“`html

Why Social Security Optimization Matters More for High-Income Couples

Social security optimization is one of the most consequential financial decisions high-income couples will ever make — and most get it wrong. For dual-income households in Florida, the difference between a well-timed claiming strategy and a default approach can exceed $100,000 in cumulative lifetime benefits.

Yet many high-net-worth individuals dismiss Social Security as an afterthought. They assume the monthly check is too small relative to their portfolio to warrant serious analysis. That assumption is a costly mistake.

Consider this: a married couple with two high earners may be entitled to combined benefits exceeding $90,000 per year at full retirement age. Over a 25- to 30-year retirement, that represents more than $2 million in guaranteed, inflation-adjusted income. The present value of that income stream rivals a significant portion of most retirement portfolios.

In my experience working with high-income clients across Stuart, Florida and beyond, social security optimization consistently ranks among the highest-impact planning moves — right alongside tax-loss harvesting and Roth conversion strategies.

The Real Cost of Claiming Too Early

Filing for Social Security at age 62 — the earliest possible age — permanently reduces your benefit by up to 30% compared to your full retirement age (FRA). For someone born in 1960 or later, FRA is age 67.

Conversely, delaying benefits past FRA earns 8% per year in delayed retirement credits, up to age 70. That’s a guaranteed, inflation-adjusted return that’s virtually impossible to replicate in today’s markets.

For a high earner entitled to the maximum benefit, the difference between claiming at 62 versus 70 can exceed $1,800 per month — or more than $21,000 per year. Multiply that by two spouses, and the stakes become enormous.

Understanding the Rules That Drive Social Security Optimization

Before diving into specific strategies, it’s essential to understand the foundational rules that govern Social Security benefits for married couples. These rules create the framework within which every social security optimization decision is made.

How Benefits Are Calculated for High Earners

Social Security benefits are based on your Average Indexed Monthly Earnings (AIME) — essentially your highest 35 years of inflation-adjusted earnings. Your AIME is then run through a progressive formula to determine your Primary Insurance Amount (PIA), which is your benefit at full retirement age.

For 2024, the maximum taxable earnings subject to Social Security tax is $168,600. If you’ve consistently earned above this threshold for 35+ years, you’ve maximized your PIA. According to the Social Security Administration, the maximum monthly benefit at FRA in 2024 is $3,822.

For high-income couples where both spouses have strong earnings histories, the combined maximum at FRA approaches $7,644 per month — or nearly $92,000 per year.

Spousal Benefits and Social Security Optimization

A spouse can claim up to 50% of the higher earner’s PIA, regardless of their own work history. However, if the lower-earning spouse has their own benefit that exceeds the spousal amount, they’ll receive their own benefit instead.

Key spousal benefit rules include:

- The higher-earning spouse must have filed for their own benefits before the other spouse can claim a spousal benefit

- Spousal benefits do not earn delayed retirement credits past FRA

- Filing before FRA reduces the spousal benefit proportionally

- Divorced spouses may qualify if the marriage lasted at least 10 years

Survivor Benefits — The Often-Overlooked Factor

Survivor benefits are one of the most powerful — and frequently neglected — elements of social security optimization for couples. When one spouse dies, the surviving spouse receives the higher of the two benefits.

This means the lower benefit disappears entirely. For high-income couples, this can represent a sudden loss of $30,000 to $50,000 or more in annual income, precisely when the surviving spouse may also face higher tax rates due to filing as single.

Planning for survivor benefits is especially critical because one spouse will almost certainly outlive the other. Actuarial data from the Social Security Administration’s period life tables shows that for a couple both age 65, there’s a roughly 50% chance at least one will live past age 90.

7 Proven Strategies for Social Security Optimization

Now let’s explore the specific strategies that high-income Florida couples should consider. Each strategy addresses different circumstances, and the optimal approach depends on factors like age differences, health status, relative earnings, and overall retirement income needs.

Consult a qualified financial professional for your specific situation before implementing any of these strategies.

Strategy 1: The Higher Earner Delays to 70

This is the single most impactful social security optimization strategy for most high-income couples. By having the higher earner delay benefits to age 70, you accomplish two critical goals:

- Maximize the larger benefit by earning three years of 8% delayed retirement credits past FRA

- Lock in the highest possible survivor benefit for the surviving spouse

For a high earner with a PIA of $3,822, delaying from FRA (67) to 70 increases the monthly benefit to approximately $4,740 — an additional $918 per month, or $11,016 per year, for life.

Strategy 2: The Lower Earner Claims at or Near FRA

While the higher earner delays, the lower-earning spouse can file at their own FRA to begin generating household income. This provides cash flow during the three-year window from age 67 to 70 when the higher earner’s benefit hasn’t yet started.

Since the lower earner’s benefit will eventually be replaced by the higher earner’s benefit upon their passing (through survivor benefits), there’s less urgency to maximize this particular benefit through delay.

Strategy 3: Bridge the Gap with Portfolio Withdrawals

High-income couples often have the portfolio assets to fund retirement spending between ages 62 and 70 without needing Social Security income. This “bridge strategy” involves drawing down taxable or tax-deferred accounts during the delay period.

Benefits of this approach include:

- Allowing both Social Security benefits to grow through delayed credits

- Potentially reducing the size of tax-deferred accounts before Required Minimum Distributions (RMDs) begin

- Creating opportunities for Roth conversions during lower-income years

- Reducing future Medicare surcharges (IRMAA) by managing taxable income

Strategy 4: Coordinate with Roth Conversion Planning

The years between retirement and age 70 — often called the “gap years” — present a unique social security optimization opportunity. With no Social Security income and potentially no employment income, your tax bracket may be unusually low.

This creates an ideal window for Roth conversions. By converting traditional IRA assets to Roth during these lower-income years, you can:

- Pay taxes at a lower marginal rate

- Reduce future RMDs

- Lower the amount of Social Security that becomes taxable in later years

- Create tax-free income that doesn’t count toward IRMAA thresholds

The interplay between Roth conversions and Social Security timing is complex. Working with a firm that provides comprehensive wealth management services can help you model these scenarios precisely.

Strategy 5: Account for Florida’s Tax Advantage

Florida residents enjoy a significant edge: no state income tax. This means your Social Security benefits and all other retirement income are taxed only at the federal level.

However, high-income couples still face federal taxation on Social Security. Up to 85% of your benefits become taxable when combined income (adjusted gross income + nontaxable interest + half of Social Security) exceeds $44,000 for married couples filing jointly.

Most high-income Florida couples will hit this threshold easily. Effective social security optimization accounts for this tax reality and integrates withdrawal sequencing to minimize the overall tax burden.

Strategy 6: Factor in IRMAA When Timing Claims

The Income-Related Monthly Adjustment Amount (IRMAA) is a Medicare surcharge that affects higher-income beneficiaries. For 2024, IRMAA kicks in when modified adjusted gross income exceeds $206,000 for married couples filing jointly.

IRMAA is based on your tax return from two years prior. This means income decisions you make today affect Medicare premiums 24 months from now. Social security optimization for high-income couples must account for:

- The timing of large capital gains events

- Roth conversion amounts

- Pension income and Required Minimum Distributions

- Social Security benefit amounts themselves

Strategy 7: Run Multiple Scenario Analyses

No single claiming strategy is right for every couple. The optimal approach depends on dozens of variables. Serious social security optimization requires modeling multiple scenarios using different assumptions for:

- Life expectancy for each spouse

- Investment returns on portfolio assets

- Inflation rates

- Tax law changes

- Healthcare costs

- Legacy goals

Break-even analysis is a starting point, but it’s insufficient on its own. A comprehensive approach considers the total household wealth across all scenarios, not just the Social Security income in isolation.

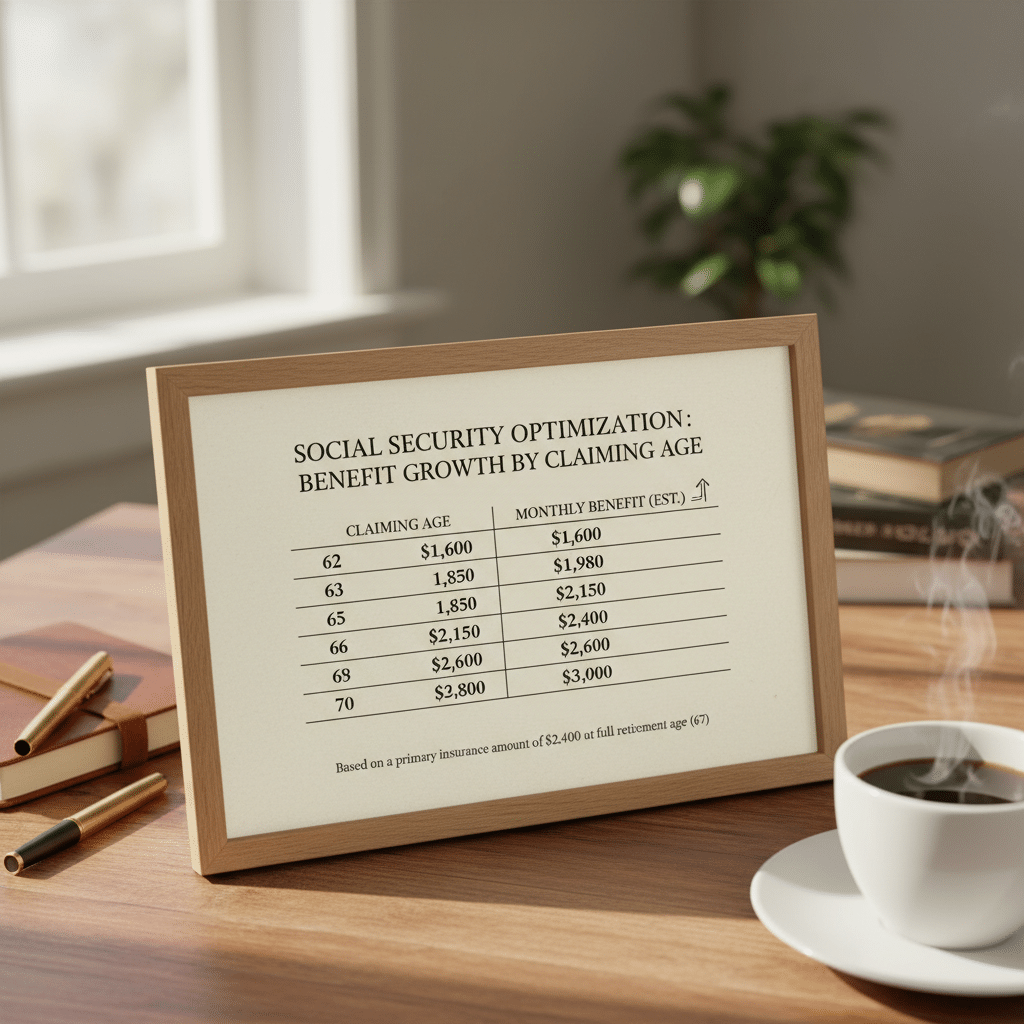

How Claiming Age Affects Your Benefits: A Comparison

The following table illustrates how claiming age impacts monthly and cumulative benefits for a high earner with a PIA of $3,822 (the 2024 maximum at FRA). These figures demonstrate why social security optimization is so powerful.

| Claiming Age | Monthly Benefit | Annual Benefit | Cumulative by Age 85 | Reduction/Increase vs. FRA |

|---|---|---|---|---|

| 62 | $2,710 | $32,520 | $748,000 | -29.2% |

| 64 | $3,121 | $37,452 | $786,500 | -18.3% |

| 67 (FRA) | $3,822 | $45,864 | $825,600 | 0% (baseline) |

| 70 | $4,740 | $56,880 | $852,000 | +24.0% |

Key takeaway: While the cumulative totals converge near age 85, the higher monthly income from delaying provides greater protection against longevity risk, inflation, and the loss of one spouse’s benefit. For high-income couples who don’t need the cash flow immediately, delaying is often the strongest play.

Common Social Security Optimization Mistakes High-Income Couples Make

Even sophisticated investors make avoidable errors with Social Security. Here are the most common mistakes I see among high-income clients.

Mistake 1: Treating Social Security in Isolation

Social Security doesn’t exist in a vacuum. Your claiming decision affects your tax bracket, Medicare premiums, Roth conversion opportunities, portfolio withdrawal rates, and estate plan. Effective social security optimization is integrated with your entire financial picture.

A study published by the National Bureau of Economic Research found that the vast majority of retirees claim Social Security benefits at financially suboptimal times, leaving significant money on the table.

Mistake 2: Both Spouses Claiming at the Same Time

Many couples default to filing simultaneously — often at 62 or at FRA. This ignores the powerful staggering strategies described above. In most cases, having at least one spouse delay to 70 produces a better outcome for the household.

Mistake 3: Ignoring the Survivor Benefit

This is perhaps the most costly oversight. When one spouse dies, the household loses the smaller of the two Social Security checks but also shifts from married filing jointly to single — a significantly less favorable tax bracket.

Planning for the surviving spouse’s financial security is a core pillar of social security optimization. Delaying the higher earner’s benefit effectively purchases a larger “insurance policy” for the surviving spouse.

Mistake 4: Not Accounting for the Earnings Test

If you claim Social Security before FRA and continue working, the retirement earnings test reduces your benefits by $1 for every $2 earned above $22,320 in 2024. In the year you reach FRA, the threshold increases to $59,520, with a $1 reduction for every $3 earned above that amount.

For high-income executives and business owners still generating significant earned income, this can temporarily eliminate much of your Social Security benefit. While the withheld amounts are eventually restored through higher future benefits, the cash flow disruption catches many people off guard.

Mistake 5: Relying Solely on Break-Even Analysis

Break-even analysis — calculating the age at which delayed benefits surpass cumulative early benefits — is a useful starting point, but it dramatically oversimplifies the decision. It ignores taxes, survivor benefits, opportunity costs, and the insurance value of higher guaranteed income.

A more sophisticated approach uses Monte Carlo simulation or present value analysis across a range of scenarios to determine which claiming strategy maximizes total household wealth and minimizes downside risk.

Special Considerations for Florida Executives and Athletes

Our practice works extensively with professional athletes, corporate executives, and business owners — populations with unique social security optimization challenges.

Professional Athletes and Irregular Earnings

Professional athletes often earn substantially above the Social Security taxable maximum during their playing years but may have fewer than 35 years of covered earnings. Since the Social Security formula uses your highest 35 years — and averages in zero-earning years if you don’t have 35 — athletes may have lower PIAs than expected.

Continuing to work in a covered employment capacity after a playing career can replace those zero-earning years and increase your benefit. This consideration should factor into any social security optimization analysis for former athletes.

Executives with Deferred Compensation

Corporate executives with nonqualified deferred compensation (NQDC) plans face a unique timing issue. NQDC distributions are subject to Social Security tax when they vest — not when they’re paid out. Understanding when these amounts were taxed is critical to accurately projecting your future benefit.

Additionally, large NQDC payouts in retirement can push income well above IRMAA thresholds, making the coordination between Social Security claiming and deferred compensation timing especially important.

Business Owners Considering a Sale

If you’re a business owner planning a sale within the next few years, the resulting capital gains can significantly impact your Medicare premiums through IRMAA for the two years following the sale. Coordinating the timing of a business sale with your Social Security claiming strategy — and potentially with tax-efficient income planning — can save tens of thousands of dollars.

Consult a qualified tax professional for your specific situation when planning a business transition.

Frequently Asked Questions About Social Security Optimization

What is social security optimization, and why does it matter for high-income couples?

Social security optimization is the strategic process of determining the best age and method for each spouse to claim Social Security benefits in order to maximize lifetime household income. For high-income couples, the stakes are especially high because both spouses often qualify for substantial individual benefits, and the combined decisions around timing, taxation, and survivor benefits can affect total wealth by $100,000 or more over a retirement.

Should both spouses delay Social Security benefits until age 70?

Not necessarily. While delaying the higher earner’s benefit to 70 is often advantageous for maximizing the survivor benefit, having both spouses delay may not be optimal. In many cases, the lower-earning spouse benefits from claiming at or near full retirement age to provide household cash flow while the higher earner’s benefit continues to grow. The ideal approach depends on your specific ages, health, earnings history, and financial needs.

How does living in Florida affect Social Security optimization strategies?

Florida’s lack of state income tax means Social Security benefits are only subject to federal taxation, which is a meaningful advantage. However, high-income Florida couples will still pay federal tax on up to 85% of their benefits. The state tax savings can be redirected toward delaying benefits, funding Roth conversions during the gap years, or simply enhancing retirement cash flow. Florida residency doesn’t change the claiming strategy itself, but it improves the after-tax value of every dollar received.

At what income level does Social Security become taxable for married couples?

Social Security benefits become partially taxable when “combined income” (adjusted gross income + nontaxable interest + half of Social Security benefits) exceeds $32,000 for married couples filing jointly. Up to 85% of benefits are taxable when combined income exceeds $44,000. Virtually all high-income couples fall into the 85% taxable category, making tax-efficient withdrawal sequencing an essential component of social security optimization.

Can a financial advisor really help maximize Social Security benefits?

Yes. A qualified financial advisor uses specialized software to model hundreds of claiming combinations, integrating Social Security timing with tax projections, portfolio withdrawals, Roth conversions, Medicare costs, and estate planning goals. This holistic analysis goes far beyond what free online calculators provide. To explore how an investment and investment strategy approach works in practice, you can schedule a discovery conversation with our team to review your specific numbers.

Take Control of Your Social Security Strategy Today

For high-income Florida couples, social security optimization isn’t a luxury — it’s a necessity. The decisions you make about when and how to claim will ripple through your tax returns, investment strategy, Medicare costs, and legacy plan for decades to come.

The strategies outlined above — delaying the higher earner’s benefit, coordinating with Roth conversions, accounting for IRMAA, and running comprehensive scenario analyses — represent the foundation of a sound approach. But every couple’s situation is unique, and the best strategy is one tailored specifically to your circumstances.

Don’t leave hundreds of thousands of dollars on the table. Start by understanding where you stand today.

📋 Download our free Retirement Readiness Checklist to evaluate your current plan and identify gaps in your social security optimization strategy. It takes just a few minutes and covers the critical decisions every high-income couple needs to address before filing.

💬 Ready for personalized guidance? Schedule a complimentary review with our team at Davies Wealth Management. We’ll walk through your Social Security statements, model multiple claiming scenarios, and show you exactly how different strategies impact your lifetime wealth.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

“`

Leave a Reply