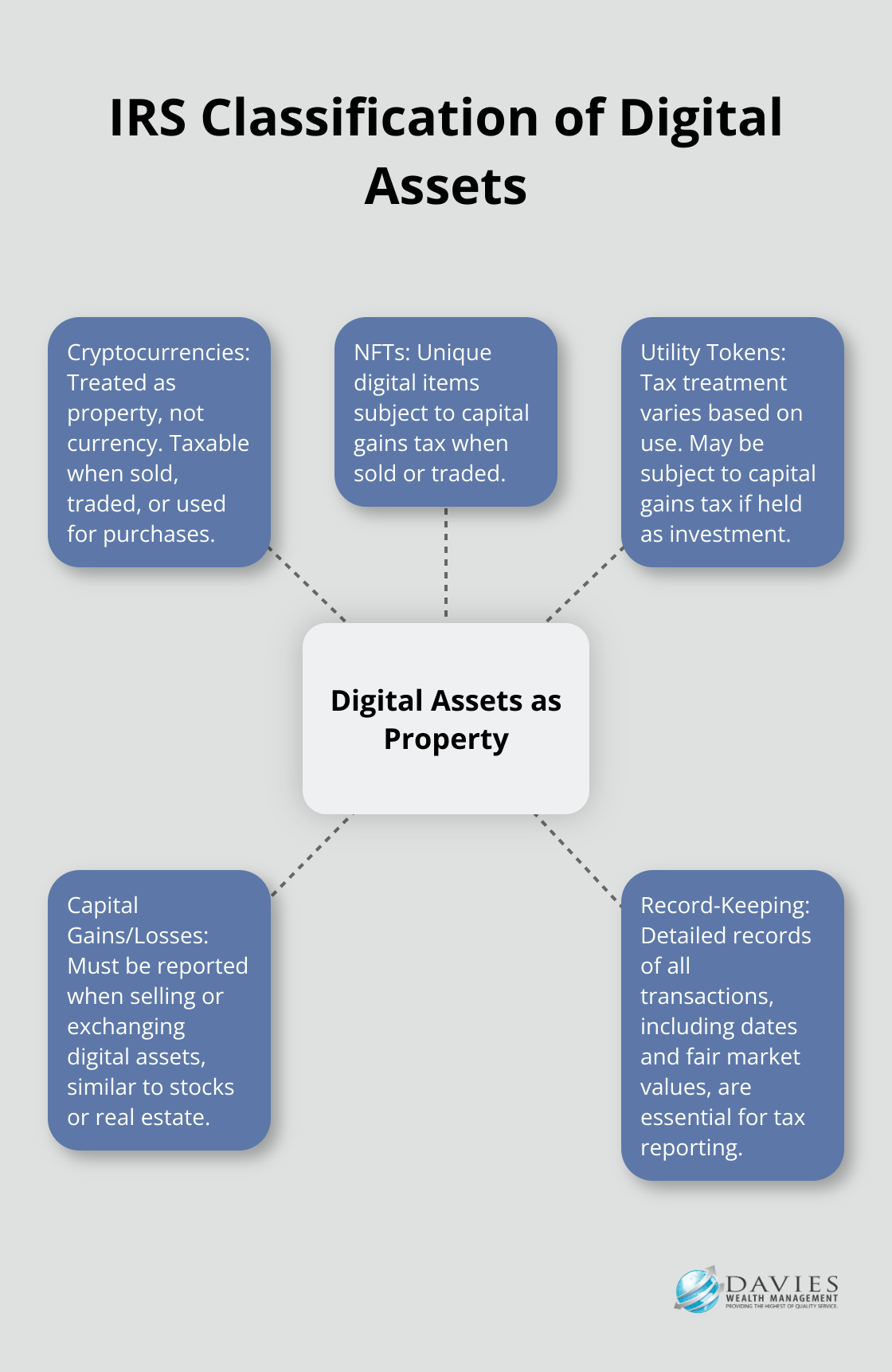

The Internal Revenue Service (IRS) defines digital assets as any digital representation of value recorded on a cryptographically secured distributed ledger or similar technology. This broad definition includes cryptocurrencies (like Bitcoin and Ethereum), non-fungible tokens (NFTs), and other digital tokens.

Types of Digital Assets and Their Tax Treatment

Cryptocurrencies

Cryptocurrencies are the most common type of digital asset. Digital assets, like cryptocurrencies and NFTs, are considered property, not currency, and their income is taxable. This includes:

- Buying goods or services with cryptocurrency

- Trading one cryptocurrency for another

- Selling cryptocurrency for fiat currency

Non-Fungible Tokens (NFTs)

NFTs represent ownership of unique digital items. When sold or traded, they are subject to capital gains tax. The tax treatment can become complex, especially when determining the fair market value of unique digital art or collectibles.

Utility Tokens

Utility tokens provide access to a product or service. Their tax treatment varies depending on their use:

- If held as an investment: typically subject to capital gains tax

- If used to access a service: tax implications can be more intricate

How the IRS Classifies Digital Assets

The IRS classifies digital assets as property, not currency. This classification has significant tax implications.

When you sell or exchange digital assets, you must report capital gains or losses, similar to stocks or real estate.

You may have to report transactions with digital assets such as cryptocurrency and non-fungible tokens (NFTs) on your tax return.

Record-Keeping for Digital Assets

Accurate record-keeping is essential for digital asset transactions. You should maintain detailed records of:

- Transaction dates

- Amounts involved

- Fair market value in U.S. dollars at the time of each transaction

This documentation is vital for accurate tax reporting and can prevent significant issues during tax season.

The world of digital assets and their taxation continues to evolve rapidly. What applies today may change tomorrow. This dynamic nature of digital asset taxation underscores the importance of staying informed and seeking professional guidance. In the next section, we will explore the specific taxable events related to digital assets and how they impact your tax obligations.

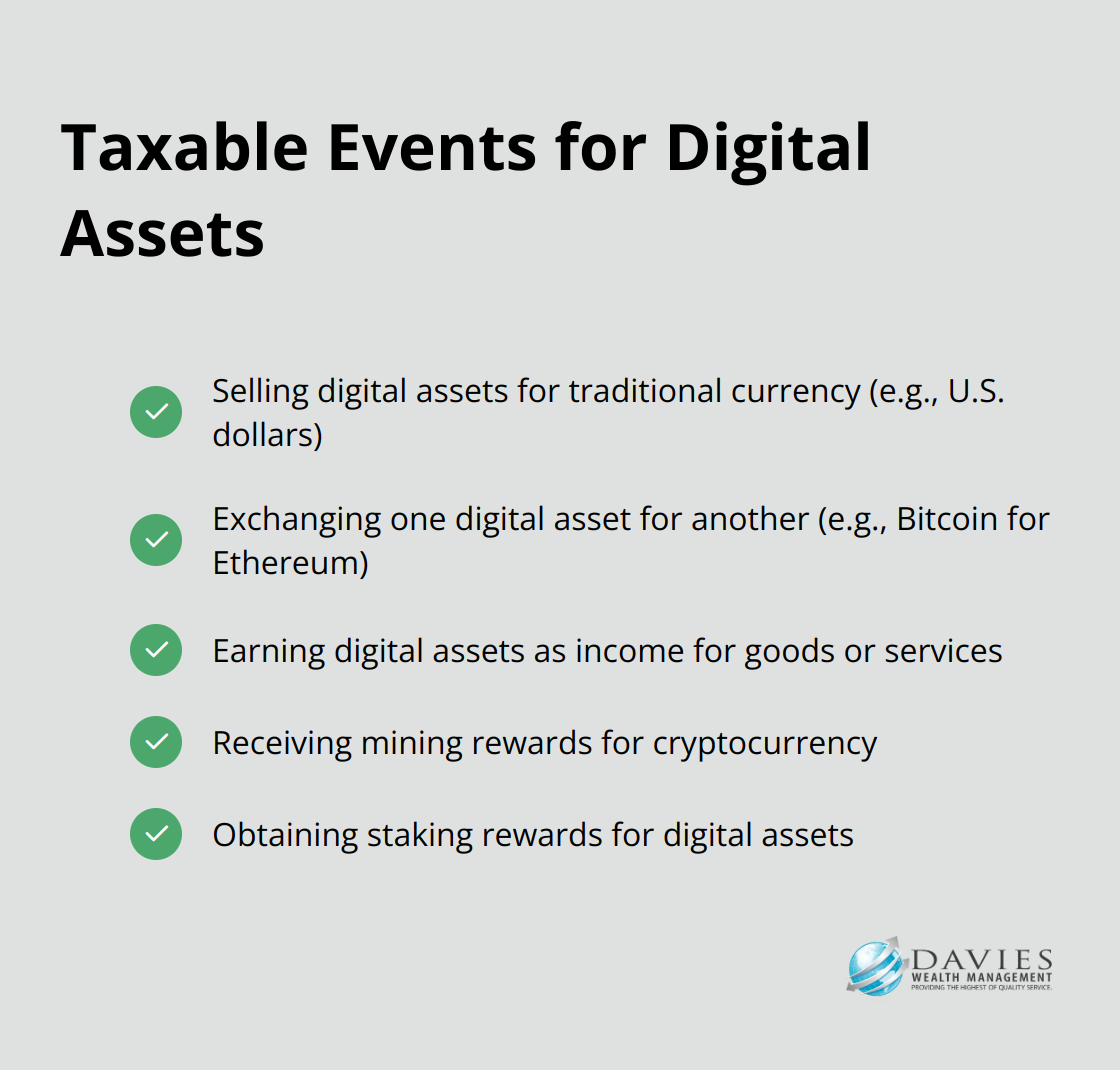

When Do Digital Asset Transactions Trigger Taxes?

Selling Digital Assets for Fiat Currency

The sale of digital assets for traditional currency (like U.S. dollars) creates a taxable event. Your tax obligation depends on the holding period and the difference between your purchase price (cost basis) and sale price. Long-term capital gains rates apply to assets held for more than a year, offering potentially lower tax rates.

For instance, if you purchase 1 Bitcoin for $30,000 and sell it a year later for $40,000, you’ll have a $10,000 long-term capital gain. Your tax rate (0%, 15%, or 20%) will depend on your income bracket.

Exchanging One Digital Asset for Another

Many investors overlook that swapping one cryptocurrency for another is a taxable event. The IRS treats this as a sale of one asset for cash, followed by a purchase of another asset. You must report the capital gain or loss on the asset you trade away.

Consider this scenario: You exchange 1 Ethereum (ETH) for 0.05 Bitcoin (BTC). If your ETH cost $2,000 when acquired and is worth $3,000 at the time of trade, you’ll need to report a $1,000 capital gain, despite not receiving any cash.

Earning Digital Assets as Income

Receiving digital assets as payment for goods or services counts as ordinary income. The fair market value of the digital asset at the time of receipt is your taxable income. This applies to freelancers paid in Bitcoin or employees receiving part of their salary in cryptocurrency.

For example, if a client pays you 0.1 Bitcoin for consulting work, and Bitcoin trades at $35,000 at that time, you’ll report $3,500 as income on your tax return. This amount also becomes your cost basis if you later sell or trade this Bitcoin.

Mining and Staking Rewards

Cryptocurrency miners and stakers often underestimate the tax implications of their activities. When you receive digital assets through mining or staking, the fair market value of those assets at the time of receipt counts as taxable income. If you later sell these assets, you’ll also need to report any capital gains or losses.

Let’s say you mine Ethereum and receive 1 ETH when it’s worth $2,500. You’ll report $2,500 as income. If you later sell that ETH for $3,000, you’ll also report a $500 capital gain.

The Importance of Proper Record-Keeping

Accurate record-keeping is essential for digital asset transactions. Virtual currency is treated as property and general tax principles applicable to property transactions apply to transactions using virtual currency. You should maintain detailed records of transaction dates, amounts involved, and fair market value in U.S. dollars at the time of each transaction. This documentation is vital for accurate tax reporting and can prevent significant issues during tax season.

As the digital asset landscape continues to evolve, staying informed about tax implications becomes increasingly important. Digital asset transactions trigger taxes, and anyone who sold crypto, received it as payment or had other digital asset transactions needs to accurately report it on their tax return. In the next section, we’ll explore the specifics of reporting these transactions and the tools available to help you navigate this complex process.

How to Report Digital Asset Transactions

Record-Keeping Essentials for Digital Assets

Accurate record-keeping forms the backbone of proper tax reporting for digital assets. You must maintain detailed records of every transaction, including:

- Acquisition date

- Cost basis (purchase price plus fees)

- Sale or exchange date

- Sale price or value received in exchange

- Transaction fees

Convert the value to U.S. dollars at the time of each transaction. This step is vital for accurate gain or loss calculations.

IRS Forms for Digital Asset Reporting

The primary forms for reporting digital asset transactions are Form 8949 and Schedule D of Form 1040. On Form 8949, report each individual sale or exchange of digital assets. Provide:

- Property description (e.g., “1 Bitcoin”)

- Acquisition date

- Sale date

- Sale proceeds

- Cost basis

- Gain or loss

After completing Form 8949, transfer the totals to Schedule D, which summarizes your capital gains and losses for the year.

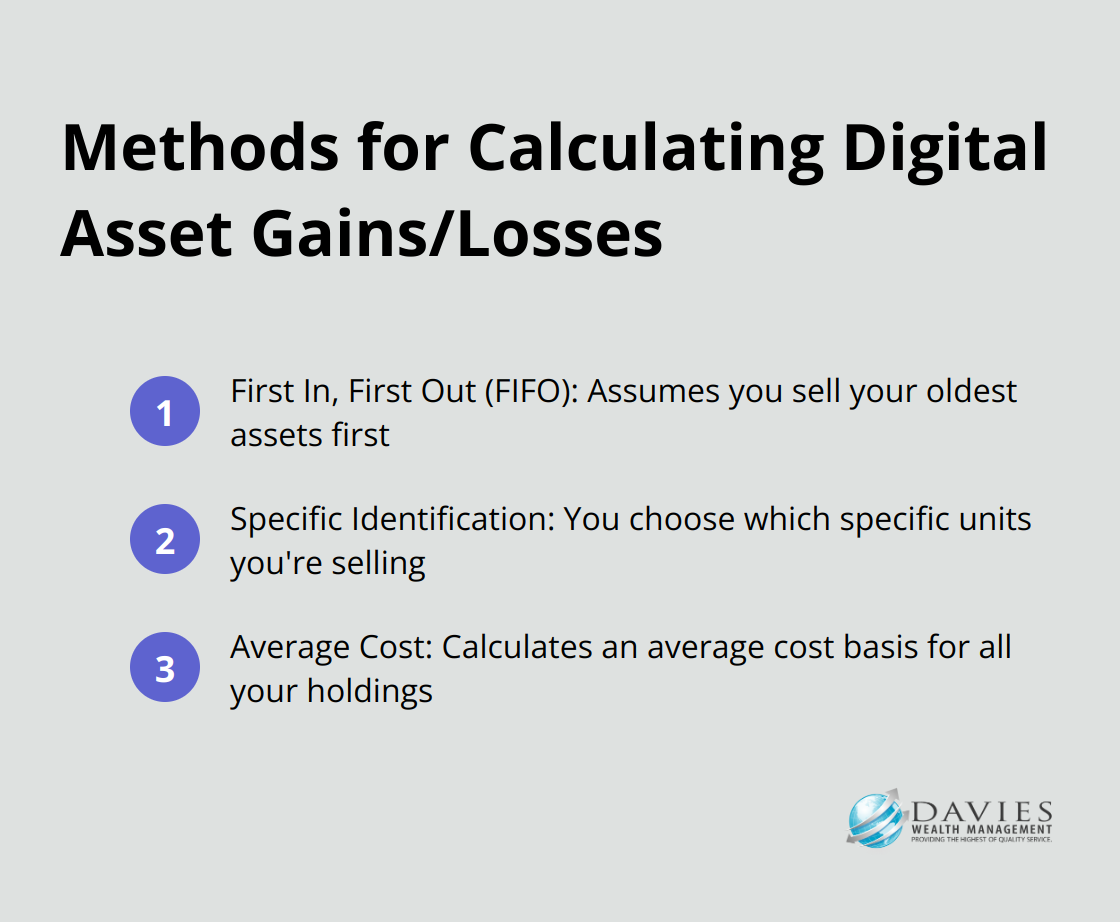

Gain and Loss Calculation Methods

The IRS allows several methods for calculating gains and losses on digital assets:

- First In, First Out (FIFO): Assumes you sell your oldest assets first

- Specific Identification: You choose which specific units you’re selling

- Average Cost: Calculates an average cost basis for all your holdings

Each method can result in different tax outcomes. FIFO might lead to higher gains if asset prices have increased over time, while specific identification allows you to minimize gains by selecting higher-cost units to sell.

Software Tools for Transaction Tracking

Manual tracking of digital asset transactions can be time-consuming and error-prone. Several software tools can simplify this process:

- CoinTracker: Integrates with major exchanges and wallets to automatically track transactions

- TokenTax: Specializes in cryptocurrency tax reporting and offers direct integration with tax filing software

- Koinly: Provides detailed tax reports and supports a wide range of cryptocurrencies and NFTs

These tools can significantly reduce the time and effort required for accurate reporting. However, you must review the generated reports for accuracy, as the responsibility for correct tax reporting ultimately lies with you.

Professional Guidance for Complex Situations

The complexities of digital asset taxation often require professional expertise. A tax professional experienced in digital assets can help you:

- Select the most advantageous calculation method for your situation

- Identify opportunities for tax loss harvesting

- Ensure compliance with the latest IRS guidance on digital assets

Holland & Knight’s Private Wealth Services Digital Assets Team serves the planning needs of clients with digital assets and helps protect their financial interests. This approach helps minimize tax liabilities while ensuring full compliance with IRS regulations.

Final Thoughts

Digital assets taxation presents a complex landscape that requires vigilance and accurate record-keeping. The regulatory environment continues to evolve, making compliance with current tax laws essential for protecting your financial future. Non-compliance can result in severe consequences, including penalties, interest charges, and potential legal action.

Professional guidance often proves invaluable when navigating the intricacies of digital assets taxation. A tax expert can help you understand reporting requirements, identify tax-saving strategies, and meet all your obligations. As governments worldwide address the rapid growth of cryptocurrencies and other digital assets, new guidelines and reporting requirements will likely emerge.

At Davies Wealth Management, we offer expertise to guide you through the complexities of digital assets taxation. Our team can help you make informed decisions about your financial future (whether you’re an experienced investor or new to digital assets). We stand ready to assist you in navigating this evolving landscape with confidence.

Leave a Reply