Here is the full HTML content with internal links added:

Knowing the financial advisor warning signs before you hand over your financial future could be the most valuable thing you do this year. For investors managing $500,000 to $10 million or more, a misaligned or unethical advisor doesn’t just cost you fees — it can cost you decades of compounded growth, unnecessary tax liability, and in the worst cases, your entire portfolio.

In Stuart and the broader Treasure Coast area, we see a wide range of investors: retired executives, professional athletes, business owners who recently sold, and families navigating multi-generational wealth. What many share in common is a frustrating story about a previous advisor who wasn’t transparent, wasn’t qualified, or simply wasn’t working in their best interest.

This guide walks through nine specific financial advisor warning signs that high-net-worth investors should never overlook — and explains what to look for in a relationship that actually protects and grows your wealth.

Why High-Net-Worth Investors Face Greater Advisor Risk

The Stakes Are Fundamentally Different at $1M+

Mass-market financial advice is built around simple accumulation: contribute to your 401(k), buy index funds, don’t panic. That advice is fine for someone with $150,000 in savings. But it fails almost completely when you’re managing a $3 million portfolio, a concentrated stock position, a pending business sale, or a taxable estate approaching the federal exemption.

At higher wealth levels, the complexity multiplies rapidly. You’re dealing with Roth conversion ladders, IRMAA thresholds, qualified opportunity zone investments, charitable remainder trusts, and estate tax cliffs. The wrong advisor — one who lacks the training, the incentive structure, or the transparency — can make costly errors that compound over time.

Why Sophisticated Investors Still Miss Financial Advisor Warning Signs

High earners and successful executives are not immune to advisor fraud or negligence. In fact, research from the U.S. Securities and Exchange Commission shows that financially sophisticated investors are specifically targeted by high-pressure and affinity-based fraud schemes. Confidence in your own intelligence can paradoxically lower your guard.

The most dangerous advisors often present well: polished offices, impressive credentials on the wall, and a reassuring pitch. That’s exactly why knowing specific warning signs matters more than relying on gut instinct.

The 9 Financial Advisor Warning Signs You Should Never Ignore

Warning Sign 1: They Cannot Clearly State Whether They Are a Fiduciary

This is the most fundamental financial advisor warning sign. A fiduciary is legally and ethically required to act in your best interest — not their firm’s interest, not their quota’s interest, yours. Ask any prospective advisor directly: “Are you a fiduciary 100% of the time for all services you provide?”

Many advisors operate under a suitability standard instead, which only requires that a recommendation be “suitable” for a client — not necessarily the best option available. The difference between these two standards can translate to tens of thousands of dollars in unnecessary commissions or inferior products over a decade.

If an advisor hesitates, qualifies their answer, or says they’re “sometimes” a fiduciary, that’s a red flag. Consult a qualified financial professional to verify the legal standard your advisor is held to before signing anything.

Warning Sign 2: Vague or Evasive Answers About Compensation

How your advisor is paid shapes every recommendation they make. This is not a cynical statement — it’s structural reality. Advisors who earn commissions on products they sell have an inherent conflict of interest, even when they’re trying to act ethically.

Here are the most common compensation structures and what to watch for:

- Fee-only: Paid directly by you (flat fee, hourly, or AUM percentage). No commissions. This is the cleanest structure for HNW clients.

- Fee-based: Earns fees AND may earn commissions. Requires careful scrutiny of when commissions apply.

- Commission-only: Paid entirely through product sales. Highest conflict of interest.

According to NerdWallet’s guide to fiduciary advisors, many investors don’t realize their advisor earns commissions until they see the fine print of a product they’ve already purchased. Ask for a full written disclosure of all compensation before you proceed.

Warning Sign 3: They Push Proprietary Products or Annuities Without Full Disclosure

One of the clearest financial advisor warning signs is an advisor who consistently steers you toward proprietary mutual funds, variable annuities, or insurance products — particularly when you didn’t ask about them.

Some annuities are appropriate for certain situations. But variable annuities can carry surrender charges of 7–10% for up to 10 years, internal expense ratios of 2–3% annually, and complex riders that few investors fully understand. For a $1 million investment, a 2.5% annual expense ratio costs $25,000 per year — every year, regardless of performance.

The SEC’s investor guide on variable annuities explicitly warns that these products are frequently sold to investors for whom simpler, lower-cost alternatives would be more appropriate. If your advisor recommends an annuity, ask them to put in writing why it’s better than a comparable low-cost alternative. Their response will tell you a great deal.

Warning Sign 4: No Written Investment Policy Statement or Financial Plan

A serious advisor builds a written roadmap. If you’ve been working with someone for more than three months and still don’t have a documented investment policy statement (IPS) or a comprehensive financial planning document, that is a significant financial advisor warning sign.

For high-net-worth clients, a proper plan should address:

- Asset allocation aligned with your specific risk tolerance and time horizon

- Tax-efficient withdrawal sequencing

- Roth conversion strategy (especially relevant given current 2026 tax brackets)

- IRMAA planning for Medicare Part B and D premiums

- Estate plan coordination including trust structures

- Concentrated stock or business exit strategy if applicable

Without a written plan, there’s no accountability, no benchmark, and no way to evaluate whether your advisor’s decisions serve your goals or their own.

Warning Sign 5: Promises of Consistent Above-Market Returns

Any advisor who promises — explicitly or implicitly — that they can consistently beat the market is either misleading you or misleading themselves. Research from Morningstar consistently shows that the majority of actively managed funds underperform their benchmarks over 10+ year periods after fees, a finding supported by the Morningstar Active/Passive Barometer.

This is not to say active management is never appropriate for HNW clients. Tax-loss harvesting, direct indexing, and alternative investment strategies can add real value in the right context. But the value proposition should be about tax efficiency, risk management, and planning — not promises of alpha that statistically don’t exist.

If an advisor shows you a track record that seems too good to be true, ask how it was calculated, whether it’s audited, and how it compares to an appropriate benchmark net of all fees.

Warning Sign 6: Ignoring Tax Implications of Every Major Decision

Taxes are often the largest single cost a high-net-worth investor faces — larger than advisor fees, larger than fund expenses, and sometimes larger than market losses. An advisor who doesn’t proactively discuss tax strategy is leaving serious money on the table.

In 2026, with the federal estate tax exemption having sunset from its elevated TCJA levels, the stakes are especially high. Depending on your estate size, failing to act on portability elections, annual gifting strategies ($19,000 per recipient in 2026), or qualified charitable distributions could cost your family hundreds of thousands of dollars.

Watch for these specific omissions:

- Never discussing Roth conversions despite your income potentially dropping in retirement

- Failing to coordinate portfolio rebalancing with tax-loss harvesting

- Not addressing IRMAA cliffs that affect Medicare premiums two years after high-income years

- Ignoring the tax treatment of business sale proceeds

- No discussion of charitable strategies like donor-advised funds or qualified opportunity zones

Consult a qualified tax professional in conjunction with your financial advisor to ensure your plan is fully coordinated.

Warning Sign 7: You Receive Statements You Don’t Understand

Complexity can be a tool of concealment. If your quarterly statements are so dense that you cannot identify what you own, what you paid in fees, and how your portfolio has performed against a relevant benchmark — that is a financial advisor warning sign worth taking seriously.

Every client deserves a clear, plain-language explanation of:

- Total fees paid in dollars (not just percentages)

- Performance compared to an appropriate benchmark

- What has changed in the portfolio and why

- Tax events triggered during the period

Transparency is not optional. It’s the baseline standard for any professional managing your assets.

Warning Sign 8: Frequent and Unexplained Trading (Churning)

Churning — the practice of excessive trading to generate commissions — remains one of the most documented forms of advisor misconduct. In a commission-based account, each trade can generate revenue for the advisor regardless of whether it benefits you.

Signs to watch for include: a portfolio that looks significantly different every time you review it, high short-term capital gains showing up on your taxes, or an advisor who can’t clearly explain why each trade was made. The IRS taxes short-term capital gains at ordinary income rates — which for HNW investors in 2026 can reach 37%. Unnecessary trades can be extraordinarily expensive.

You can check an advisor’s complaint history and disciplinary record for free using SEC’s EDGAR database or FINRA’s BrokerCheck tool.

Warning Sign 9: Resistance to Outside Review or Collaboration

A confident, ethical advisor welcomes a second opinion. They will readily collaborate with your CPA, estate attorney, or family office. If your advisor becomes defensive, dismissive, or discouraging when you mention bringing in another professional — that reaction itself is one of the most telling financial advisor warning signs.

High-net-worth wealth management is inherently a team sport. Tax strategy, estate planning, risk management, and investment management must be coordinated. An advisor who positions themselves as the only person you need is either overestimating their competence or protecting their turf — neither of which serves you.

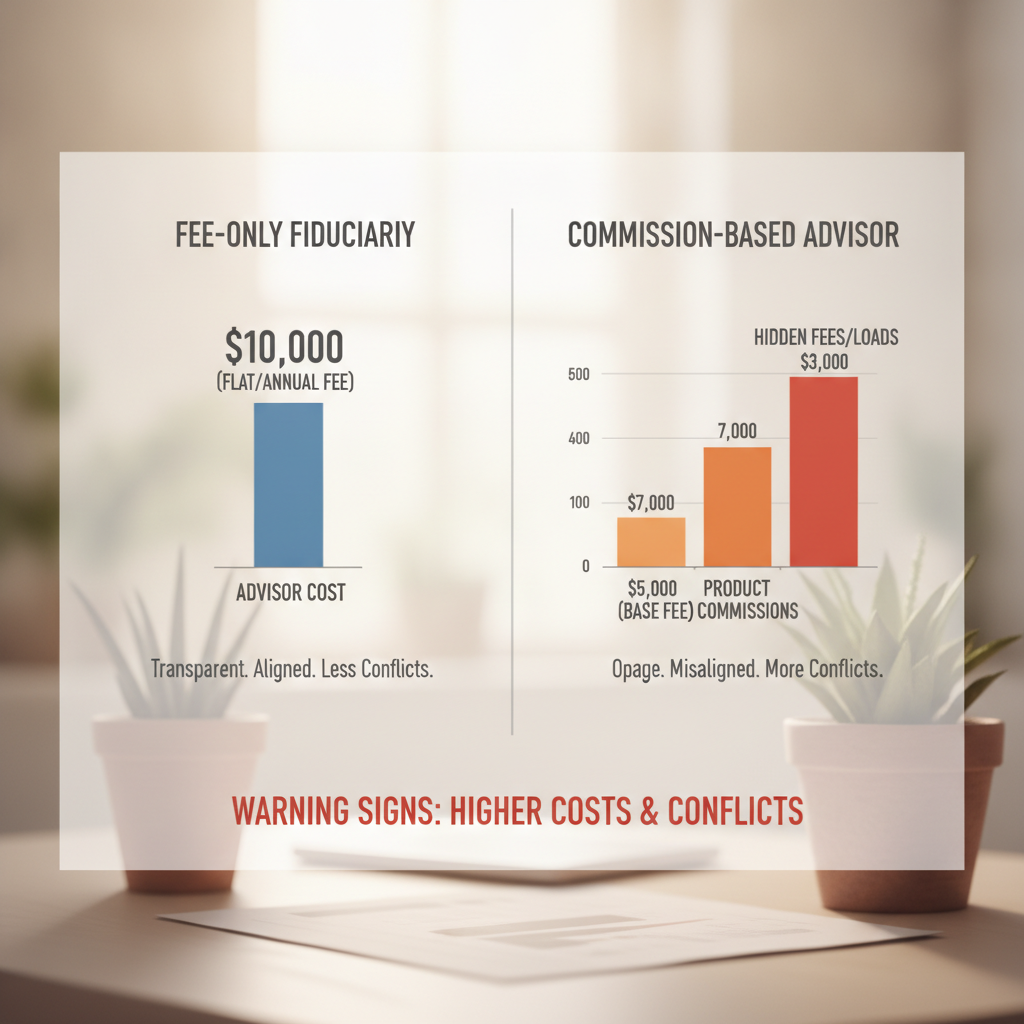

How Fee-Based Fiduciary Advisors Compare to Commission-Based Advisors

The table below illustrates why the advisor structure matters — not just in principle, but in real dollars for HNW investors.

| Factor | Fee-Only Fiduciary RIA | Commission-Based Broker |

|---|---|---|

| Legal Standard | Fiduciary — must act in client’s best interest at all times | Suitability — recommendation must be “suitable,” not necessarily best |

| Compensation | Paid by client (AUM fee or flat fee); no commissions | Earns commissions on products sold; potential conflicts of interest |

| Product Shelf | Access to entire market; no proprietary products to push | May favor in-house funds or products with higher commissions |

| Tax Strategy Integration | Typically coordinated with CPA; proactive tax planning | Often siloed; tax planning not typically part of service model |

| Transparency | Full fee disclosure required; ADV Part 2 publicly available | Disclosure requirements vary; commissions may not be clearly itemized |

| Regulatory Oversight | Registered with SEC or state; Form ADV publicly filed | Registered with FINRA; BrokerCheck record publicly available |

For a $3 million portfolio, the difference between a 1% fee-only advisor and a commission-based relationship generating 2.5% in total costs adds up to $45,000 per year — and substantially more in compounded impact over a 20-year retirement. Consult a qualified financial professional to evaluate the full cost structure of any advisory relationship.

What to Do If You Recognize These Financial Advisor Warning Signs

Step 1: Request Full Written Disclosure

Ask your current advisor for their Form ADV Part 2 — every registered investment adviser is required to provide this document, which discloses conflicts of interest, compensation structure, and disciplinary history. If they can’t produce it or seem unfamiliar with it, that alone tells you something important.

Step 2: Get a Fee Audit

Pull together your last 12 months of statements and add up every dollar paid in fees — advisory fees, fund expense ratios, transaction costs, and any insurance product charges. Many HNW investors are genuinely shocked when they see the full number. Our comprehensive wealth management services include a transparent fee structure designed specifically for clients who have outgrown the one-size-fits-all model.

Step 3: Seek a Second Opinion Without Obligation

A reputable fiduciary firm will review your current situation without pressuring you to move assets. The goal of a second opinion is clarity — understanding whether your current plan is truly optimized for your goals, tax situation, and estate needs. If you’re in the Stuart, Florida area or work with a Treasure Coast-based advisor, we encourage you to schedule a discovery conversation to explore what a different approach might look like for your specific situation.

Frequently Asked Questions About Financial Advisor Warning Signs

What is the most important financial advisor warning sign for a high-net-worth investor?

The inability — or unwillingness — to clearly confirm they are a full-time fiduciary is the single most critical financial advisor warning sign for wealthy investors. At $1 million or more in investable assets, the difference between a fiduciary standard and a suitability standard can cost tens of thousands of dollars over time in avoidable fees, inferior products, and missed tax strategies.

How can I verify whether my financial advisor has a disciplinary history?

You can check any registered investment adviser’s record through the SEC’s Investment Adviser Public Disclosure database at adviserinfo.sec.gov, and broker-dealers through FINRA’s BrokerCheck at brokercheck.finra.org — both are free and publicly available. Look for complaints, regulatory actions, or frequent employer changes, which can indicate patterns of misconduct.

Is it normal for a financial advisor to discourage a second opinion?

No — and resistance to outside review is itself one of the clearest financial advisor warning signs. A confident, ethical advisor has nothing to hide and welcomes collaboration with your CPA or estate attorney. Defensiveness about a second opinion should immediately raise your level of scrutiny.

What should a high-net-worth investor expect to pay for a fee-only fiduciary advisor?

Fee-only RIAs typically charge between 0.5% and 1.25% of assets under management annually, depending on portfolio size and service complexity, with larger portfolios often receiving lower percentage rates. For a $5 million portfolio, a well-structured advisory relationship at 0.75% costs $37,500 per year — a fraction of what unnecessary commissions, tax inefficiency, or poor product selection can cost over the same period. Always ask for the total all-in cost, including fund expenses.

How do financial advisor warning signs differ for retirees versus pre-retirees?

Retirees should be especially alert to advisors who fail to address IRMAA planning, Social Security optimization, required minimum distributions, and tax-efficient withdrawal sequencing — gaps that can silently cost thousands annually. Pre-retirees with significant assets should watch for advisors who treat their 401(k) as the entire plan without addressing taxable accounts, stock options, business interests, or estate structure. In both cases, the absence of a written, comprehensive financial plan is a fundamental red flag regardless of life stage.

Working With a Fiduciary Advisor in Stuart, Florida

At Davies Wealth Management, we work exclusively as a fee-based fiduciary RIA serving high-net-worth individuals, executives, professional athletes, and business owners. Our clients come to us because they’ve outgrown their broker, their national wirehouse, or their advisor who treats a $3 million portfolio the same as a $300,000 one.

We don’t sell products. We don’t earn commissions. Every recommendation we make is filtered through one question: is this in the client’s best interest, tax-adjusted, risk-adjusted, and aligned with their long-term goals? That standard — not as a marketing tagline but as a legal and ethical obligation — is what we believe every high-net-worth investor deserves.

Recognizing financial advisor warning signs is the first step. Taking action on them is what separates the investors who protect their wealth from those who discover the problem only after significant damage has been done.

Take the Next Step

Not sure if your current advisor relationship is truly optimized for your situation? Start by taking our Financial Wellness Quiz — a quick, no-obligation assessment designed to help high-net-worth investors identify gaps in their current financial strategy, including whether their advisor relationship is structured in their best interest.

→ Take our Financial Wellness Quiz and get a personalized snapshot of where your plan stands today.

Already know you want a different conversation? Ready for personalized guidance from a fee-based fiduciary? Book a complimentary phone call. There’s no obligation — just a direct conversation about whether our approach is a fit for your goals.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

Leave a Reply