“`html

Why a Roth Conversion Ladder Matters More Than Ever for High-Net-Worth Retirees

A Roth conversion ladder is a systematic, multi-year strategy for moving assets from a traditional IRA or 401(k) into a Roth IRA — converting just enough each year to fill specific tax brackets while avoiding unnecessary spikes in your marginal rate. For retirees with $1 million to $10 million or more in tax-deferred retirement accounts, it may be the single most impactful tax-planning tool available.

Why does this strategy demand attention right now? The answer lies in a convergence of factors: historically favorable individual tax rates under the Tax Cuts and Jobs Act (TCJA), which are currently scheduled to sunset after December 31, 2025, the potential for higher rates in future years, and the looming impact of Required Minimum Distributions (RMDs) that can push affluent retirees into the highest brackets. For 2026, the landscape is shifting — and a well-designed Roth conversion ladder is one of the best defenses.

Key point: Mass-market investors rarely face this problem. If your traditional IRA balance is $150,000, the tax savings from a conversion ladder are modest. But when your balance exceeds $1 million — or when combined household retirement accounts reach $3 million to $5 million — the compounding effect of decades of tax-free growth and the elimination of RMDs can be worth hundreds of thousands of dollars over a retirement spanning 25 to 35 years.

How a Roth Conversion Ladder Works: The 7-Step Framework

At its core, a Roth conversion ladder is elegant in concept but demanding in execution. Here are the seven steps that form the foundation of a successful multi-year strategy.

Step 1: Quantify Your Tax-Deferred Exposure

Begin by calculating the total value of all traditional IRAs, rollover IRAs, SEP-IRAs, SIMPLE IRAs, and pre-tax 401(k)/403(b) accounts across both spouses. This is your “tax-deferred exposure” — the pool of money that will eventually be taxed as ordinary income, whether through voluntary conversions or mandatory RMDs.

For a couple with $3.5 million in combined pre-tax retirement accounts, the eventual tax liability at a blended federal rate of 32% could exceed $1.1 million. A Roth conversion ladder aims to shrink that number by converting strategically in lower-rate years.

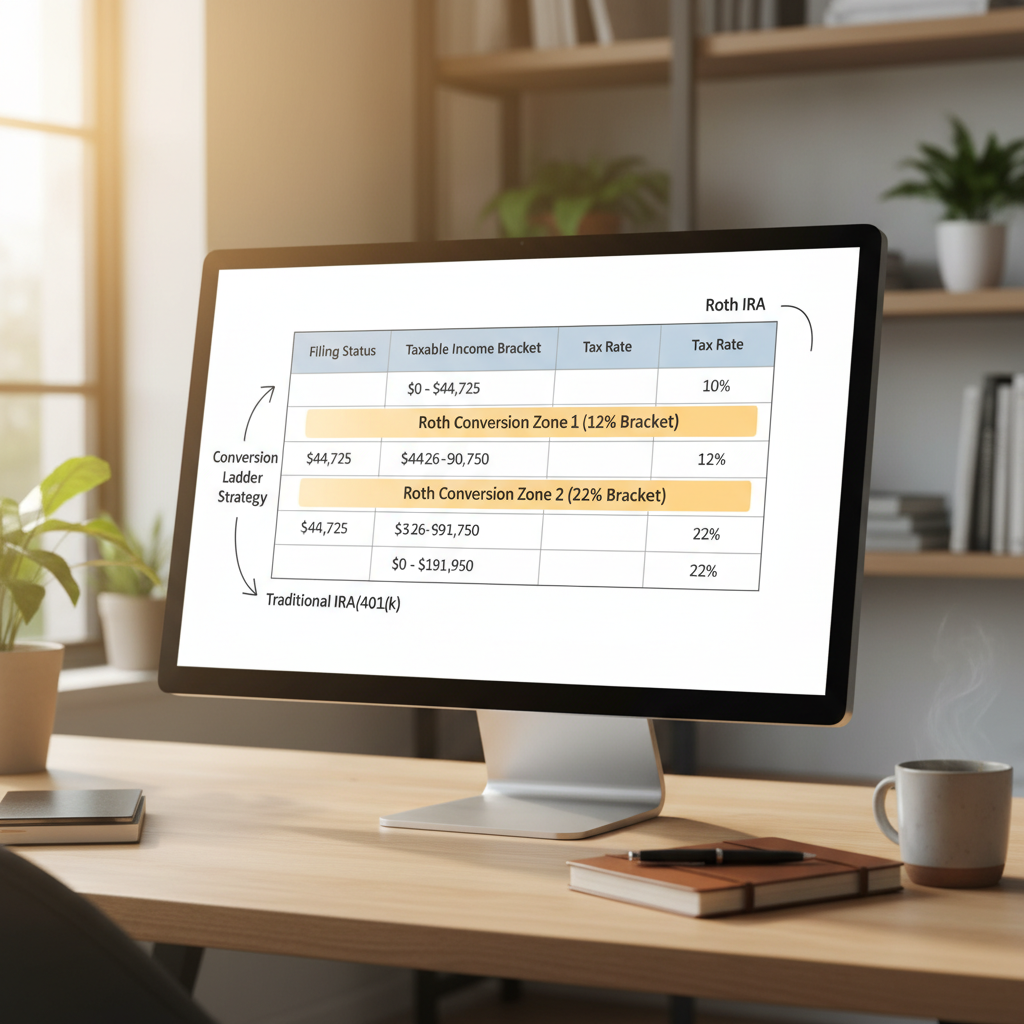

Step 2: Map Your Roth Conversion Ladder to Tax Brackets

The 2026 tax year brings important changes. With the TCJA provisions expiring (absent new legislation), the IRS federal income tax brackets are expected to revert to pre-TCJA levels, adjusted for inflation. For married filing jointly in 2026, the top marginal rate returns to 39.6% on taxable income above approximately $609,350 (projected).

The goal is to convert enough each year to “fill up” a target bracket — often the 24% or 32% bracket — without spilling into the next one. This requires projecting all income sources: Social Security, pensions, rental income, dividends, and capital gains.

Step 3: Establish a Conversion Window Based on Retirement Age

The most valuable conversion window often falls between retirement and age 73 (when RMDs begin for most retirees under current rules). During these years, taxable income may be lower — especially if Social Security is delayed to age 70 and pension income hasn’t started.

For a 62-year-old executive who has just retired, there may be an 11-year window of reduced income before RMDs kick in. That’s 11 opportunities to execute rungs on a Roth conversion ladder at favorable rates.

Step 4: Coordinate with Social Security Timing

Social Security benefits become up to 85% taxable once combined income exceeds certain thresholds. Aggressive Roth conversions during the years before you claim Social Security can reduce the future tax drag on those benefits. Conversely, converting too much in a year when you’re already collecting Social Security can make more of those benefits taxable.

Step 5: Model IRMAA Surcharges Into Every Roth Conversion Ladder Decision

One of the most frequently overlooked costs of Roth conversions for high-net-worth retirees is the Income-Related Monthly Adjustment Amount (IRMAA). Medicare Part B and Part D premiums increase significantly once Modified Adjusted Gross Income (MAGI) exceeds specific thresholds. For 2026, the first IRMAA surcharge tier for married couples filing jointly is projected at approximately $206,000 in MAGI (based on 2024 income reported on your tax return).

A $300,000 Roth conversion could push a couple into the third or fourth IRMAA tier, adding $6,000 to $12,000+ in annual Medicare surcharges per couple. This cost must be weighed against the long-term tax savings. Consult a qualified tax professional for your specific situation.

Step 6: Fund the Tax Bill from Non-Retirement Assets

One critical rule: never pay the conversion tax from the converted funds themselves. Doing so dramatically reduces the compounding benefit. For a $400,000 conversion at a 32% effective rate, the tax bill is approximately $128,000. That should come from a taxable brokerage account, cash reserves, or other non-retirement sources.

This is why a Roth conversion ladder is primarily a strategy for high-net-worth retirees — you need sufficient liquid assets outside your IRA to cover the tax cost without dipping into the converted funds.

Step 7: Reassess Annually and Adjust the Ladder

A Roth conversion ladder is not a set-it-and-forget-it strategy. Every year, you must reassess based on:

- Actual investment returns (a down year may present a larger conversion opportunity)

- Changes in tax law or bracket thresholds

- Unexpected income events (sale of property, business distributions, large capital gains)

- Changes in estate planning goals

- Updated IRMAA projections

In our experience working with clients, the annual recalibration is where the most value is created — and where many do-it-yourself approaches fall short.

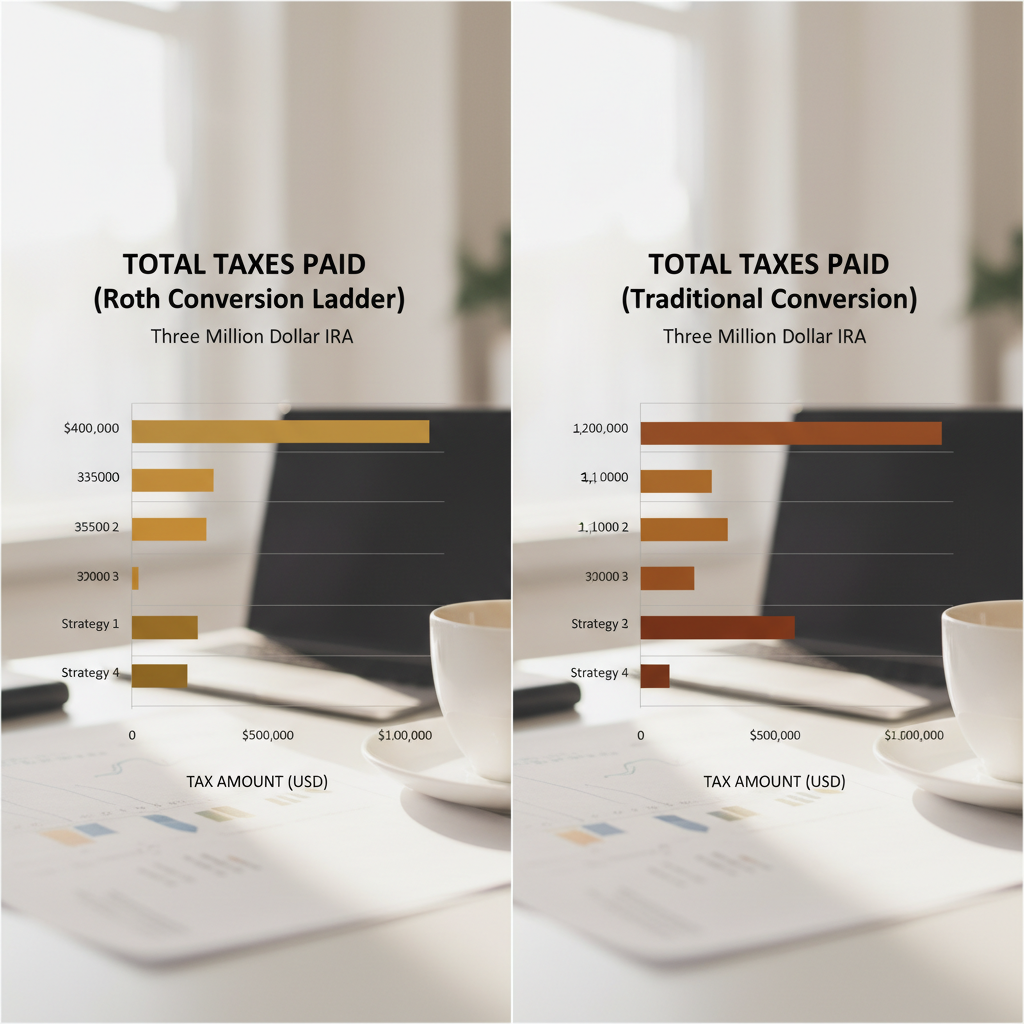

Roth Conversion Ladder vs. Single Large Conversion: Why Timing Matters

Many high-net-worth retirees wonder whether it’s better to convert a large sum all at once or spread conversions over many years. The table below illustrates the dramatic difference.

| Approach | Total IRA Balance | Conversion Period | Estimated Blended Federal Tax Rate | Estimated Total Federal Tax Paid |

|---|---|---|---|---|

| Single Large Conversion | $3,000,000 | 1 year | ~37% | ~$1,110,000 |

| Roth Conversion Ladder (10 years) | $3,000,000 | 10 years at ~$300K/year | ~24-28% | ~$720,000 – $840,000 |

| No Conversion (RMDs only) | $3,000,000 (growing) | 20+ years of RMDs | ~32-37% (with bracket creep) | ~$1,200,000+ (on larger balance) |

| Partial Ladder + QCD Strategy | $3,000,000 | 10 years (conversions + QCDs after 70½) | ~22-26% | ~$600,000 – $780,000 |

The takeaway: A 10-year Roth conversion ladder on a $3 million IRA could save $270,000 to $400,000 or more in federal taxes compared to a single conversion or doing nothing. State taxes (if applicable — Florida residents enjoy no state income tax) and IRMAA costs would adjust these figures further.

This comparison underscores why high-net-worth families need fundamentally different advice than mass-market investors. A $200,000 IRA simply doesn’t produce enough tax savings to justify the complexity. But at $1 million and above, the math becomes compelling — and at $3 million or more, it’s potentially transformational.

Advanced Roth Conversion Ladder Strategies for Affluent Families

Beyond the basic framework, several advanced techniques can amplify the benefits of a Roth conversion ladder for families with substantial wealth.

Tax-Loss Harvesting to Offset Roth Conversion Ladder Income

If you hold a taxable brokerage portfolio alongside your retirement accounts, harvesting capital losses in the same year as a Roth conversion can partially offset the income. While capital losses first offset capital gains (and then up to $3,000 of ordinary income per year), the broader portfolio rebalancing can free up room for larger conversions without increasing your overall tax burden.

Combining Qualified Charitable Distributions (QCDs) with Your Roth Conversion Ladder

Once you reach age 70½, you can direct up to $105,000 per person (2026 limit, indexed for inflation) from your traditional IRA directly to charity via a Qualified Charitable Distribution (QCD). QCDs satisfy RMDs without increasing taxable income.

For charitably inclined retirees, a hybrid approach — converting aggressively in pre-70½ years, then shifting to QCDs — can be the optimal multi-decade tax strategy. This is particularly powerful for families already making $50,000 to $100,000+ in annual charitable gifts.

Using Market Downturns to Accelerate Your Roth Conversion Ladder

Market corrections present a unique opportunity. When your traditional IRA drops 20-30% in value, you can convert the same number of shares at a lower dollar amount — triggering less taxable income — and then benefit from the subsequent recovery inside your tax-free Roth IRA. This “buy low, convert low” approach is one of the most powerful tactics within a broader Roth conversion ladder strategy.

Roth Conversion Ladder Considerations for Business Owners

Business owners face unique complexities. If you’re planning to sell your business, the year of sale may push you into the highest brackets — making conversions inadvisable that year. But the years after a business sale, when your income normalizes, may present an ideal window. Similarly, owners who have deferred compensation or own rental real estate need to model all income streams before sizing each year’s conversion.

The Estate Planning Dimension of a Roth Conversion Ladder

Since the SECURE Act eliminated the “stretch IRA” for most non-spouse beneficiaries, inherited traditional IRAs must now be fully distributed within 10 years. For heirs who are in their peak earning years — a 45-year-old surgeon inheriting a $2 million IRA — this can mean hundreds of thousands of dollars in income taxes at the highest marginal rates.

How a Roth Conversion Ladder Protects Your Heirs

By converting traditional IRA assets to Roth during your lifetime, you effectively prepay the tax at your rate (potentially lower) rather than forcing your heirs to pay at theirs. The inherited Roth IRA still must be distributed within 10 years, but those distributions are tax-free.

For a family with a combined estate of $5 million to $13 million, this intersects with federal estate tax planning. In 2026, the federal estate tax exemption reverts to approximately $7 million per individual (roughly $14 million per married couple), down from the elevated TCJA levels. Paying conversion taxes during your lifetime reduces your taxable estate, which can provide an additional benefit for estates near or above the exemption threshold.

Dynasty Trust Integration with Roth Conversion Ladder Planning

For ultra-high-net-worth families, combining a Roth conversion ladder with contributions to a dynasty trust can create multi-generational tax-free growth. While the Roth IRA itself cannot be placed directly into a trust during the owner’s lifetime, naming a properly structured trust as the Roth IRA beneficiary can provide asset protection and multi-generational control. Consult a qualified estate planning attorney for your specific situation.

Common Mistakes That Derail a Roth Conversion Ladder

Even sophisticated investors make errors when executing this strategy. Here are the most common pitfalls we see:

Mistake 1: Ignoring IRMAA When Sizing Roth Conversion Ladder Amounts

As noted above, Medicare surcharges can erode the net benefit of conversions. IRMAA uses a two-year lookback (your 2024 tax return determines your 2026 premiums), so the impact isn’t felt immediately — but it’s very real. A proper projection must model IRMAA costs in every year of the conversion ladder.

Mistake 2: Converting Too Aggressively in a Single Year

Jumping from the 24% bracket to the 37% bracket in one year eliminates much of the benefit. The power of a Roth conversion ladder lies in consistent, moderate conversions that stay within favorable brackets — not in maximizing conversion volume.

Mistake 3: Failing to Coordinate Across All Accounts and Income Sources

We frequently encounter clients who have a Roth conversion plan that ignores their spouse’s pension, their rental income, or a pending restricted stock vesting event. Every income source must be modeled to avoid bracket surprises.

Mistake 4: Not Accounting for State Taxes

Florida residents enjoy a significant advantage here: no state income tax. But for retirees who recently relocated to Florida from states like California, New York, or New Jersey, there may be questions about domicile establishment and whether the former state will attempt to tax the conversion. Properly establishing Florida domicile is essential.

Mistake 5: Using a Generic Online Calculator Instead of Comprehensive Modeling

Free online Roth conversion calculators rarely account for IRMAA, the interaction between Social Security taxation and conversion income, Net Investment Income Tax (NIIT), or estate tax implications. For portfolios above $1 million, this level of complexity requires professional modeling — it’s one of the key differences between mass-market financial advice and comprehensive wealth management services designed for high-net-worth families.

Who Benefits Most from a Roth Conversion Ladder?

Not every high-net-worth retiree is a candidate. The strategy tends to deliver the greatest value for individuals who meet several of the following criteria:

- Large pre-tax retirement balances ($1 million or more in traditional IRA/401(k) assets)

- Several years of lower income between retirement and RMD age (the “gap years”)

- Sufficient non-retirement assets to pay the annual tax bill without touching converted funds

- A long time horizon for the Roth to grow tax-free (ideally 10+ years before any withdrawals)

- Heirs in high tax brackets who would face steep taxes on an inherited traditional IRA

- Charitable intent that can be paired with QCD strategies

- Florida (or other no-income-tax state) residency that eliminates the state tax cost of conversion

In my experience working with clients, the ideal candidate is often a recently retired executive aged 60-68 with $2 million to $5 million in pre-tax accounts, a healthy taxable brokerage portfolio, and a desire to leave tax-efficient wealth to the next generation.

The 2026 Tax Landscape and Your Roth Conversion Ladder

The expiration of TCJA individual tax provisions creates urgency — and opportunity. While conversions completed in 2025 benefited from the lower TCJA brackets, the 2026 reversion to higher rates doesn’t eliminate the value of a Roth conversion ladder. It simply changes the math.

Under the reverted 2026 brackets, the 28% and 33% brackets return, replacing the TCJA’s 22% and 24% brackets at certain income levels. For a married couple with $400,000 in taxable income, the effective rate on conversions may be 2-4 percentage points higher than in 2025. But compared to the rate their heirs might face — or the rate they’ll face when RMDs combine with Social Security at age 75 — converting in 2026 may still be advantageous.

The critical insight: a Roth conversion ladder is a relative value strategy. You’re comparing today’s tax rate to tomorrow’s estimated rate. Even in a higher-rate environment, if your future rate will be higher still, the conversion wins. This analysis requires year-by-year projections extending 20 to 30 years — exactly the kind of work a qualified financial professional should perform.

Frequently Asked Questions About the Roth Conversion Ladder

What is the ideal annual amount for a Roth conversion ladder?

There is no one-size-fits-all amount. The optimal conversion size depends on your current tax bracket, other income sources, IRMAA thresholds, and long-term projections. For most high-net-worth retirees, annual conversions range from $150,000 to $500,000, sized to fill a target bracket without triggering the next one. Consult a qualified tax professional for your specific situation.

How long should a Roth conversion ladder last?

Most ladders span 5 to 15 years, beginning at or shortly after retirement and continuing until RMDs begin, the traditional IRA is fully converted, or tax rates make further conversions inadvisable. The length depends on the size of your pre-tax balances and your annual conversion capacity.

Can you do a Roth conversion ladder if you’re already taking RMDs?

Yes, but with an important caveat: your RMD itself cannot be converted. You must first satisfy your RMD for the year, then convert additional amounts above and beyond the RMD. This means RMD income is “baked in” as taxable income before you size the conversion, which reduces the room available in lower brackets.

Does a Roth conversion ladder affect my Medicare premiums?

Yes. Roth conversion income increases your Modified Adjusted Gross Income (MAGI), which can trigger IRMAA surcharges on Medicare Part B and Part D premiums. The impact is felt two years after the conversion year. A proper Roth conversion ladder analysis must include IRMAA projections for every year of the strategy.

Is a Roth conversion ladder worth it if tax rates go up in 2026?

In many cases, yes. Even under the higher 2026 rates, converting now may be advantageous if your future combined income (RMDs + Social Security + other income) would push you into even higher brackets. The key is comparing your current conversion rate to your projected future rate — including the impact on your heirs. The analysis is specific to each family’s circumstances.

Take the Next Step Toward a Tax-Efficient Retirement

A well-executed Roth conversion ladder can be one of the most valuable strategies in a high-net-worth retiree’s financial plan — potentially saving hundreds of thousands of dollars in lifetime taxes while creating a more flexible, tax-efficient legacy for the next generation. But the complexity demands precision, and the margin for error is significant at these dollar amounts.

If you’re evaluating whether a Roth conversion ladder belongs in your retirement plan, the right analysis starts with a clear picture of your complete financial situation — something a discovery conversation with a qualified advisor can help you begin.

📘 Want to understand how IRMAA surcharges interact with your Roth conversion strategy? Download our Medicare IRMAA Planning Guide for a detailed breakdown of thresholds, surcharge tiers, and planning strategies designed for high-net-worth retirees.

📞 Ready for personalized guidance from a fee-based fiduciary? Book a complimentary phone call with our team to discuss your Roth conversion ladder and broader retirement tax strategy.

This content is for educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Advisory services offered through Davies Wealth Management, a Registered Investment Adviser. Please consult a qualified financial, tax, or legal professional regarding your specific situation.

“`

Leave a Reply